Precious Metals Payment Processing: Why Coin and Bullion Dealers Get Frozen

Why Coin and Bullion Dealers Get Frozen by Ordinary Processors

Precious metals payment processing usually breaks in a predictable way. A coin shop or bullion dealer opens a standard merchant account — or signs up with an aggregator like Square, Stripe, or PayPal — runs a few large online orders, and then the funds stop moving. The processor, looking at a string of transactions in the thousands or tens of thousands of dollars on a product that converts straight to cash, decides the account looks like unmanaged risk and responds with a hold, a reserve demand, or an outright freeze. Nobody underwrote the business as a precious metals business; the system simply was not built to expect gold and silver volume.

That is the core problem. An ordinary account is tuned for ordinary retail, where the average ticket is small and the goods are not liquid. Coin dealers and bullion sellers sit at the opposite end — high ticket, high liquidity, and a heavy share of card-not-present orders. To a processor that did not plan for it, every one of those traits reads as a reason to slow your money down. Stable precious metals payment processing has to start with an account that was underwritten for exactly this profile.

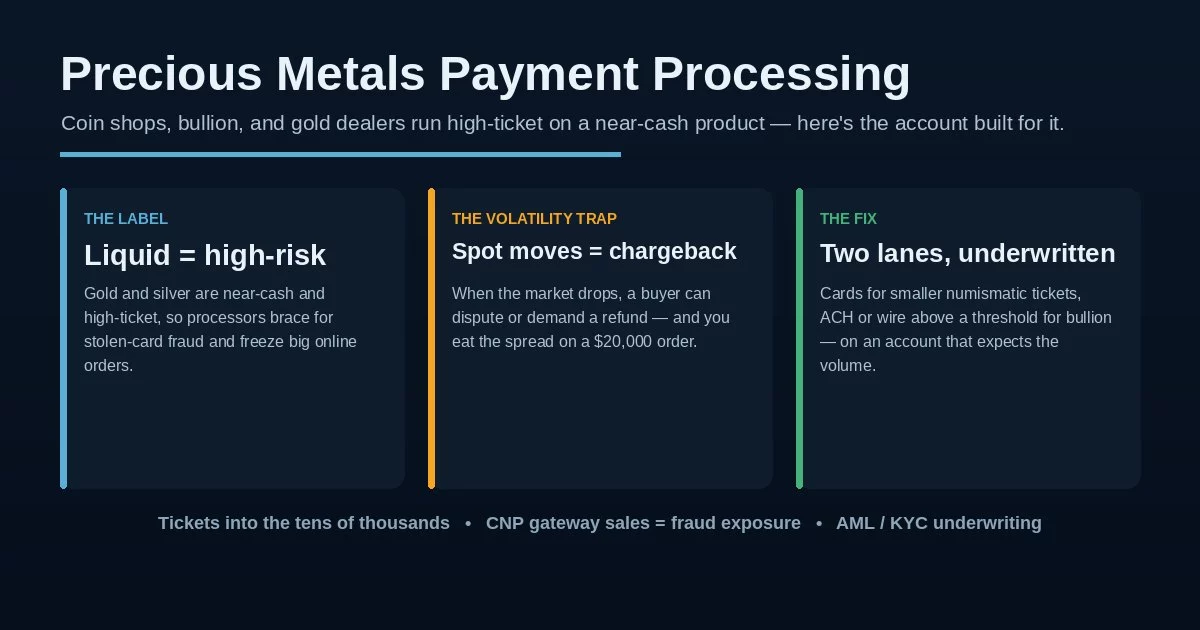

Standard accounts assume small tickets and goods that are hard to resell. A coin or bullion dealer is the inverse: five-figure orders for a product that is essentially cash. The same transaction that is routine for a clothing store trips fraud and exposure flags on an account that never expected it — which is why the freeze comes after the business is already running.

Why Coin and Precious Metals Dealers Are “High-Risk”

Selling gold, silver, and rare coins is a legitimate, long-established business — so why do banks classify it as high-risk? Three traits stack up. First is the product itself: bullion is high-value and near-cash-liquid, which makes it a magnet for fraud, because a stolen card that buys gold turns into an untraceable asset fast. Second is the channel — a large share of coin and bullion sales happen online, over the phone, or by mail order, all card-not-present, with no in-person ID or signature to verify the buyer. Third is regulation: precious metals dealers sit under anti-money-laundering and know-your-customer obligations, and some hard-currency and bullion sales carry consumer-protection rules, so the underwriting carries extra due diligence.

None of that is a judgment about whether you run a clean shop. It is a structural classification, the same one that covers other regulated categories — our overview of high-risk payment processing lays out how these accounts differ from ordinary ones. The combination is what does it: a high-ticket, highly liquid product sold mostly card-not-present is close to a worst case for a conventional processor, which is why a coin dealer payment processing setup needs a bank that has chosen to underwrite the category rather than one that stumbles into it. Getting precious metals payment processing right starts with an account that names the business honestly at underwriting.

On a precious metals account, the dollars at stake are not small. A single held batch can be tens of thousands of dollars in settled sales locked away for weeks while the processor reviews the file — money you may have already paid a supplier for in metal. For a dealer running on thin margins over spot, one freeze can mean covering a five-figure gap out of pocket with no warning.

