The Pricing Model With No Fixed Definition — What Pass-Through Pricing Actually Means When a Processor Quotes It

Pass-through pricing has no fixed industry definition. Some processors use it as a synonym for interchange-plus. Others use it to mean a more granular itemization with network fees broken out separately. Here’s what the term actually means when a processor quotes you “pass-through pricing” — and the three things to verify on the contract before you sign.

Why Pass-Through Pricing Means Different Things to Different Processors

Walk into a quote conversation with three different payment processors and ask each of them what “pass-through pricing” means. You will get three different answers. Sometimes meaningfully different. Sometimes only superficially different. Always different enough that comparing two pass-through quotes from two processors becomes an exercise in reading the fine print, not the headline rate.

The reason is that pass-through pricing is not a defined term in the payment processing industry. There is no governing body — not Visa, not Mastercard, not the card networks, not the Consumer Financial Protection Bureau — that says “this set of cost components must be passed through to qualify for the label.” Each processor uses the term as marketing language, and each defines it according to their own contract structure.

What this means in practice: a merchant comparing pass-through pricing from Processor A against pass-through pricing from Processor B may be comparing two structures that share a name and almost nothing else. Same label. Different math. Different total cost.

What Pass-Through Pricing Actually Means in Practice

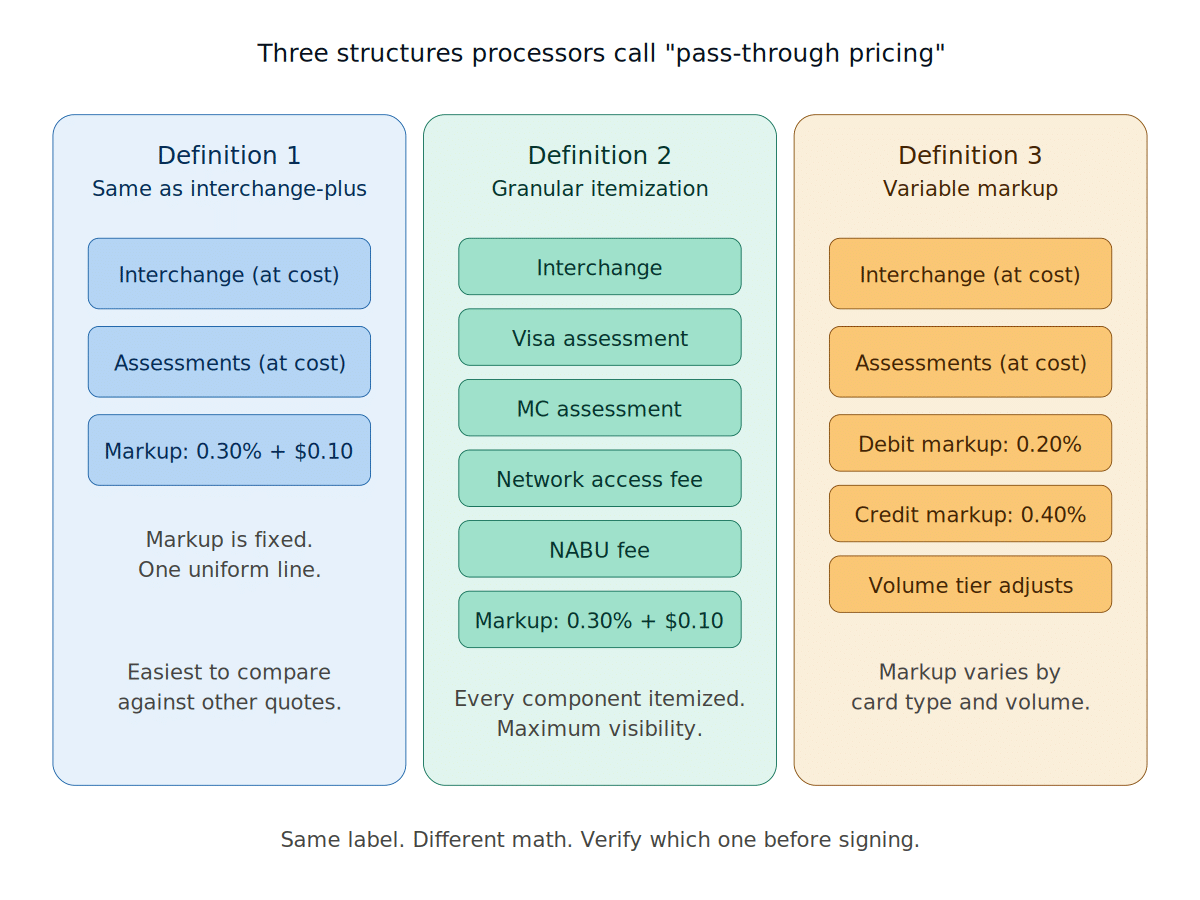

In the wild, pass-through pricing is used to describe one of three pricing structures. Knowing which one you are being offered is the difference between making an apples-to-apples comparison and being quoted three different things.

