Reduce Utility Payment Processing Costs: Three Levers and the October 2025 Rule

Utilities have quietly kept absorbing card-processing fees that other billers stopped eating years ago — and a card-network rule change in October 2025 just widened the options to reduce utility payment processing costs. Water districts, co-ops, and municipal utilities running thousands of recurring bills a month are often on a flat-rate or software-bundled processor that quietly marks up every card payment, while a newer program now lets them move that cost off their own books entirely.

This is a practical guide to the three levers that actually lower a utility’s card cost — and the one that backfires on large bills. For the broader vertical, start with our overview of utility payment processing; this page is specifically about cutting the fee.

How to Reduce Utility Payment Processing Costs

There are only three real ways to reduce utility payment processing costs, and most utilities are using none of them. Each attacks a different part of the bill.

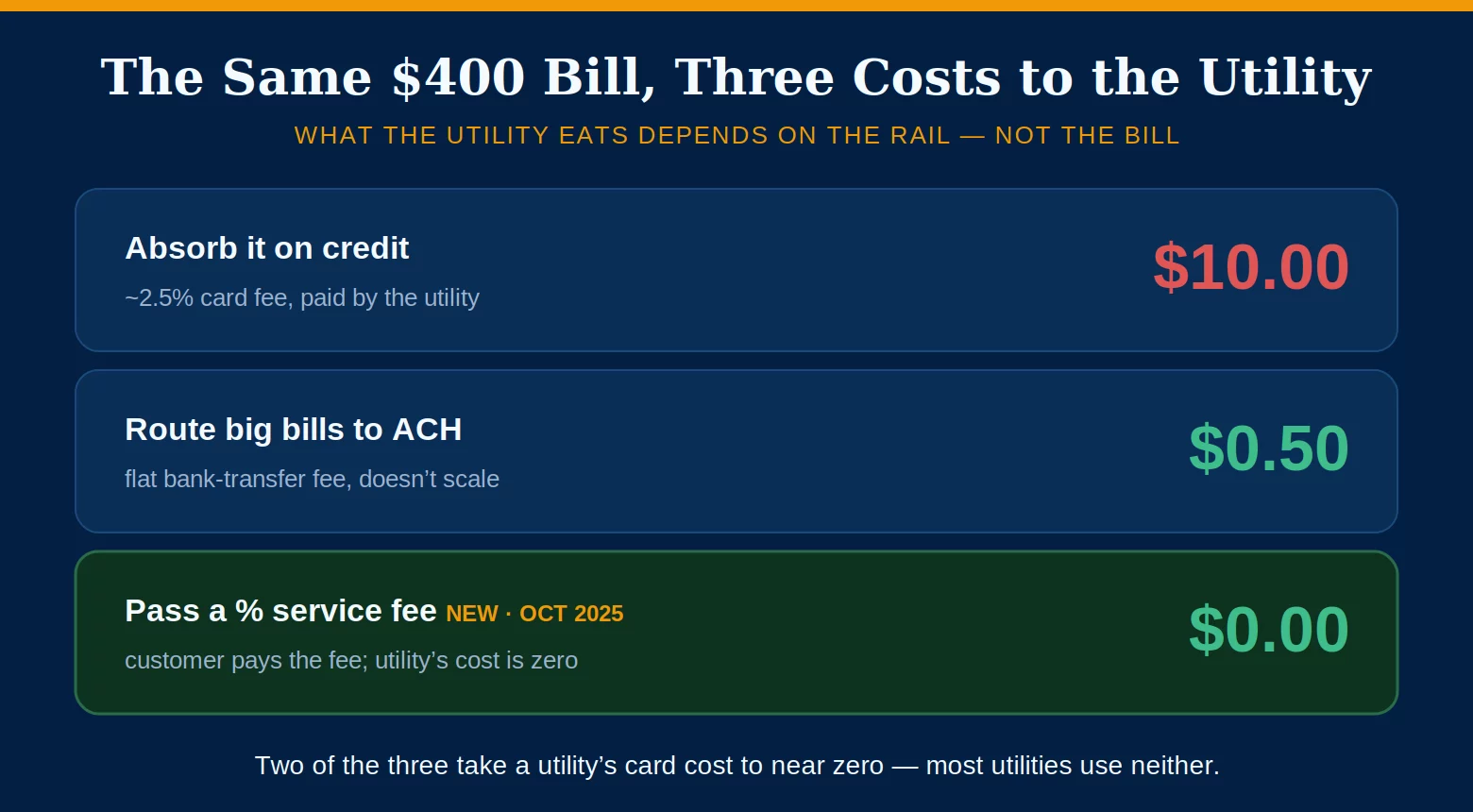

Most utilities sit on a flat retail rate or a billing-software bundle that never gets shopped. Interchange-plus pricing exposes the true cost and strips the padded markup, and qualifying utility and government transactions for Level 2/Level 3 data can drop the interchange itself. This is the single biggest lever on the card cost you keep.