The Chargeback Weapon Nobody Warns You About: Spot Price

Here is the risk unique to this industry. The price of what you sell changes by the minute. When a customer buys an ounce of gold and the spot price drops the next day, some buyers reach for a chargeback or a refund demand to escape a position that moved against them — a form of friendly fraud that no clothing or electronics retailer ever faces. On a high-ticket order, you can end up reversing the sale at a price that no longer matches the metal you already shipped or committed, and you eat the spread.

This is why a clear, enforced order policy is part of the payment setup, not separate from it. Locking the price at the moment the order is confirmed, stating refund and cancellation terms in writing before checkout, and keeping signed proof of delivery on every shipment are what turn a volatility dispute from a loss into a winnable case. The card networks let you fight disputes with evidence — tools like Compelling Evidence 3.0 exist precisely so a merchant with good documentation can win — but only if the documentation exists. Precious metals payment processing done right builds the dispute defense in before the first order ships.

A buyer who regrets a purchase after spot moves can frame a perfectly valid sale as “item not as described” or “unauthorized.” Without a locked price, a written refund policy, and proof of delivery, you are defenseless. With them, the same dispute is one you can win — the difference is entirely in the paperwork you set up before the sale.

What a Real Precious Metals Merchant Account Looks Like

The durable answer is a dedicated precious metals merchant account placed with an acquiring bank that wants the category — your own merchant ID, individual underwriting by analysts who expect five-figure metal orders, and fraud tooling built for card-not-present sales. The smartest precious metals payment processing setups run two lanes. Cards handle the smaller, in-store, numismatic and collectible side, where a coin shop credit card processing flow keeps checkout easy; for the big investment bullion orders, you move buyers above a set threshold onto ACH or wire transfer, which strips out chargeback risk on the transactions where it would hurt most. A coin shop is really two businesses — collectibles and investment metal — and the account should be built to serve both.

An underwritten bullion merchant account costs more than vanilla retail, and that is expected — plan for it rather than chasing a headline rate that will not survive underwriting. Per-transaction pricing runs above standard retail, and most setups carry a rolling reserve, where the processor holds back a percentage of sales for a set period against chargebacks. None of that is a scam; it is the cost of stability for a gold dealer merchant account, and it is what separates a real precious metals merchant account from a freeze waiting to happen. What you can control is transparency: insisting on interchange-plus pricing so the markup is a visible line item, and running any offer through an effective rate calculator so you compare true all-in costs, not the rate on the first page.

Your own merchant ID, underwriting that expects high-ticket metal volume, fraud scoring on card-not-present orders, a two-lane structure that routes big bullion to ACH or wire, and dispute tools built to fight volatility chargebacks. You trade a slightly higher rate for the thing that matters — an account that does not freeze the week you have your best sales.

Staying Approved — and What to Ask Before You Sign

Getting approved is the easy part; staying approved is where precious metals payment processing gets unforgiving for dealers. The heaviest pressure is on disputes — crossing the card networks’ chargeback thresholds can get an account terminated and land the business on the MATCH list, an industry blacklist that makes the next account far harder to open. The defense is operational: lock prices at order, keep airtight proof of delivery, route your largest orders to bank transfer, and keep your anti-money-laundering and know-your-customer records current, since underwriters revisit them. The same discipline keeps a rolling reserve from ballooning.

Whether you are opening a first account or replacing one that just got frozen, the vetting questions are concrete. Will you get your own merchant ID, individually underwritten — or are you being slotted into a shared aggregator account? Does the processor support a two-lane setup, with cards for smaller tickets and ACH or wire for big bullion orders? What fraud-scoring tools come with the card-not-present side? What is the reserve structure, what percentage, and when does it release? Is the pricing interchange-plus, with the markup spelled out? And read the merchant agreement closely — term length, early-termination fee, and reserve language matter most when something goes wrong. Done right, precious metals payment processing stops being the thing that could freeze your best week and becomes just another part of running the shop.

Frequently Asked Questions

Three traits combine: the product is high-value and near-cash-liquid, which attracts fraud; most sales are card-not-present online, phone, or mail orders with no in-person verification; and dealers carry anti-money-laundering and consumer-protection obligations that add underwriting scrutiny. A high-ticket, liquid product sold mostly card-not-present is close to a worst case for a conventional processor, so the account needs a bank that underwrites the category on purpose — which is what stable precious metals payment processing depends on.

Yes, indirectly. When metal prices fall after a purchase, some buyers dispute the charge or demand a refund to escape a position that moved against them, often framing a valid sale as “not as described.” On a high-ticket order you can eat the spread. Locking the price at order, a written refund policy, and signed proof of delivery turn that dispute from an automatic loss into a case you can win.

Not entirely — cards win you smaller numismatic and collectible sales and walk-in customers who expect to tap or swipe. The better model is two lanes: accept cards for smaller tickets, and move buyers above a set threshold onto ACH or wire for big bullion orders, where chargeback risk is highest. That keeps checkout easy where it helps and removes dispute exposure where it hurts.

Keep Reading Before You Choose a Processor

Get a precious metals processing setup that survives your busiest week.

Send us your current setup or a recent statement and we will show you whether you are on an account that could freeze on a big order, how to split cards and bank transfer across your ticket sizes, what a properly underwritten precious metals account would cost, and how to build the dispute defense in before you ship — no obligation, no sales pressure. Learn more about payment processing consumer protections from the CFPB.

Review My Precious Metals ProcessingNo obligation • No pressure • Response within one business day