Definition One: Pass-Through as a Synonym for Interchange-Plus

The most common usage. Some processors say “pass-through pricing” and mean exactly what other processors call interchange-plus pricing: interchange and assessments pass through at cost, plus a fixed processor markup expressed as a percentage and per-transaction fee.

The format reads as interchange + 0.30% + $0.10 per transaction — identical to a standard interchange-plus quote. If a processor describes pass-through pricing this way, the term is purely cosmetic. They are quoting interchange-plus and calling it something else.

Definition Two: Pass-Through With Granular Fee Itemization

A more meaningful version. Some processors use “pass-through pricing” specifically to differentiate from standard interchange-plus by passing through every distinct cost layer separately: interchange, assessments, network fees, dues, NABU fees, monthly minimums — each itemized as a discrete line on the statement, with the processor’s markup also broken out as its own line.

The functional difference from interchange-plus: instead of the processor bundling assessments and network fees into a single “plus” component, they show every component separately. The total cost may or may not differ from a standard interchange-plus structure, but the visibility is greater. A merchant on this version of pass-through pricing can identify exactly what every dollar paid for.

Definition Three: Pass-Through With Variable Markup

The version most likely to confuse. Some processors describe pass-through pricing as a structure where the processor’s markup itself varies by card type or transaction volume — for example, 0.20% markup on debit, 0.40% on credit, with a sliding scale based on monthly volume. Interchange and assessments pass through at cost, but the “plus” component is not fixed.

This structure can produce competitive effective rates for merchants whose card mix sits in the favorable categories, but it is also the version that requires the most careful reading of the merchant agreement. The processor’s markup is no longer a single number you can multiply against your volume — it depends on what kind of cards your customers happen to use.

Three Things to Verify Before Signing a Pass-Through Pricing Agreement

Because pass-through pricing varies so widely between processors, comparing two quotes requires verifying the structural details before comparing the headline numbers. The three questions that resolve nearly all ambiguity:

A fixed markup (0.30% + $0.10 across all card types) is comparable to other interchange-plus quotes. A variable markup that changes by card type, transaction volume, or processing channel needs to be modeled against your actual card mix to produce a meaningful effective rate.

The phrase “pass through at cost” should specifically include interchange AND assessments AND network fees. Some processors pass through interchange but mark up assessments. Others pass through interchange and assessments but bundle network fees into the markup. Get the list of pass-through components in writing.

Statement fees, PCI compliance fees, monthly minimums, batch fees, and gateway fees are usually billed separately from the per-transaction pricing structure. A pass-through quote that looks competitive on the per-transaction line can produce a much higher effective rate once monthly fees are factored in. Ask for the complete fee schedule, not just the per-transaction terms.

How to Tell What Kind of Pass-Through Pricing You Actually Have

If you are already on pass-through pricing and not sure which version your processor uses, the statement tells you. Pull a recent processing statement and look for these specific markers:

The statement shows separate line items for “Visa Assessment Fee,” “Mastercard Assessment Fee,” “Visa Network Access Fee,” “NABU Fee,” and similar — each one a small percentage or per-transaction charge billed individually, not bundled into a single “fees” total.

The per-transaction markup line shows different rates for different card types or transaction categories. You may see “Debit Markup: 0.20% + $0.10” alongside “Credit Markup: 0.35% + $0.10” — distinct rates rather than a single uniform markup.

A single uniform markup line (“Discount Rate: 0.30% + $0.10”) applied across all transactions, with interchange categories listed but no separate breakdown of assessments or network fees beyond what a standard interchange-plus statement would show.

Pass-Through Pricing vs. the Three Other Pricing Models

Pass-through pricing exists alongside three other common pricing structures, and merchants comparing options should understand where pass-through fits relative to its siblings:

Pass-through vs. interchange-plus: often the same thing under different marketing language (Definition One). When meaningfully different (Definitions Two or Three), pass-through provides either greater fee transparency or variable markup. Effective cost depends on which version.

Pass-through vs. flat-rate pricing: pass-through (in any version) almost always produces a lower effective rate for merchants processing more than $10,000 per month, because flat-rate pricing pockets the spread between actual interchange cost and the bundled rate.

Pass-through vs. tiered pricing: tiered pricing groups transactions into qualified, mid-qualified, and non-qualified buckets that the processor controls. Pass-through pricing in any version is more transparent and almost always lower-cost than tiered pricing for merchants who process a normal mix of consumer and rewards cards.

