Junk Removal Payment Processing: Why the Bundled Rate Skims Every Load

Why Junk Haulers Lose Money on Every Card Sale

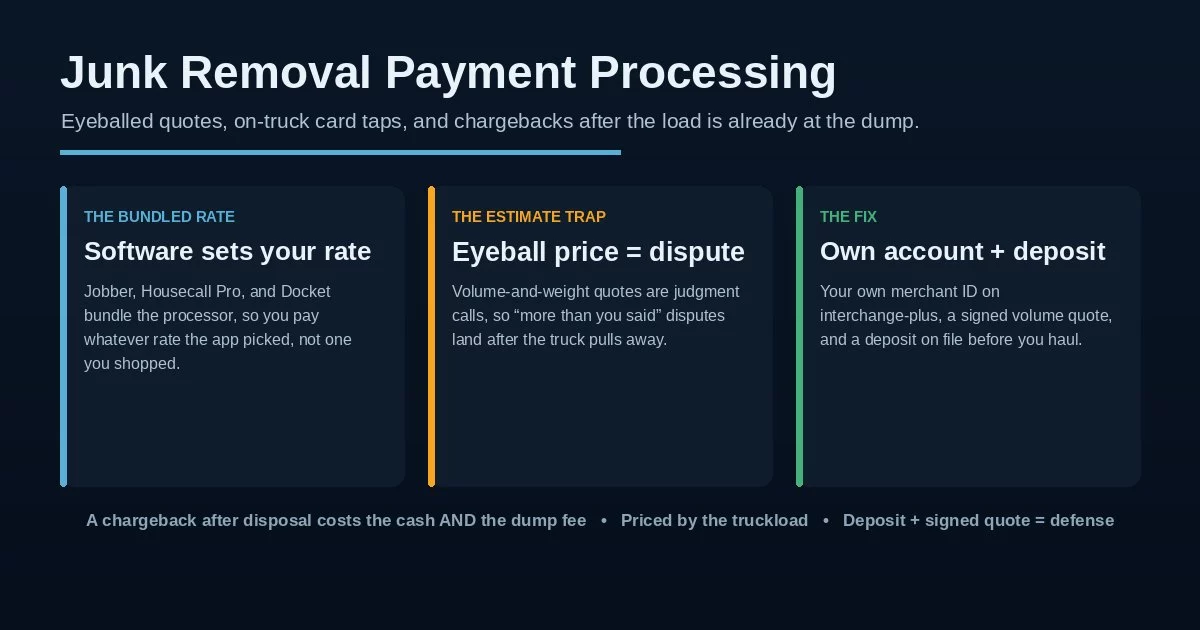

Junk removal payment processing usually arrives as an afterthought. You sign up for a hauling platform — Jobber, Housecall Pro, Docket — because you need scheduling, routing, and invoicing, and the card processing comes bundled in. It works, so you never look closely. Then you notice that 2–4% comes off the top of every load, surprise “statement” or “PCI” fees show up, and the rate you’re paying is one you never actually shopped — the software picked it for you.

On a business built around fast, one-and-done jobs, that adds up quietly. A few percent on a $350 truckload, job after job, is a real chunk of a thin-margin operation — money that could cover fuel, a crew hour, or the next dump run. The processing came packaged with the software, so it feels like a fixed cost of doing business. It isn’t. A junk removal merchant account you actually control is a separate decision from the app you schedule with, and treating it that way is where the savings start. Junk removal payment processing is its own line item, and it deserves its own decision.

When the processor is bundled into your hauling software, the markup is set for you and buried in a flat rate. It’s convenient, but convenience is the whole pricing strategy — there’s no incentive to give a one-truck operator a competitive rate when switching feels like switching your whole operating system. Junk removal credit card processing should be priced on its own merits, not bundled out of sight.

When You Eyeball the Price, You Invite the Dispute

Here’s the risk built into how junk removal is priced. Jobs are quoted by the truckload — fractions of how full the truck gets — or by weight or time, which means the final number is a judgment call made on the spot. That’s normal for the trade, but it’s also exactly what fuels disputes: a customer who agreed to “a half load” in the moment looks at the card charge later and decides it was more than they pictured, and reaches for a chargeback. The work was fair; the pricing was verbal; and now it’s your word against theirs.

Those disputes do more damage than the single refund. Each one counts toward the chargeback ratio thresholds the card networks watch — roughly 1% for Visa — and a run of them in a busy month can tip the account into a monitoring program or a freeze, even when you’d win most of them on the merits. The defense is to take the judgment call off the table: a written, signed-off volume quote before you load a single item turns “that’s more than you said” into a documented agreement. Junk removal payment processing that survives is built around that habit, not around hoping customers remember the number.

A chargeback isn’t just a reversed sale here. By the time it lands, you’ve already paid the crew, burned the fuel, and run the load to the landfill. You can’t un-haul a hot tub. So a single disputed job costs you the payment, the labor, and the disposal — and still dings the ratio that keeps your account open.

