Franchise Payment Processing: Who Controls the Rate Across Your Locations

Franchise payment processing has a problem no single-location business faces: the decision about who processes your cards, and at what rate, is split between corporate and the individual owner — and the fees get lost in the gap. A franchisee signs an agreement built around brand standards and a point-of-sale system, and the processing rate rides along inside it, rarely shopped and rarely questioned. Multiply a small overpay across a dozen locations and it becomes one of the largest uncontrolled line items in the whole operation.

This is a guide to how franchise payment processing actually works — who chooses the processor, where the rate hides, and where a franchisee or franchisor can still cut the cost. For the broader picture, our overview of retail merchant services covers the single-location fundamentals this builds on.

Who Actually Chooses the Processor in Franchise Payment Processing

The first question in any franchise payment processing setup is who controls the processor, because it determines whether there is any room to negotiate at all. There are three common arrangements.

Corporate mandates the processor — every location runs the brand’s chosen processor at a set program rate; the franchisee has no lever. Corporate mandates the POS but not the processor — the software is fixed, but the merchant account behind it can be shopped; this is the common case, and the one where savings live. The franchisee chooses freely — full control, and full responsibility to not overpay.

Most franchisees assume they are in the first bucket when they are actually in the second — locked to a POS but free to place the processor. Confirming which model your agreement actually specifies is the first move, because it decides everything that follows.

