When Your Processor Rebrands, Nothing Changes

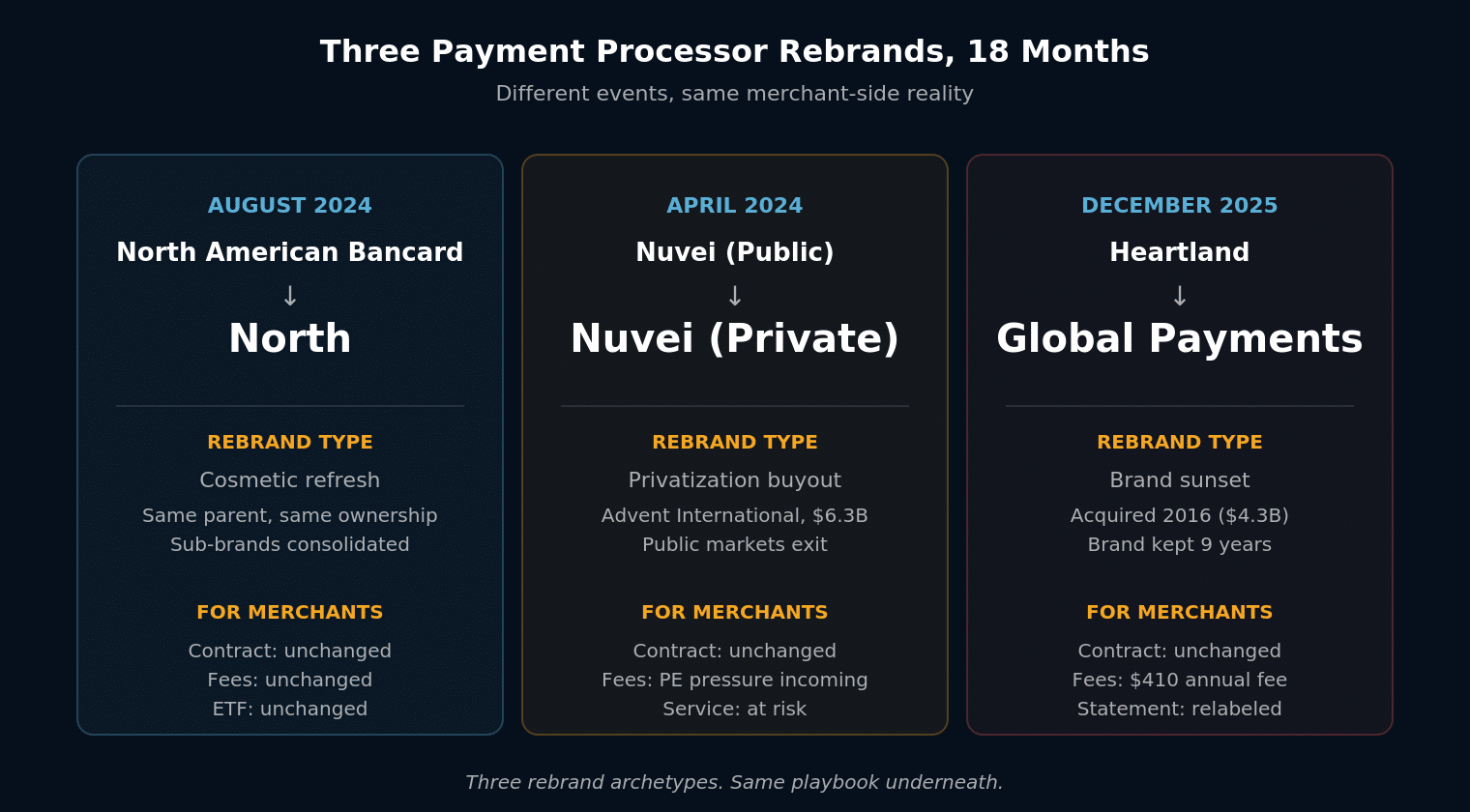

If your processing statement looks different this month — new logo, new color scheme, new name at the top — there is a reasonable chance you have just lived through a payment processor rebrand. Three of the larger names in U.S. merchant services have changed brand identities in the past 18 months. North American Bancard became North in August 2024. Nuvei was taken private by Advent International in April 2024 in a $6.3 billion buyout. And by December 2025, the Heartland Payment Systems brand was officially sunset after nine years as a subsidiary, with all Heartland branding and logos replaced by Global Payments on monthly statements.