Card fees scale with the bill; a bank transfer does not. On a large quarterly or commercial utility bill, ACH at a low flat cost beats any percentage card rate by a wide margin, so steering high-dollar and autopay customers to ACH removes the most expensive transactions from the card mix entirely.

The third lever is the one that changed in October 2025 — the most direct way to reduce utility payment processing costs, taking a utility’s card cost to nearly zero.

The October 2025 Rule: Utilities Can Now Pass the Fee

Effective October 18, 2025, Visa expanded its Government, Higher Education, and Utility Payment Program to include utilities (merchant category 4900), and simplified the old two-account setup into a single combinable transaction. Under this program a qualifying utility can assess a utility service fee on card payments — and unlike a plain convenience fee, that service fee can be a percentage, not just a flat amount.

A convenience fee must be a flat dollar amount. The service fee under the utility program can be a percentage, which is what makes it work on utility bills of every size. When the customer pays the service fee, the utility’s own processing cost drops toward zero. See what a convenience fee is and how fee programs are structured.

This is the profitable path to reduce utility payment processing costs, and the one worth setting up correctly, because the older flat-fee approach quietly loses money on exactly the bills utilities care about most.

Why a Flat Fee Backfires on Large Bills

The instinct is to charge a small flat fee — the roughly $2.55 you see on debit tax payments. On a small bill that works. On a large utility bill it goes underwater, and understanding why is central to how you reduce utility payment processing costs without creating a loss.

Card-network assessment fees run about 0.10% to 0.15% of the transaction and are non-negotiable, on top of interchange. On a $600 utility bill, the assessment alone is roughly $0.60–$0.90 — but on a $3,000 balance it is $3–$4.50, which already exceeds a small flat fee before interchange or the processor’s own cost. A flat fee that ignores bill size means someone absorbs the shortfall on every large payment. A percentage service fee scales with the bill and never inverts.

So the lesson is not “pass a flat fee.” It is: absorb small card costs where a flat fee makes sense, route big bills to ACH, and use the percentage service fee where you want card acceptance without eating the cost. Match the structure to the bill.

What to Put in Place

Once the model is chosen, the cost outcome comes down to how the account is built. To reduce utility payment processing costs in practice, confirm five things:

Interchange-plus pricing (not a bundled flat rate); Level 2/Level 3 data enabled so government and utility transactions qualify for the lower interchange; an ACH rail for large and autopay bills; a compliant percentage service fee under the Visa utility program if you want card acceptance at no cost to the utility; and settlement timing that funds your operating account on your schedule.

A utility that gets all five right rarely pays more than a fraction of what a bundled software processor was quietly charging — and often pays nothing at all on the card side once the service fee is passed correctly. Done together, those five steps reduce utility payment processing costs as far as the model allows.

Frequently Asked Questions

As of October 18, 2025, utilities (MCC 4900) qualify for Visa’s service fee program alongside government and higher education, and the service fee can be a percentage. Whether and how you can apply it still depends on your state’s rules and the card-network requirements for your setup, so confirm the current requirements for your jurisdiction before turning it on.

For utilities, a percentage service fee is the durable choice. A small flat fee works on low bills but goes underwater on large ones, because percentage-based network assessments and interchange exceed the flat amount as the bill grows. The percentage service fee scales with the payment and never inverts.

ACH bank transfer is the lowest-cost rail for large and recurring utility bills, since its flat cost does not scale with the balance. For card acceptance, interchange-plus pricing with Level 3 data on the base rate, plus a percentage service fee passed to the customer, is how utilities keep their own card cost near zero — the combination that reduces utility payment processing costs the most.

Keep working the utility payment stack

Send Us a Statement. We’ll Show You What You’re Overpaying.

Send Brookside a recent processing statement and we’ll calculate your true effective rate, flag the Level 3 and ACH savings you’re missing, and show you whether the new percentage service fee can take your card cost to zero. Learn more about payment processing consumer protections from the CFPB.

Get a Free Utility Cost ReviewNo obligation • No pressure • Response within one business day