Real Estate Tax Payments: Choosing Between an API and Bill Presentment

The Real Estate Tax Payments Decision Nobody Explains in the Demo

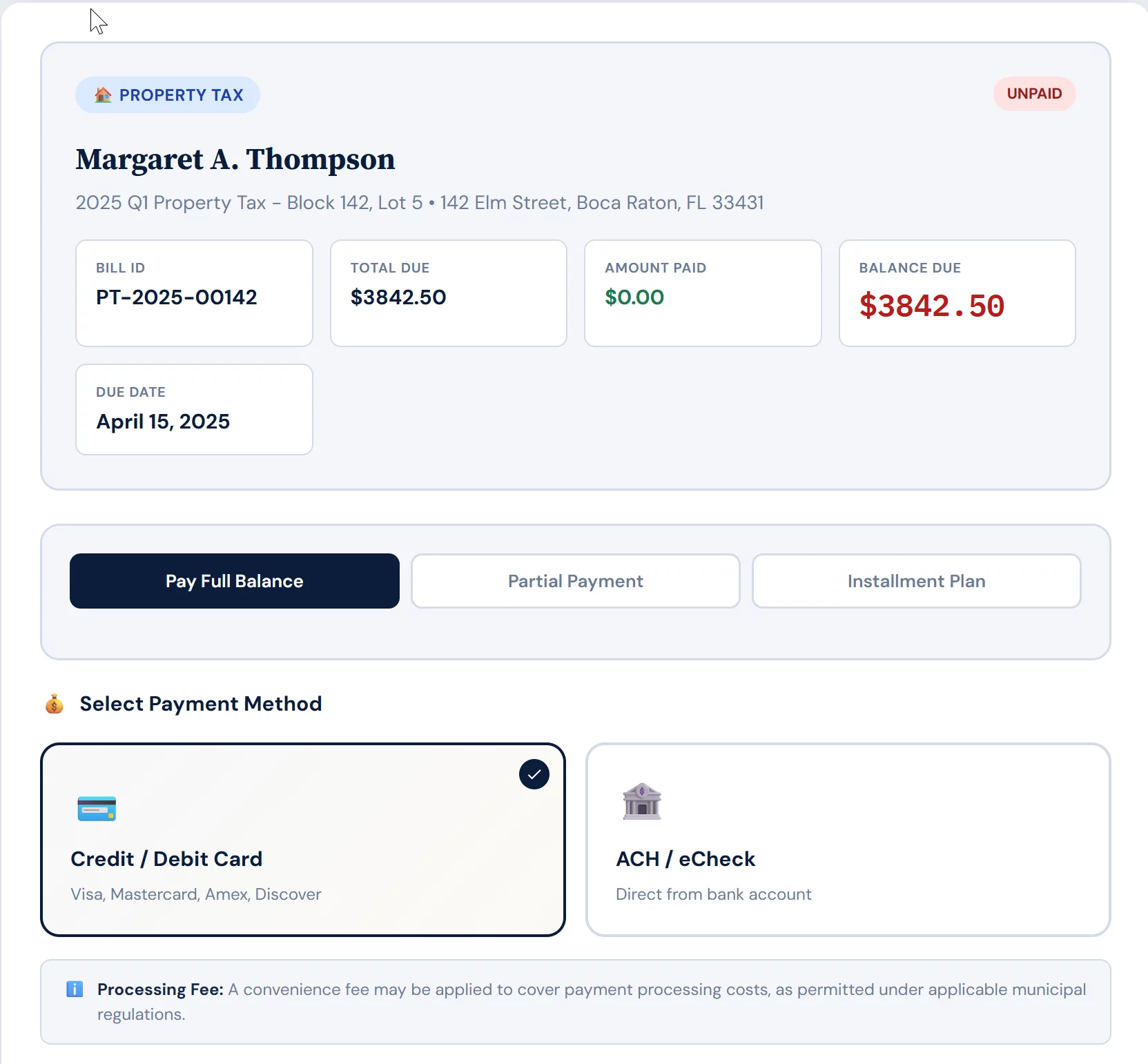

When a county or municipality decides to accept real estate tax payments online, every vendor demo points at the same thing: the citizen-facing portal — the logo, the search box, the receipt screen. That part matters, but it isn’t the decision that determines your staff’s workload or whether your books close cleanly at month-end. The quieter, more consequential choice is how the payment system connects to your tax and billing system. There are two models, and treasurers and finance directors are usually asked to sign off on one without anyone naming the trade-off. (A third option, a no-integration standalone payment portal, fits offices that cannot integrate either system.)