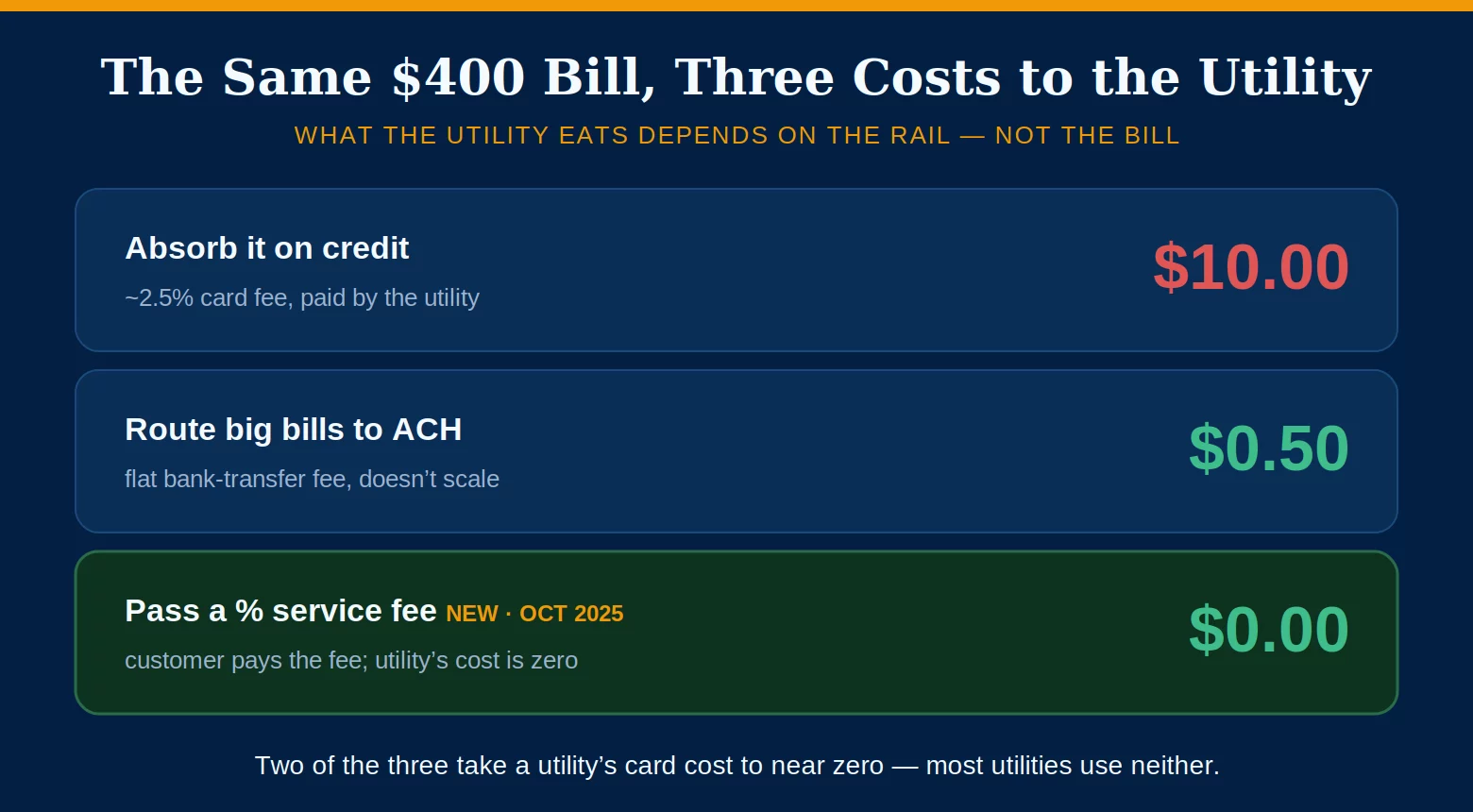

What Corporate Negotiated vs. What You Pay

Franchisors often negotiate a national processing program and present it as a benefit. Sometimes it is. But a corporate program is priced for the average location, and it frequently carries a bundled or tiered rate that buries the markup — so a high-volume franchisee subsidizes the system while believing they are getting a group discount.

A corporate program locked at a flat 2.6% can cost a busy location far more than interchange-plus pricing would, where the true interchange is exposed and only a small transparent markup sits on top. Ask what pricing model the program actually uses before assuming it is competitive — “negotiated by corporate” and “lowest cost for my location” are not the same sentence.

Some corporate programs pay the franchisor a cut of every location’s processing fees — a revenue stream for headquarters, not a discount for you, and a reason a “mandated” program can sit above market. If your franchise payment processing runs through a corporate deal, ask whether corporate receives a rebate on your volume. The answer reframes whether the program is a benefit or a markup on your franchisee fees.

Multi-Location Reconciliation

Beyond the rate, franchise payment processing carries an operational cost that single locations never see: reconciling deposits, fees, and disputes across many stores. When each location settles separately, matching card batches to bank deposits and pulling a clean picture of total processing cost becomes a monthly slog — and hidden fees survive precisely because no one is looking across the whole set.

This is where franchise merchant services differ most from a standalone shop. A single owner reads one statement; a multi-location operator is reconciling ten, each with its own batch timing, adjustments, and chargeback trickle. Quiet rate creep hides in that volume, and by the time a bookkeeper flags a location drifting upward, months of overpay have already cleared.

A processor that rolls every location into one dashboard — deposits, effective rate, and chargebacks visible together — turns reconciliation from a headache into a control. It also surfaces the outlier location paying too much, which a per-store statement pile hides. For multi-location payment processing, the reporting structure is worth as much as the rate.

Where a Franchisee Can Actually Cut Costs

Assuming the processor is negotiable — the common case — the same levers that work anywhere apply, sharpened by volume across locations.

Move to interchange-plus pricing so the markup is visible and shoppable; submit Level 2 and Level 3 data if the franchise sells B2B or handles large tickets, to drop the interchange itself; route large or recurring payments to ACH; and consolidate locations under one agreement for reporting and negotiating leverage. Each is small on one store and significant across ten.

The through-line of franchise payment processing is that the cost is controllable far more often than franchisees assume — the trap is treating the corporate program as fixed when the merchant account behind the mandated POS is usually yours to place.

Frequently Asked Questions

Sometimes, but less often than franchisees assume. Many agreements mandate the point-of-sale system while leaving the merchant account — the processor behind it — open to your choice. Read what your franchise agreement actually requires; if only the POS is specified, you are usually free to shop the processing rate — the single highest-leverage move in franchise payment processing, and the one most owners never make.

No. A national program is priced for the average location and often uses a bundled or tiered rate that hides the markup. A high-volume franchisee can frequently do better on interchange-plus pricing. Compare the program’s effective rate against a transparent quote before assuming the group rate wins.

The cleanest setup consolidates locations under one processor with unified reporting — deposits, effective rate, and chargebacks visible across every store — while still funding each location’s account correctly. Consolidated reporting is what surfaces the outlier store overpaying and gives the group negotiating leverage.

Build out the multi-location payment stack

Send Us a Statement. We’ll Find the Overpay.

Send Brookside a processing statement from any location and we’ll calculate the true effective rate, compare it against your corporate program, and show what interchange-plus and consolidated reporting would save across your footprint. Learn more about payment processing consumer protections from the CFPB.

Get a Free Rate ReviewNo obligation • No pressure • Response within one business day