Three different corporate events. Three different payment processor rebrand archetypes. One identical merchant-side reality: the contract you signed is still in force, the fees you were paying are still being charged, and the early termination penalty written into your agreement is still enforceable. The brand on the statement changed. Almost nothing else did.

This post explains what each of the three payment processor rebrands actually was, why they happened, and what merchants should and should not do in response. The short version: a payment processor rebrand is not a reason to switch processors, and it is not a reason to feel reassured. The contract terms govern the relationship, and the contract terms did not change just because the brand did.

Three different corporate events. Same merchant-side reality: the contract, the fees, and the early-termination penalty are unchanged. The brand on the statement is the only thing that moved.

North American Bancard Became North — A Cosmetic Payment Processor Rebrand

On August 5, 2024, North American Bancard announced it would now be known as North. The Troy, Michigan-based company had grown through three decades of organic expansion and acquisitions, accumulating sub-brands including Point & Pay, CWA Merchant Services, Electronic Payment Exchange, Inovio Payments, Money Machine, and PayTrace. The North payment processor rebrand consolidated all of these under a single name; sub-brands were re-labeled as “by North.”

The stated reason was alignment between the company’s “innovative spirit” and “outward image.” Founder and CEO Marc Gardner said the new name “best represents the company’s long-standing recognition and expertise in the payments space.” The rebrand did not involve a change in ownership, processing platforms, or the merchant agreements customers had signed.

The North case is the cosmetic-refresh archetype. The brand changed; the company did not. Merchants on the legacy North American Bancard contracts continued to pay the same fees, on the same schedule, under the same termination provisions. Some merchants reported still seeing North American Bancard logos on statements months after the rebrand was announced — large processors run statement generation through legacy systems that update on their own cadence, not the marketing department’s.

The complaint pattern around North also did not change. Third-party review sites tracking merchant feedback continued to log the same categories — disputed billing, fees not disclosed at signing, difficulty reaching support, friction on contract cancellation. Reviewers noted complaint volume remained steady or increased through the first half of 2025, which suggests the payment processor rebrand was a brand-marketing exercise rather than operational change.

For merchants, the North rebrand prompted exactly one practical question: does the new name on my statement mean my contract has changed? It does not. The contract you signed with North American Bancard is the contract you have with North. The legal entity, the obligations, and the termination provisions all carry over.

Cosmetic refresh. Same parent, same ownership, same contracts. The brand consolidation made existing internal structure visible; it did not change anything about what merchants pay or what they signed.

Nuvei Was Taken Private by Advent International — The PE Payment Processor Rebrand

The Nuvei case is different in kind from the North case. On April 1, 2024, Nuvei announced a definitive agreement with private equity firm Advent International to be taken private in an all-cash deal valued at $6.3 billion. Public shareholders received $34.00 per share, a 56% premium to where the stock had been trading three weeks earlier. As of mid-2024, Nuvei was no longer a publicly traded company.

The name “Nuvei” did not change. What changed was the ownership, the capital structure, and the operating mandate. A publicly traded payments processor with declining stock had become a private company majority-controlled by one of the largest private equity firms in the world. This is a payment processor rebrand of a different kind — the brand identity stayed the same, but everything underneath it changed.

This matters because the private equity payment processor playbook is well-documented and operates on a predictable schedule. PE buyouts in payments aim to extract returns through some combination of fee increases, support cost reductions, contract enforcement intensification, and eventual resale at a higher multiple. The acquired company tends to look the same on the surface for the first 12 to 18 months. The merchant-side changes arrive on a delay — rate creep, support degradation, harder cancellation processes, tougher chargeback positions.

We have covered this pattern in detail separately. The short version is that the PE playbook is the dominant economic force shaping merchant services in the U.S. right now, and the Nuvei privatization is a textbook example of it. The rebrand here is not the name change — Nuvei kept its name. The rebrand is the structural shift from public-company to PE-portfolio-company, and the operational consequences that come with it.

Merchants on Nuvei contracts in 2024 may not have noticed the privatization at all. Merchants on Nuvei contracts in 2025 and 2026 should expect to see the playbook play out — small fee additions, harder service interactions, contract enforcement that did not exist before. If those signals appear, they are not random. They are the visible consequences of a corporate event that happened in April 2024.

The brand stayed the same, the ownership did not. PE buyouts run on a 12-to-24-month delay before merchant-side changes appear. The April 2024 transaction is the cause; the rate creep and service degradation arriving in 2025 and 2026 are the predictable effects.