The two models are bill presentment — you hand your tax roll to a portal and reconcile payments back by file — and API integration — the payment system and your tax system stay wired together in real time. The short version: bill presentment is batch and periodic; an API is real-time and continuous. Both can take a taxpayer’s money. They differ entirely in what happens to the data on either side of that payment, and that difference is where real estate tax payment processing either saves your office time or quietly creates a reconciliation problem you’ll be untangling at audit. When those gaps surface as taxpayer payment complaints, how the office handles them matters as much as the rail.

The portal is the part residents see; the integration is the part your office lives with. Posting speed, balance accuracy, reconciliation labor, and how clean the general ledger looks all trace back to this one architectural choice — not to which portal has the nicer interface.

Bill Presentment: Export the Roll, Reconcile by File

In a bill presentment model — sometimes called electronic bill presentment and payment, or EBPP — your office exports the real estate tax roll to the payment portal: parcels, owners, balances, and due dates, usually as a scheduled file. Taxpayers look up their parcel, see the presented amount, and pay it. Payments then come back to you as a batch settlement and reconciliation file that your staff imports into the tax system on a schedule, often overnight. It’s a loosely coupled, periodic arrangement: here are the bills, collect against them, reconcile afterward.

That model fits real estate taxes more naturally than it fits almost anything else, because a real estate tax bill is a fixed annual amount with a known due date — it doesn’t move between billings. Presentment is also the realistic option when your tax or CAMA system is older and can only export and import files rather than expose live connections. It’s the same plumbing mortgage servicers already rely on when they pull a bulk escrow file to pay thousands of parcels at once. The cost is that reconciliation is a recurring, staff-driven task, and the presented balance is a snapshot — accurate only as of the last file you sent.

You are presenting a copy of the bills as they stood when you exported them. Between exports, that copy is frozen. For a fixed annual real estate tax bill that’s fine; for anything where the number can change after the file goes out, it’s the source of most of the trouble below.

API Integration: One Live Connection, Instant Posting

An API model wires the payment system directly to your tax system. When a taxpayer starts a payment, the integration pulls the current balance straight from the tax roll at that moment, takes the payment, and posts it back to the parcel immediately. There’s no file to export, no file to import, and no overnight wait — the payment and the record update in one motion. Modern county tax, CAMA, and customer-information systems increasingly expose this kind of real-time connection through pre-built connectors, which is what makes the live model practical without custom development.

Real-time integration earns its keep wherever the number can change or the timing matters. Delinquent real estate taxes accrue penalties and interest; a live balance pull always quotes today’s amount due, while a parcel where someone needs to see the payment immediately — to release a hold, clear a lien, or hand a taxpayer a definitive receipt — can’t wait for a batch. The trade-off is that API integration is more upfront work to stand up and depends on a tax system that can actually expose the connection. What you get in return is near-zero ongoing reconciliation: real estate tax payments, adjustments, and refunds sync to the billing and accounting records on their own.

Always-current balances, instant posting, definitive receipts, and reconciliation that mostly handles itself — which is what shrinks the month-end close and the audit-season scramble. You trade a heavier setup for far less recurring manual work.

How to Actually Choose Between Them

For most offices the decision starts with a gating question: what will your tax or CAMA system actually support? If it can only export and import files, bill presentment is effectively your answer regardless of preference; if it can expose a live, real-time connection, both models are genuinely on the table. That single capability often makes — or forecloses — the choice before any other factor comes into play, so it is worth confirming with your system vendor early rather than after a portal demo has already won you over.