A Chargeback After the Junk Is Already Gone

This is the part that makes junk hauling payment processing different from ordinary retail. In most businesses, a chargeback means you refund the sale and, often, get the product back. You can’t. The whole service is that the stuff is gone — hauled away, tipped at the transfer station, dump fee paid. When a customer disputes after the fact, there is nothing to return and nothing to resell. You eat the payment, the labor, the fuel, and the disposal cost, all at once.

That asymmetry is why documentation matters more here than almost anywhere. Photos of the load before and after, a signed volume agreement, and a deposit taken at booking are what turn a “the goods are gone, I can’t prove anything” situation into a winnable case. The card networks let a documented merchant fight back — tools like Compelling Evidence 3.0 exist for exactly this — but only if the evidence was captured before the truck left. A junk removal merchant account set up right bakes that capture into the job, so the disposal sting never becomes a total loss. That is the heart of junk hauling payment processing done right.

Retail can absorb a dispute because the item often comes back. Hauling can’t — the value left on the truck. Treat every job as if it might be disputed: deposit at booking, signed quote before loading, photos at completion. The five minutes of documentation is cheaper than one lost load.

What the Right Junk-Removal Setup Looks Like

The durable answer for junk removal payment processing is a dedicated junk removal merchant account that’s separate from your scheduling software — your own merchant ID on interchange-plus pricing, so the markup is a visible line you can audit instead of a blended rate the app set. You can keep the software you like for dispatch and routing and still route the actual card processing through an account you control; the two don’t have to be the same vendor. If you’re currently on a bundled platform rate, our breakdown of reducing Jobber payment processing fees shows the mechanics, and an effective rate calculator tells you your true all-in cost so you can compare honestly.

The operational half is what kills the disputes: a deposit and a signed volume quote at booking, taken on a card kept on file, with the balance charged on completion. That sequence — supported by every major hauling platform — means the customer agreed to the price and the method before you ever lifted anything. For in-person residential jobs, some haulers also lower their net card cost with a compliant cash discount or dual-pricing program; both are options worth understanding rather than defaulting into the platform’s flat rate.

Your own merchant ID on interchange-plus you can audit, the freedom to keep your scheduling app without its payment markup, a deposit-and-signed-quote workflow that documents agreement before the haul, and dispute tools that win the cases you should. You stop renting your revenue to a bundled rate and stop losing whole loads to after-the-fact disputes.

Staying Approved — and What to Ask Before You Sign

Keeping the account healthy comes down to the same discipline that lowers disputes: deposit at booking, signed volume quote before loading, photos at completion, and an itemized receipt. When a customer does dispute, the chargeback process rewards the hauler who can show an agreed price and proof of work — and that same paper trail keeps friendly fraud from sticking. Seasonal swings matter too: moving season and spring cleanouts spike volume, and a sudden jump on a thin processing history is a classic trigger for a processor to hold funds — a seasonal merchant account structure anticipates it.

Whether you’re leaving a bundled platform rate or opening a first real account, the questions are concrete. Will you get your own merchant ID on interchange-plus, with the markup itemized — or a flat rate set by the software? Can you keep your scheduling app and still move the card processing? Does the account support deposits and card-on-file so you can document agreement at booking? What’s the reserve structure, and how does it treat a seasonal spike? And read the merchant agreement closely — term length, early-termination fee, and reserve language matter most when one busy month spikes both your volume and your disputes. Junk removal payment processing handled this way stops skimming your loads and starts behaving like the tool it should be. For the broader field-service picture, our home services payment processing guide covers the trades next door.

Frequently Asked Questions

Because the processor is bundled into the software and the rate is set for you, not shopped. Platforms like Jobber, Housecall Pro, and Docket package card processing with scheduling and invoicing at a convenient flat rate — convenient, but there’s no pressure to give a one-truck operator a competitive markup. You can keep the app for dispatch and route the actual card processing through your own account on interchange-plus, which itemizes the markup so you can see and audit it.

Take the judgment call off the table before you load. A written, signed-off volume quote at booking, a deposit on a card kept on file, and before-and-after photos turn a verbal “half load” into a documented agreement — the exact evidence that wins a dispute. It matters more in hauling than in retail because once the load is at the landfill, there’s nothing to return and a chargeback costs you the payment, the labor, and the disposal — which is why junk removal credit card processing leans so hard on documentation.

Usually, yes. The scheduling, routing, and invoicing you rely on are separate from who actually processes the card. Many haulers keep the software they like and move the card processing to their own merchant account on interchange-plus pricing, which can meaningfully lower the effective rate without changing how you run the day. Compare your true all-in cost with an effective rate calculator before deciding; that comparison is the start of better junk removal payment processing.

Keep Reading Before You Choose a Processor

Get a junk-removal setup that stops skimming your loads.

Send us your hauling software’s rate or a recent statement and we’ll show you what you’re really paying on every load, whether you can keep your app and move the processing, what a deposit-and-signed-quote workflow would catch before the next dispute, and what an interchange-plus account would cost — no obligation, no sales pressure. Learn more about payment processing consumer protections from the CFPB.

Review My Junk-Removal ProcessingNo obligation • No pressure • Response within one business day