Heartland Sunset to Global Payments — A Brand-Sunset Payment Processor Rebrand

Heartland Payment Systems was acquired by Global Payments in 2016 for $4.3 billion. At the time, Global Payments committed to operating Heartland under its existing brand — a commitment Heartland’s CEO described in SEC filings as “the deal clincher.” Global Payments would retain the Heartland name, the merchant bill of rights, and the sales professionals bill of rights. For nine years, Global Payments honored that commitment.

That arrangement ended in late 2025. By December 2025, all Heartland branding and logos were replaced with Global Payments on monthly statements and payment platforms. Heartland customers received notification that their accounts were officially Global Payments accounts as of the brand transition. Press around the change was minimal because Global Payments had been running Heartland for nearly a decade — the change was paper, not operational.

Two specific items were noteworthy. First, the Annual Reporting Fee billed to former Heartland customers on December 2025 statements was up to $410 per location, roughly $200 higher than the equivalent fee the prior year. The fee increase coincided with the brand transition but was an independent decision; processors regularly increase annual fees on December statements regardless of whether a payment processor rebrand is happening. Merchants caught up in the rebrand may have read the fee increase as part of it. It was actually the standard year-end fee adjustment, with the rebrand running in parallel.

Second, the Heartland Merchant Bill of Rights — a published commitment to transparent pricing and merchant-friendly contract terms that Heartland had used as a differentiator for two decades — was effectively dissolved by the brand sunset. The Bill of Rights had been a signature of the Heartland brand. Once the brand was retired, the marketing artifact retired with it. Whether the underlying commitments persist as informal Global Payments policy is a question that will be answered case-by-case as merchants test it.

The Heartland rebrand is the brand-sunset archetype. The acquisition happened a decade ago. The brand was preserved for marketing reasons. When those reasons stopped justifying the cost of running two parallel brand identities, the legacy brand was retired. Merchants who chose Heartland in the 2016-to-2024 window were buying a brand that no longer exists. The contract they signed, however, does still exist. So do the fees.

A nine-year brand preservation ended in late 2025. The Merchant Bill of Rights that was a Heartland marketing differentiator dissolved with the brand. Annual reporting fees rose to up to $410 per location on December 2025 statements — coincident with the rebrand but billed independently of it.

What the Three Payment Processor Rebrands Have in Common

The three events are different on the surface. North changed its name. Nuvei changed its ownership. Heartland was retired into a parent brand. The corporate-comms reasons given for each were also different — innovation alignment, capital structure optimization, brand consolidation. The press treated them as three unrelated events, which they were at the corporate level.

From the merchant side, however, the three payment processor rebrands sit on the same spectrum. Each was a visible signal of an underlying corporate dynamic that had been running for years. North had been quietly consolidating its sub-brand portfolio for a decade before the rebrand made the consolidation visible. Nuvei had been struggling with public-market valuation for several years before the privatization made the strategic shift visible. Heartland had been a Global Payments subsidiary for nine years before the brand sunset made the integration visible.

The payment processor rebrand, in other words, is the part of the iceberg that surfaces. The underlying corporate dynamic was already in motion. For merchants paying attention, the rebrand is mostly useful as a signal that something the company had been doing privately is now visible publicly — not as a new event that requires a new response.

This is the same pattern that shows up in regulatory events on the network side. The 2026 Visa-Mastercard settlement is being treated by the trade press as a major event because the dollar number is large. From the merchant-statement side, the actual changes are a small interchange trim and modified network rules — operationally meaningful for merchants who actively manage their card mix, mostly invisible for merchants who do not. In both the rebrand case and the regulatory case, the same epistemic move applies: the loud announcement is rarely where the merchant impact lives. The contract terms, the pricing model, and the underlying network rules are where it lives.

What the three payment processor rebrands also have in common is what they do not change. They do not change merchant agreements. They do not change processing fees. They do not change the early termination penalty written into existing contracts. They do not change the gateway technology, the chargeback dispute process, or the funding cadence. They change the brand identity, the marketing materials, and in some cases the corporate ownership structure. The merchant-facing operational layer is largely unaffected.

The payment processor rebrand is the part of the iceberg that surfaces. The underlying corporate dynamic was already running — for years, in each case. The rebrand is not a new event requiring a new response; it is a visible signal of something private becoming public.

The Three Reactions Merchants Have to a Payment Processor Rebrand

When a processor rebrands, three merchant reactions are common. Each one is wrong for slightly different reasons.