When you do have a real choice, the most important differentiator is whether the balance moves. A clean annual real estate tax bill paid before its due date is a fixed number, and bill presentment handles it perfectly well. But the moment penalties and interest start accruing on delinquencies, a presented balance goes stale between file exports — and a taxpayer can pay yesterday’s amount in good faith, leaving your staff to chase the shortfall. After that it comes down to practical trade-offs: does posting speed matter — does anyone need to see the payment the instant it’s made — and how much reconciliation labor can your office absorb, given that batch reconciliation is a recurring cost while real-time sync largely removes it?

- Delinquent parcels accruing daily penalty and interest.

- Payment plans or partial payments that change the balance mid-cycle.

- Adjustments, abatements, or corrections issued after the last file export.

- Any case where a taxpayer could reasonably pay a number that’s no longer current.

If your real estate tax payments include much of the above, the periodic snapshot of bill presentment is working against you, and a live balance pull is the safer architecture.

Who Pays for It — and Why Government Has an Edge

The fee on real estate tax payments worries finance directors most, and here government is in a genuinely better position than a private business. A private merchant faces surcharge caps and outright state bans on passing card costs to customers. Government, tax, and education payments sit in a permitted category: through the Mastercard Government and Education convenience-fee program and Visa’s service-fee rules for those categories, a county can pass the card cost to the taxpayer who chooses to pay by card, charged as a separate, clearly disclosed service or convenience fee. The practical result is that your office can accept cards at little to no cost to itself — the payer who wants the convenience covers it, while taxpayers who prefer to avoid the fee can still pay by eCheck or ACH, typically for a small flat amount or free.

That doesn’t make the cost side a non-issue. The fee still has to be assessed and disclosed correctly, and the specifics vary by state and by card network. The mechanics of permitted government fees — what’s allowed, how it’s disclosed, and where it differs from a surcharge — are worth understanding before you commit; our breakdown of convenience fees on government payments covers the detail, and the broader options for the public sector live under government payment processing. For a neutral, finance-office view of the same decisions — vendor selection, fees, and PCI — the GFOA’s best practice on accepting payment cards is a useful reference.

You don’t have to choose in the abstract. We’ve developed customized solutions for both bill presentment and real-time API integration, so you can watch each one run against a live tax-payment flow before deciding which fits your system. Contact us today for a demo: (833) 382-1992 or hello@brooksidepayments.com.

Frequently Asked Questions

Generally, yes. Government and tax payments are a permitted category under the Mastercard Government and Education convenience-fee program and Visa’s service-fee rules, so the card cost can be passed to the taxpayer who chooses to pay by card — charged as a separate, clearly disclosed service or convenience fee rather than embedded in the tax amount. The specifics vary by state and processor, so confirm the rules that apply to your jurisdiction before you turn it on.

A real-time, always-on view of every transaction. Your office gets a secure online payment portal, available 24/7, where you can look up any payment or batch as it posts and export the records to Excel — so reconciling card and eCheck batches against your bank deposits and your general ledger is a quick lookup rather than an end-of-month reconstruction.

Settlement — the transfer of collected funds into your government’s bank account — typically lands the next business day. The taxpayer’s payment is authorized instantly, but the money actually moves at settlement: once the day’s transactions batch and close, funds generally deposit the following business day, subject to the processor’s cutoff time and your acquiring bank’s funding schedule. ACH and eCheck payments settle on a comparable next-business-day cycle.

Yes. Both models work best for any bill where the exact amount is known beforehand. Real estate taxes are the clearest example, and utilities, court fees, and licenses are common ones too — but other fixed-amount obligations can run through the same setup. The API-versus-bill-presentment choice stays the same: a fixed, known amount suits bill presentment, while a balance that changes or needs instant posting favors an API.

Before You Sign Off on a Payment Setup

Map the right real estate tax payment setup — before the vendor maps it for you.

Tell us how your office collects real estate taxes today and which tax or CAMA system you run, and we’ll lay out whether an API integration or bill presentment fits your situation, how to pass the card fee to payers correctly, and what reconciliation looks like either way — no obligation, no sales pressure. A short conversation now is cheaper than a reconciliation problem at audit.

Review Our Tax Payment SetupNo obligation • No pressure • Response within one business day