Why Firearms Payment Processing Breaks on Stripe, Square, and PayPal

Why Firearms Payment Processing Breaks on Stripe, Square, and PayPal

Firearms payment processing almost always starts the same way: a licensed dealer signs up for Stripe, Square, or PayPal in a few minutes, runs sales for a while, and assumes payments are handled. Then one morning the account is frozen, the funds are held, and there is no one to call. It is not bad luck. Those platforms are aggregators — they run thousands of businesses under one master merchant account and screen signups with automated rules. Their acceptable-use policies explicitly prohibit firearms, ammunition, and related products, and their systems flag those words on sight.

The model that makes aggregators effortless for a coffee shop is exactly what makes them dangerous for a gun shop. There is no individual underwriting, so nobody ever evaluated your business as a firearms business — the algorithm simply had not caught it yet. When it does, the response is automatic: the account is terminated and the balance can be held for up to 180 days against potential chargebacks, usually with no meaningful appeal. Being fully licensed does not help, because the platform’s objection was never to your compliance — it was to the category. Stable firearms payment processing has to start somewhere else entirely.

An aggregator gives you a shared merchant ID and instant, automated approval — fine for low-risk retail, a liability for firearms. A dedicated firearms merchant account gives you your own merchant ID, underwritten by people who actually reviewed your FFL and your business. The first is built to onboard fast; the second is built to keep you on.

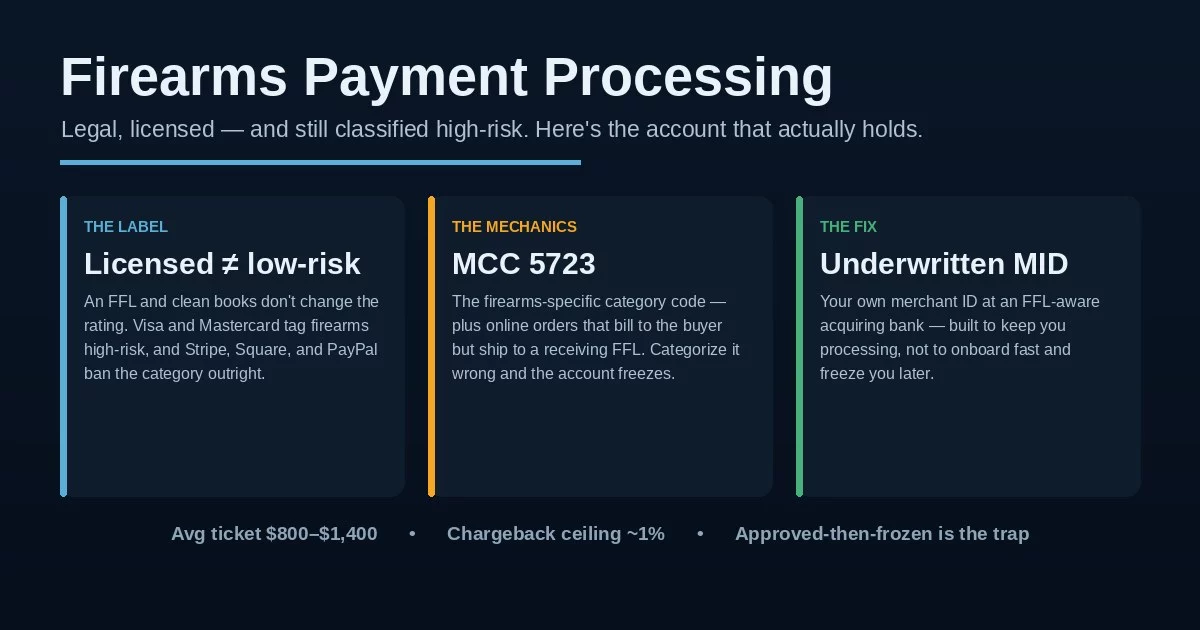

A Legal, Licensed Gun Shop Is Still “High-Risk”

Selling firearms is legal, federally regulated, and licensed through the ATF — so why do banks treat it as high-risk? Because “legal” and “low-risk” are not the same thing to an acquiring bank. Three forces stack up. First is reputational and political exposure: card networks and banks have watched activist pressure and media campaigns push some processors to de-platform firearms merchants preemptively, so they price that risk in. Second is the average ticket — firearms sales commonly run $800 to $1,400, and high-ticket disputes hurt more. Third is chargeback sensitivity: exceed the card networks’ roughly 1% dispute threshold and you land in a monitoring program with heavy monthly fines that can end the account.

None of that is a judgment about whether you run a clean shop. It is a structural classification, the same one that covers other regulated categories — our overview of high-risk payment processing lays out how these accounts differ from ordinary ones, and the CBD and hemp world faces the identical “legal but high-risk” trap. Understanding the label is the first step to building firearms payment processing that lasts instead of getting blindsided. The same forces that classify firearms as high-risk also make these accounts targets for sudden repricing and review once they are open.

When an aggregator terminates a firearms account, it does not just stop new sales — it can hold the money already in the pipeline for up to six months. That is payroll, inventory at the distributor, and rent locked away with no appeal, often arriving with zero warning. For most independent gun shops and online FFLs, a single freeze is an existential event, not an inconvenience.