Reaction 1: “I should switch processors because the brand changed.” A payment processor rebrand is not a reason to switch. The fees, the service quality, and the contract terms determine whether switching makes sense — and those signals existed before the rebrand and will persist after it. If the underlying service was good before the rebrand, it likely remains good. If it was bad before, the rebrand did not fix it. The right time to switch is when the underlying economics or service quality justify it, which is a separate analysis from whether a rebrand happened.

Reaction 2: “I should feel reassured because the company is investing in itself.” This is the read most processor sales reps want merchants to take. The payment processor rebrand gets framed as evidence of forward momentum, technology investment, customer focus. In some cases that framing is accurate. In most cases it is not. The North rebrand was a marketing exercise. The Nuvei privatization was a capital-structure decision. The Heartland sunset was a brand-consolidation decision. None was inherently good or bad for existing merchants, but none was the merchant-friendly investment the marketing would suggest.

Reaction 3: “I should ignore it entirely.” Closer to right, but not quite. A payment processor rebrand is informational. It tells you something about the corporate posture of your processor — whether they are investing in marketing, going through ownership changes, or being absorbed into a parent company. Each signal predicts something about the next 12 to 24 months of the relationship. Ignoring the rebrand means missing the signal it carries. Reading it correctly means treating it as a data point about your processor’s trajectory, not as a reason to take immediate action.

The right reaction is to treat the rebrand as a prompt to re-read your processing statement with fresh attention. Has the effective rate changed? Have new fees appeared? Have line-item names changed in ways that obscure what is being charged? The rebrand is neutral. The statement that arrives after will tell you whether anything changed underneath.

Processor sales teams are most active in the 90 days following a rebrand. The brand event is treated internally as a moment when merchants are paying attention to their statements, which makes it a natural time to push contract renewals, equipment leases, or “platform alignment” upgrades. If your rep calls about something other than a routine check-in within three months of a rebrand announcement, the call is part of the rebrand strategy — not separate from it.

The Four Signals That Matter on a Post-Rebrand Statement

If your processor has been through a payment processor rebrand recently — and given the cadence of consolidation in payments, it is increasingly likely that yours has — there are four specific things worth checking on the next statement that arrives.

First, the legal entity name in the fine print. The brand at the top of the statement is the marketing identity. The legal entity that holds your contract is named in the small text at the bottom or in the contract itself. If the legal entity has changed — for example, an entity merger or a transfer to a different subsidiary — that is a meaningful event that often happens around payment processor rebrands without being announced loudly. The legal entity is who you would sue if the relationship goes wrong; it is worth knowing whether that entity is the same as it was before.

Second, the fee schedule. Every rebrand creates an opportunity for the processor to introduce small fee changes attributed to “system updates” or “platform alignment.” Compare the line items on the post-rebrand statement to a statement from six months prior. Look specifically for new fees with names that did not exist before, fees that increased without notice, and fees that were combined or split in ways that obscure the change.

Third, the early termination provisions in the new welcome packet. Many processors send updated welcome materials around a rebrand. The materials often include “updated terms and conditions” the merchant is presumed to have accepted by continuing to use the service. If the post-rebrand terms make termination harder, more expensive, or longer in notice period than the original terms, the rebrand was the moment those changes took effect. Knowing what your ETF math looks like before the rebrand is the only way to recognize when it has changed afterward.

Fourth, the contract renewal cycle. Payment processor rebrands sometimes coincide with auto-renewal language that resets the contract clock. A merchant who was 18 months into a 36-month contract before the rebrand may find themselves on a fresh 36-month contract afterward, with the renewal date language obscured in the new welcome packet. The renewal cycle is the single most important date on a merchant agreement; verifying it has not been quietly extended is worth the 10 minutes it takes.

Legal entity in the fine print. Fee schedule vs. six months ago. Early termination provisions in any updated welcome packet. Contract renewal cycle. Ten minutes of statement attention catches whether the rebrand was paper-only or quietly reset terms underneath it.

The Conditions That Justify Switching, Payment Processor Rebrand or Not

The rebrand itself is not a reason to switch. The conditions that justify switching are the same before, during, and after a payment processor rebrand. Three signals matter most.

The first is effective rate. If your effective rate — the single number that tells you what you are actually paying across all your card volume — is materially higher than what a competitive processor would offer on interchange-plus pricing, switching makes sense. Most merchants on flat-rate or tiered pricing are paying 50 to 150 basis points more than they would on a transparent pricing model. The rebrand has nothing to do with that math; the math justifies switching regardless.

