Convenience Fee

What Is a Convenience Fee? Definition & Guide

A convenience fee is a card-brand-sanctioned charge assessed when a payor uses an alternative payment channel — such as an online portal or automated phone system — instead of the standard in-person or mail-in method. Card brand rules vary by channel, jurisdiction, and entity type. See Visa’s rules for this fee type for full requirements.

What is a convenience fee? It is a card-brand-approved charge that government agencies, schools, and utilities can assess when a payor uses a card through an alternative channel — like an online payment portal — instead of the standard method such as a counter window or mail. When structured correctly, it passes the entire processing cost to the payor — resulting in zero net cost to the organization.

Unlike a credit card surcharge, which applies to credit card transactions broadly, a government convenience fee applies specifically to the use of a non-standard payment channel — such as an online payment convenience fee portal. Only qualifying entity types may use it — government agencies, educational institutions, and certain utilities. Private businesses cannot use this structure under card brand rules.

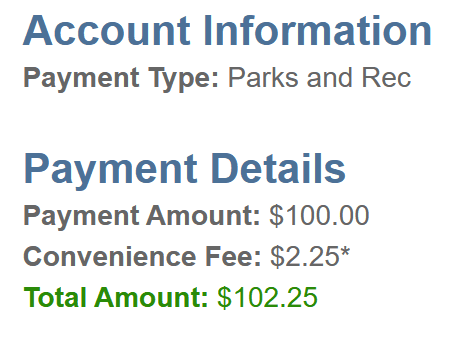

Here is how it works for a qualifying government entity:

The key compliance requirement: the payor must be shown the exact amount before confirming payment and must have access to a no-fee alternative method (mail-in, in-person, ACH).

Card brand rules limit this charge to specific entity types. Qualifying organizations include:

- Federal, state, county, and local government agencies

- Public K–12 school districts, charter schools, and state universities

- Municipal utilities (water, electric, sewer, gas)

- Certain rent, insurance, and telecom billing portals

Does not qualify: Private businesses, retailers, restaurants, and most commercial service providers cannot use this structure. These organizations should evaluate a surcharge program or cash discount program instead.

These two fee types are frequently confused but operate under entirely different rules. Card brand convenience fee rules govern which entities qualify and how the charge must be disclosed:

| Feature | Convenience Fee | Surcharge |

|---|---|---|

| Who can use it | Government, schools, utilities | Most businesses |

| Applies to | Alternative payment channel | Credit card transactions |

| Card types | Any card type | Credit cards only |

| State restrictions | Varies by jurisdiction | Some states prohibit |

It is a charge for using an alternative payment channel — typically an online portal or automated phone system. Only qualifying government agencies, educational institutions, and utilities may use it under card brand rules.

This charge is permitted for government entities, educational institutions, and certain utilities paying via a non-standard channel. Private businesses generally cannot use this structure.

In most cases, yes. The fee is borne by the citizen, so the government nets the full payment amount at no processing cost. This is most common in tax collection, utility billing, and court payments. For very low-volume entities, a small monthly fee or equipment cost may apply — but for most government organizations, the program runs at zero net cost.

Yes. A properly structured program results in zero net processing cost for the organization, since the full amount is passed to the payor.

Government Entities Can Legally Pass Card Costs to Cardholders. The Card Brand Rules Are Specific.

Send us your last processing statement. We will assess whether convenience fee implementation fits your transaction profile, walk through the specific card-brand and state-level disclosure requirements, and show you what implementation would look like at your volume.

Request a Free Statement ReviewNo obligation • For glossary readers comparing pricing models and processor options • Response within one business day