Chargeback Ratio Thresholds: When the Networks Step In

Source: Visa VAMP fact sheet (2025) · Mastercard ECP program guide

A 1% chargeback ratio sounds small until you realize what crossing the chargeback ratio threshold actually triggers. The networks don’t issue warnings. They issue fees, then reserves, then termination — and the rules changed substantially in 2025, then tightened again in April 2026.

Most merchants don’t think about their chargeback ratio until a processor sends a notice. By then the math has already happened — disputes counted, ratio calculated, threshold crossed, account flagged. The window to react is narrower than it should be, and the penalties escalate faster than most merchants expect. A confirmed scam merchant monitoring case can cut off acceptance even faster.

This post lays out where the lines actually are. Visa rewrote its monitoring framework in April 2025, tightened it in October 2025, and stepped the threshold down again on April 1, 2026. Mastercard’s program runs in parallel with different math and different fines. And both networks share the same nuclear option — placement on the MATCH list, which functionally ends a merchant’s ability to accept cards anywhere for five years.

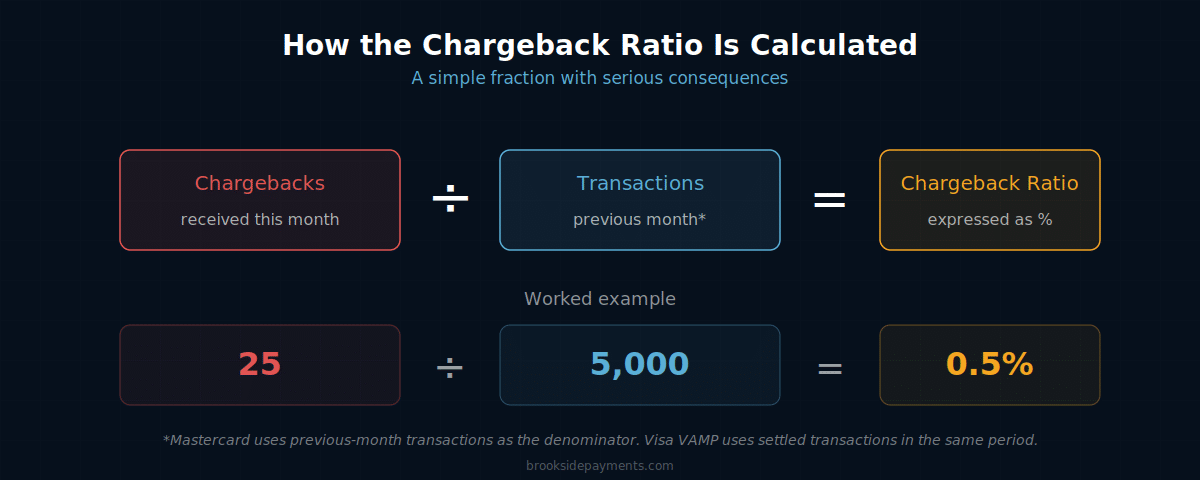

How the Chargeback Ratio Is Calculated

The chargeback ratio is the number of chargebacks divided by the number of transactions, expressed as a percentage. Simple in concept — but the networks calculate it differently, and your ratio under one framework may not match your ratio under the other.

For a deeper walkthrough of how the ratio works, what’s a “good” number for your industry, and the timing trap that catches merchants off guard, see the chargeback ratio glossary entry. The rest of this post focuses on what happens once your chargeback ratio threshold is crossed — and crossing it is what triggers the monitoring programs the networks rolled out in 2025.

Visa VAMP — The Chargeback Ratio Threshold That Just Tightened

Until April 2025, Visa ran two separate monitoring programs: the Visa Dispute Monitoring Program (VDMP) for chargebacks and the Visa Fraud Monitoring Program (VFMP) for fraud. Effective April 1, 2025, both were consolidated into a single framework — the Visa Acquirer Monitoring Program, or VAMP. The advisory period ended October 1, 2025, when Visa began enforcing penalties.

The consolidation changed three things merchants need to understand.