The practical takeaway: if a processor is quoting pass-through pricing, the structure is almost certainly more competitive than tiered or flat-rate. The remaining question is whether it is meaningfully better than a standard interchange-plus quote, which is what the three verification questions above resolve.

Which Merchants Benefit Most From Pass-Through Pricing

Pass-through pricing — in any of its three forms — produces the largest savings for merchants whose card mix and transaction profile make standard interchange-plus or pass-through structures predictably cheaper than tiered or flat-rate alternatives.

Merchants processing $10,000+ per month with a mixed consumer and business card portfolio tend to see the cleanest savings under pass-through pricing. The granular itemization (Definition Two) provides additional accounting visibility for businesses that do their own statement reconciliation.

Merchants in B2B or wholesale sectors that process Level 2 or Level 3 data benefit from the variable markup version (Definition Three) because their card mix produces lower interchange categories that the markup structure can capture more efficiently.

Merchants processing under $10,000 per month often do better on a flat-rate structure where the simplicity is worth the higher effective rate, particularly if their card mix is debit-heavy and the flat-rate processor’s blended rate happens to land below their actual interchange cost.

The decision between pass-through and other pricing structures comes down to the same calculation in every case: divide your total monthly fees by your total monthly card volume to get the effective rate, then compare it against what each pricing structure would produce on the same volume.

Pass-through pricing decides how transparently you pay card interchange. ACH avoids interchange altogether. For B2B merchants whose customers are other businesses paying invoices, collecting by bank transfer carries no interchange to pass through — just a flat fee, typically under a dollar. A clean pass-through agreement is the right goal for card volume; for invoiced B2B revenue, ACH is often the cheaper rail before pricing model even enters the picture. The B2B credit-card-vs-ACH cost gap typically lands at $200-$300 per $10K invoice.

Frequently Asked Questions

Sometimes — “pass-through pricing” is not a defined industry term, so there’s no governing body specifying what must pass through to qualify. Some processors use it as a synonym for interchange-plus (interchange and assessments at cost, plus a fixed percentage and per-transaction markup). Others use it for granular fee itemization, where every cost layer — interchange, assessments, network fees, dues, NABU fees — is listed separately. A third group uses it for variable markup that changes by card type, volume, or channel. Same label, three different structures.

Three questions resolve nearly all ambiguity. Is the markup fixed or variable? A fixed 0.30% + $0.10 across all card types is comparable to a standard interchange-plus quote; a markup that changes by card type or volume must be modeled against your actual mix. What passes through at cost? It should include interchange AND assessments AND network fees — get the list in writing, since some pass through interchange but mark up assessments, and others bundle network fees into the markup. Are there fees outside the pass-through structure? Statement, PCI, monthly minimum, batch, and gateway fees are usually billed separately and can offset competitive per-transaction pricing.

The statement tells you. Granular pass-through shows separate line items — “Visa Assessment Fee,” “Mastercard Assessment Fee,” “Visa Network Access Fee,” “NABU Fee” — each billed individually rather than bundled. Variable markup shows different rates by card type (“Debit Markup: 0.20% + $0.10” alongside “Credit Markup: 0.35% + $0.10”). Standard interchange-plus rebranded as pass-through shows a single uniform markup line (“Discount Rate: 0.30% + $0.10”) across all transactions, with no separate breakdown of assessments or network fees beyond a standard interchange-plus statement.

Above $10,000/month, almost always yes. Flat-rate pricing pockets the spread between actual interchange cost and the bundled rate, so any pass-through structure produces a lower effective rate at scale. Tiered pricing groups transactions into qualified, mid-qualified, and non-qualified buckets the processor controls — pass-through is more transparent and almost always lower-cost for a normal consumer/rewards mix. Merchants under $10,000/month sometimes do better on flat-rate where the simplicity is worth the higher rate, particularly if their mix is debit-heavy and the blended rate lands below their actual interchange cost.

Merchants over $10,000/month with a mixed consumer and business card portfolio see the cleanest savings. The granular itemization version adds accounting visibility for businesses doing their own statement reconciliation. B2B or wholesale merchants processing Level 2/Level 3 data benefit from the variable markup version, since their lower interchange categories are captured more efficiently. The decision comes down to the same calculation every time: divide total monthly fees by total card volume for your effective rate, then compare against what each structure would produce on the same volume.

Companion references for pricing model comparison

Have a Pass-Through Pricing Quote? We Will Tell You Which Version You Are Actually Being Offered.

Send us the pricing schedule from any pass-through quote you have received. We will identify which of the three versions it is, flag any clauses that produce variable cost, and run the effective rate it would produce on your actual card volume. The review takes 1-2 business days and produces a one-page advisor-format summary you can compare directly against any other quote.

Request a Free Statement ReviewNo obligation • Advisor-format deliverable • Response within one business day