The second is service quality. If you cannot reach support when something goes wrong, if chargeback responses take days that should take hours, if your batch settlements are unpredictable, those are operational problems that switching can fix. Whether the processor recently went through a rebrand is irrelevant to whether the service is currently functional.

The third is contract trajectory. If your processor is in a phase of corporate change — a recent payment processor rebrand, a recent ownership change, a recent rate increase — the next 12 to 24 months tend to bring more changes, not fewer. The PE playbook describes the predictable arc: small fee additions, support cost reductions, contract enforcement intensification. If you are in early innings of that arc with your current processor, the case for switching to a smaller, owner-operated processor that is not on the same arc gets stronger over time, not weaker.

The discipline is to switch on the underlying economics, not on the brand noise. Merchants who switch every time their processor changes its logo end up making three or four switching decisions over a decade based on the wrong information. Merchants who never switch regardless of what happens around them end up paying for a decade of accumulated fee creep that never gets reset. The right cadence: review the statement carefully twice a year, switch when the numbers justify it, and ignore the brand events that do not change the numbers.

A rebrand is the right time to read your statement carefully — not the right time to switch. The trigger for switching is the effective rate, the service quality, and the contract trajectory. Those are the same signals that mattered before the rebrand and the same ones that will matter after.

Frequently Asked Questions

No, not on the rebrand alone. A rebrand changes the brand identity but not the merchant agreement, fee schedule, or early termination provisions. The right reasons to switch are the same before and after: an effective rate materially higher than competitive interchange-plus, service quality that has broken down, or a contract trajectory suggesting more changes coming. Use the rebrand as a prompt to read your statement carefully, not as a trigger to switch.

Three different archetypes. North is a cosmetic refresh — North American Bancard renamed itself in August 2024 with no change to ownership, contracts, or operations. Nuvei is a private-equity event — the brand stayed but Advent International took it private in April 2024 in a $6.3 billion buyout, which typically triggers fee creep and service degradation on a 12-to-24-month delay. Heartland is a brand sunset — Global Payments retired the name in December 2025 after nine years, dissolving the Heartland Merchant Bill of Rights along with it. Different corporate events; same merchant-side reality that contracts, fees, and termination provisions remain unchanged.

It was effectively dissolved when the Heartland brand was sunset in December 2025. The Bill of Rights had been a Heartland differentiator for two decades — a published commitment to transparent pricing and merchant-friendly terms. When the brand retired into Global Payments, the marketing artifact retired with it. Whether the underlying commitments persist as informal Global Payments policy is being answered case-by-case as merchants test it. Merchants who chose Heartland specifically for the Bill of Rights have a contract with Global Payments now and should not assume those commitments still bind.

PE buyouts of processors operate on a predictable schedule. The acquired company looks the same on the surface for the first 12 to 18 months. Merchant-side changes arrive on a delay: small fee additions (“network access fees,” “compliance fees,” “platform alignment fees”), support cuts that show up as longer hold times and harder escalation, contract enforcement intensifying (early termination penalties enforced more aggressively), and tougher chargeback positions. The Nuvei privatization in April 2024 is a textbook example. Merchants on Nuvei contracts in 2025 and 2026 should expect the playbook to play out — and recognize the changes as predictable consequences of the April 2024 transaction, not random degradation.

Four specific things. First, the legal entity name in the fine print — the brand at the top is marketing; the legal entity in the small text is who holds your contract, so verify it hasn’t changed. Second, the fee schedule — compare line items to a statement from six months prior, looking for new fees, fees that increased without notice, and fees combined or split to obscure the change. Third, the early termination provisions in any updated welcome packet — “updated terms and conditions” you’re presumed to have accepted by continuing service. Fourth, the renewal cycle — verify the rebrand didn’t quietly reset the clock onto a fresh 36-month contract. The rebrand is neutral; the statement that arrives after tells you whether anything changed underneath.

More on Payment Processor Rebrands and Corporate Change

Find Out What Actually Changed Beneath the New Logo

A rebrand is the easiest moment for a processor to introduce small fee changes that hide inside the rebrand noise. Send us your last processing statement. We will compare the post-rebrand line items against what they were six months ago, identify new fees that appeared without disclosure, and tell you whether your effective rate has crept up or held steady. The new logo is cosmetic. The line items underneath it are the only thing that determines what you actually pay.

Get Your Free Statement ReviewNo obligation • For merchants whose processor recently rebranded • Response within one business day