Under VDMP and VFMP, merchants got an early-warning identification before crossing into Excessive territory. Under VAMP, there’s only one identification level for merchants — Excessive. A merchant either trips the threshold or doesn’t. Visa does grant a three-month grace period to first-time offenders — defined as merchants who have been out of VAMP for at least 12 months on a rolling basis — during which enforcement fees are held off; after that window, a merchant still over the line is enrolled and assessed fees per disputed or fraudulent transaction.

Visa initially set the merchant Excessive threshold at 2.2% combined fraud + dispute ratio. As of April 1, 2026, that threshold is 1.5% in the U.S., Canada, the EU, and Asia-Pacific; CEMEA remains at 2.2%. A merchant sitting at 2.0% — comfortably under the old 2.2% line — is now in violation.

The number being measured also changed. VAMP merges what used to be two separate metrics into one ratio: reported fraud (Visa’s TC40 reports) plus disputes (TC15) divided by settled transactions (TC05), counting card-not-present activity only. The catch is double-counting — one $500 order flagged as fraud and then charged back lands as two strikes against the same ratio, so a merchant that only manages chargebacks while ignoring fraud reports can stay above threshold without understanding why.

An acquirer’s portfolio is flagged Above Standard at 0.5% and Excessive at 0.7%. To stay below those portfolio averages, many acquirers impose internal merchant thresholds well below Visa’s published 1.5% — sometimes as low as 1.0%. The merchant feels the squeeze before the merchant has done anything wrong by Visa’s measure.

The minimum trigger to qualify for VAMP enforcement is 1,500 combined fraud reports and disputes per month. Below that, the program doesn’t apply. Above it, Visa charges $8 per fraudulent or disputed transaction at the Excessive level. A merchant with 2,000 monthly disputes at the Excessive threshold is paying $16,000 a month in VAMP fees on top of standard chargeback fees.

The Excessive Chargeback Program — Two Tiers and Escalating Fines

Mastercard’s Excessive Chargeback Program (ECP) runs on different math and different consequences than Visa’s framework. It’s also been more stable — the structure has changed less, but the penalties have always been steeper for merchants who linger above threshold.

The program has two tiers. A merchant gets flagged at the lower tier first, with a one-month grace period before fines begin.

Triggered by 100+ chargebacks AND a 1.5% – 2.99% chargeback-to-transaction ratio in a single month. Both must be exceeded. Fines start in the second consecutive month at $1,000, then escalate: $5,000 monthly in months 4–6, $25,500 in months 7–11, $50,000 in months 12–18, and $100,000 monthly from month 19 onward.

Triggered by 300+ chargebacks AND a 3.0%+ ratio in a single month. Fines escalate faster. Beyond month 4, Mastercard may also assess an Issuer Recovery Assessment of $5 per chargeback above 300 — on top of the monthly fines and the per-dispute fees the merchant’s processor is already charging.

The exit path is also strict: a merchant must stay below the ECM threshold for three consecutive months to graduate from the program. One month back over the threshold and the clock resets. For high-velocity merchants — subscription services, e-commerce with tight margins, anything with seasonal volume — three clean months in a row is harder than it sounds.

What Happens When the Account Is Terminated

Above the Excessive thresholds, the next step isn’t another fine. It’s account termination. And termination is rarely the end of the consequences — it’s the beginning of a five-year industry shutout.

The MATCH list — Member Alert to Control High-Risk Merchants — is a database maintained by Mastercard and accessed by every member acquirer in the network. When a merchant is terminated for excessive chargebacks (or a handful of other reasons including fraud, money laundering, and account data compromise), the acquirer reports the merchant to MATCH. The listing stays for five years.

What that means in practice: every time the merchant tries to open a new merchant account at any processor, MATCH is checked. A hit on MATCH doesn’t legally prohibit a processor from underwriting the merchant — but no major processor will. The merchant is functionally locked out of the card-acceptance system for five years, regardless of how the underlying chargeback situation actually got resolved.

This is also why high-risk merchant account processors exist as a separate category. They serve businesses that can’t get into the standard acceptance system — sometimes because of MATCH listings, sometimes because of vertical risk profile, sometimes because of merchant history. The pricing is correspondingly higher.