What MCC 5723 Means for Your Account

Every business is assigned a Merchant Category Code that tells the card networks what you sell. Firearms retailers historically rode under broad codes like sporting goods (MCC 5941), but a firearms-specific code, MCC 5723, now exists to identify gun and ammunition sellers more precisely. Its rollout is contested and uneven — some states have moved to require it, others have moved to restrict or ban its use, and how widely acquirers apply it still varies. For a dealer, the practical point is not the politics; it is that your account has to be categorized correctly and consistently.

That matters because the most common reason a firearms account gets frozen is a mismatch. If a processor slotted you under generic “retail” or “sporting goods” to win your business on a cheaper rate, and your transaction pattern later reads as firearms, the sponsor bank can flag the misclassification and shut you down — funds held while they sort out the exposure. There is one more firearms-specific wrinkle most processors mishandle: on an online order the card bills to the buyer, but the gun ships to a receiving FFL, not the cardholder’s address. A payment system that cannot handle bill-to and ship-to being different addresses will throw fraud flags on perfectly legitimate transfers. Getting firearms payment processing right means the categorization and the FFL-transfer workflow are both built in from day one.

A processor that promises low-risk retail rates for a gun shop is usually planning to file you under the wrong MCC. It looks like savings for a few months — until an audit catches the mismatch and the account is terminated. Correct categorization under MCC 5723 from the start is what makes a firearms account stable, even though it prices higher than vanilla retail.

What a Real Firearms Merchant Account Looks Like

The durable answer is a dedicated firearms merchant account placed with an acquiring bank that actually wants the category — not an aggregator that tolerates you until its system notices. That means your own merchant ID, individual underwriting by analysts who understand FFL documentation, and a processor that expects firearms volume rather than getting startled by it. The same structure scales across channels: a retail counter, an online FFL doing transfers, an ammunition or parts seller, or a range running memberships all sit under the same FFL-aware underwriting umbrella. A proper FFL merchant account is built to verify your license, handle the bill-to/ship-to split, and survive the monitoring that high-risk firearms processing always carries.

Underwritten gun store payment processing costs more than vanilla retail, and that is expected — plan for it rather than chasing a headline rate that will not survive underwriting. Per-transaction pricing typically runs above standard retail, there is usually a monthly gateway fee, and many setups carry a rolling reserve, where the processor holds back a percentage of sales for a set period as protection against chargebacks. None of that is a scam; it is the cost of stability. What you can control is transparency: insisting on interchange-plus pricing so the processor’s markup is a visible line item, and running any offer through an effective rate calculator so you compare true all-in costs, not the rate on the first page.

Your own merchant ID, underwriting that already accounts for firearms, correct MCC categorization, a checkout that handles FFL-transfer shipping, and chargeback tools built for high-ticket disputes. You trade a slightly higher rate for the thing that actually matters — an account that is still processing next quarter.

Staying Approved — and What to Ask Before You Sign

Getting approved is the easy part; staying approved is where firearms merchants get hurt. Acquiring banks keep monitoring an account long after onboarding, and the trigger is usually a change, not the product: a new online sales channel, a jump in volume that no longer matches what underwriting approved, or a chargeback ratio drifting toward the networks’ threshold. Guard that ratio above all — crossing the card networks’ dispute thresholds can get an account terminated and land the business on the MATCH list, an industry blacklist that makes the next account far harder to open. Clean billing descriptors, AVS and CVV checks on card-not-present orders, and strong evidence when you do fight a dispute keep you clear; the same discipline keeps a rolling reserve from ballooning.

Whether you are opening a first firearms account or replacing one that just got frozen, the vetting questions are concrete. Will you get your own merchant ID, individually underwritten — or are you being slotted into a shared aggregator account? Are you being categorized under MCC 5723, or filed cheap under sporting goods? What is the reserve structure, what percentage, and when does it release? Does the gateway handle FFL-transfer shipping where bill-to and ship-to differ? Is the pricing interchange-plus, with the markup spelled out? And read the merchant agreement closely — the term length, early-termination fee, and reserve language matter most when something goes wrong. Done right, firearms payment processing stops being the thing that could end your business overnight and becomes just another part of running it.

Frequently Asked Questions

Not reliably. All three are aggregators whose acceptable-use policies prohibit firearms and ammunition, and their automated systems freeze or terminate accounts when they detect the category — often holding funds for months with no real appeal. Being a fully licensed FFL does not change it, because the objection is to the category, not your compliance. A dedicated firearms merchant account is the stable path to durable firearms payment processing.

MCC 5723 is the firearms-specific Merchant Category Code used to identify gun and ammunition sellers, distinct from the older sporting-goods code. Its use is contested and varies by state and acquirer, but the practical issue is categorization: if a processor files you cheap under generic retail and your activity later reads as firearms, the bank can flag the mismatch and shut the account down. Correct categorization from the start is what keeps a firearms account stable.

Because firearms ship to a receiving FFL, not to the cardholder, so the billing address and shipping address legitimately differ — and a payment system built for ordinary retail reads that as fraud. An FFL-aware firearms merchant account and gateway are set up to handle the bill-to/ship-to split, so legitimate transfers clear instead of getting blocked or held.

Keep Reading Before You Choose a Processor

Get a firearms processing setup built to last — not one waiting to be frozen.

Send us your current setup or a recent statement and we will show you whether you are on an aggregator that could freeze you, whether your account is categorized correctly, what a properly underwritten firearms account would cost, and how to structure it so approval actually holds — no obligation, no sales pressure. Learn more about payment processing consumer protections from the CFPB.

Review My Firearms Processing SetupNo obligation • No pressure • Response within one business day