Card Network Dispute MonitoringChargeback Ratio

Chargeback Ratio — Definition & Guide

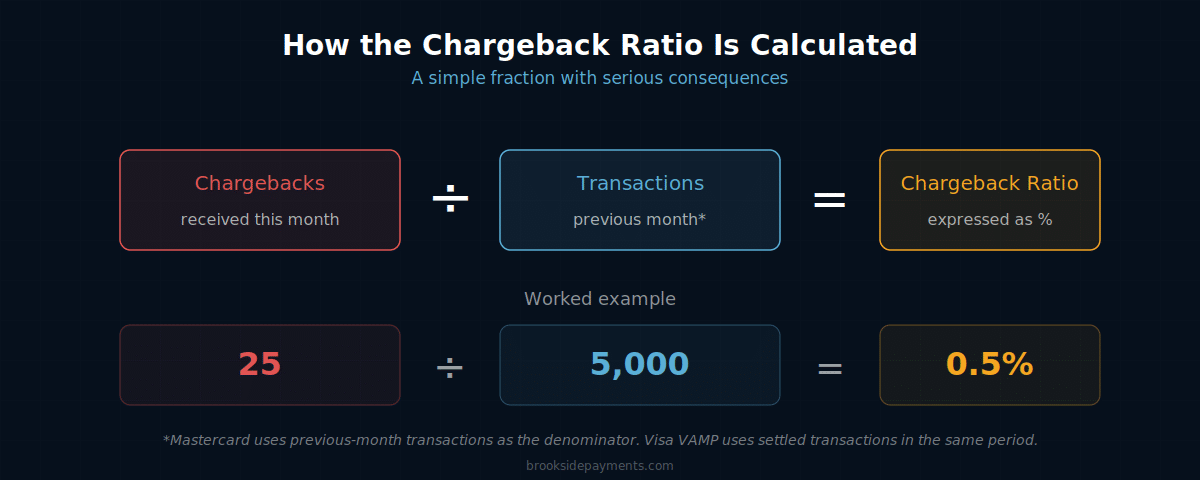

Your chargeback ratio is a simple percentage: chargebacks received divided by total card transactions, expressed as a percentage. Card networks monitor this metric closely for every merchant. Cross the wrong threshold and you face fees, reserves, or account termination — and the rules tightened substantially in 2025.

The number counts all chargebacks received — even ones you win. A successful dispute response recovers the funds but does not remove the chargeback from the ratio calculation. This is why prevention matters more than response.

Visa and Mastercard each operate dispute monitoring programs with defined thresholds. The numbers are different for each network, and Visa rewrote its framework in April 2025:

- Below 0.65% — Safe zone. No monitoring program risk. This is the target for merchants who process recurring billing or card-not-present transactions.

- 0.65% – 1.5% — Early warning territory. Some processors flag accounts in this range for internal review before network programs trigger.

- Above 1.5% — Mastercard’s Excessive Chargeback Merchant (ECM) threshold (with 100+ monthly chargebacks). Visa’s VAMP threshold drops to 1.5% on April 1, 2026 in the U.S., Canada, and EU. Placement triggers fines and mandatory remediation.

- Above 3.0% — Mastercard’s High Excessive Chargeback Merchant (HECM) threshold. Account termination risk. MATCH list placement becomes likely if not remediated quickly.

For a deeper walkthrough of network programs, fines, and what happens when accounts cross these lines, see chargeback ratio thresholds.

Most merchants assume the calculation uses current-month transactions as the denominator. For Mastercard, it doesn’t. Mastercard’s formula divides this month’s chargebacks by last month’s transactions. The reasoning is that chargebacks typically arrive 30–60 days after the original sale, so dividing them against the month they originated is more accurate than dividing them against the month they were filed.

The problem is what happens during volume swings. A holiday-driven retailer with a big December and a quiet January can show up on Mastercard’s monitoring radar in February, when their January chargebacks (from December sales) divide against January’s much smaller transaction count. The merchant feels stable. The number doesn’t.

Visa’s VAMP uses a different formula — settled card-not-present transactions in the same period as the disputes — so the timing trap doesn’t apply there. But knowing both calculations is the only way to predict where you actually stand with each network.

Prevention is more effective than response. The most common causes of elevated ratios — and how to address them:

- Unclear billing descriptors — Customers who don’t recognize a charge dispute it. Use a clear, recognizable business name on every statement descriptor.

- Missing CVV and AVS — Collect and submit billing address and security code on every card-not-present transaction. Reduces fraud-based disputes significantly.

- No delivery confirmation — For shipped goods, always send tracking information and delivery confirmation. Documentation wins disputes.

- Difficult refund process — Make refunds easy to request. A customer who can get a refund directly rarely escalates to a dispute.

- Slow retrieval responses — Respond to retrieval requests immediately. A missed retrieval becomes a chargeback automatically.

The CFPB’s guidance on dispute rights outlines what cardholders are entitled to in a dispute — understanding the cardholder’s perspective is the most direct path to reducing frivolous disputes before they are filed.

Keep your ratio below 0.65% to avoid any monitoring program risk. Above 1.5% triggers Mastercard’s ECM program and (after April 1, 2026) Visa’s VAMP program in the U.S., Canada, and EU. Above 3.0% triggers Mastercard’s HECM program with severe fines and account termination risk.

Yes. The ratio counts all chargebacks received, even those you successfully dispute and win. A successful response recovers the funds but does not remove the chargeback from the ratio calculation — which is why prevention is more valuable than response.

Use clear billing descriptors, require CVV and AVS on card-not-present transactions, send delivery confirmations, make refunds easy to request, and respond promptly to retrieval requests before they escalate to disputes.

Concerned About Your Account’s Dispute History?

A high chargeback ratio affects more than your account standing — it affects your rates, your reserves, and your processor options. Send us your last processing statement. We will show you what your dispute history looks like from a processor’s perspective and what steps reduce your exposure before it becomes a problem.

Request a Free Statement ReviewNo obligation • No pressure • Response within one business day