What Actually Keeps Your Ratio Down

One reflex backfires. Tightening fraud filters to auto-decline anything borderline feels like the safe move, but it shrinks the denominator — total transactions — without lowering the fraud reports and disputes in the numerator, which pushes the ratio up, not down. Staying under 1.5% is a dual problem: approve more legitimate orders while cutting genuine fraud and disputes, not simply blocking more aggressively.

Most ratio-management strategy isn’t about winning chargeback disputes — it’s about preventing them from being filed in the first place. Once a chargeback is filed, even a successful dispute response counts toward the chargeback ratio threshold the networks are watching. The math doesn’t care whether you won or lost.

Visa’s Rapid Dispute Resolution (RDR) and Verifi’s CDRN platform allow merchants to refund a customer before a chargeback is formally filed. These resolutions are excluded from the VAMP ratio calculation entirely. They cost the sale, but they don’t cost the ratio damage — which is the right trade for a merchant near a threshold.

Issuer-side alert systems notify merchants when a customer has initiated a dispute conversation with their bank but before the chargeback is formally filed. The alert window is short — usually 24–72 hours — but a proactive refund within that window prevents the chargeback from ever counting against the ratio.

Visa’s updated framework for first-party-fraud disputes lets merchants submit evidence of customer engagement (login history, prior order history, IP patterns) that, when accepted, removes the dispute from the VAMP ratio. This works against the rising volume of friendly fraud disputes specifically.

A non-trivial share of disputes get filed because customers don’t recognize the business name on their statement. The descriptor that appears should match what the customer expects — DBA name, ideally with a contact phone number. Cleaning up the descriptor is the cheapest, fastest ratio intervention available.

A processor that monitors your ratio in real time and calls when it climbs is worth meaningfully more than one that processes disputes without comment. The same volume of chargebacks at two different processors can produce two completely different outcomes depending on whether someone is paying attention.

Frequently Asked Questions

It depends on which network. Mastercard’s ECM tier triggers at 100 chargebacks AND a 1.5% chargeback-to-transaction ratio in a single month. Visa’s VAMP triggers at 1.5% combined fraud and dispute ratio in the U.S., Canada, EU, and Asia-Pacific (2.2% in CEMEA), as of April 1, 2026, with a minimum of 1,500 combined disputes and fraud reports per month. Both must be calculated separately because the formulas differ.

No. The chargeback counts toward the ratio at the moment it’s filed, regardless of outcome. The only ways to keep a chargeback off the ratio are pre-dispute resolution (Visa RDR, Verifi CDRN, Ethoca alerts) or successful representment under Visa’s Compelling Evidence 3.0 framework, which removes qualifying disputes from VAMP calculations.

Mastercard’s ECP requires three consecutive months below the ECM threshold. Visa’s VAMP requires the merchant to drop below the Excessive threshold and stay there. The clock resets if the merchant goes back above the threshold even briefly. In both cases, exiting requires structural fixes — billing descriptor changes, fraud screening upgrades, refund policy adjustments, or pre-dispute alert subscriptions — not just a quiet month.

MATCH stands for Member Alert to Control High-Risk Merchants. It’s a database Mastercard maintains and every major acquirer checks before underwriting a new merchant account. A merchant gets listed when terminated for excessive chargebacks (or other defined reasons), and the listing stays for five years. A MATCH listing functionally locks the merchant out of mainstream card acceptance for the duration — which is why high-risk merchant account providers exist as a separate category for businesses with MATCH history.

More on chargeback risk and dispute mechanics

If Your Chargeback Ratio Is Climbing, You Need a Processor Who’s Watching

A processor that flags your ratio climb at 0.8% and helps you intervene before you cross 1.5% is worth meaningfully more than one that processes the chargebacks silently and waits for the threshold to trigger a reserve. The difference shows up in your statement — in the dispute fees, in the reserve hold, in the program fines that may or may not appear. A free statement review shows you exactly what your processor is charging per chargeback, what your effective dispute exposure looks like at your volume, and what a processor relationship that actively manages ratio risk looks like.

Get Your Free Statement ReviewNo obligation • No pressure • Response within one business day