What Is a Processing Commitment Fee — And Why It Differs from Your Monthly Minimum

Source comparison: Consumer Financial Protection Bureau guidance on merchant agreement terms and standard payment processor disclosures.

You scan your processing statement and find a line you do not recognize. PROCESSING COMMITMENT FEE — $50. Or maybe it shows as VOLUME COMMITMENT or PROCESSING SHORTFALL with the same kind of number next to it. You search the statement for an explanation. There is none. You compare it to last month and find no matching line. You wonder if it is the same thing as your monthly minimum fee, which appears two lines above it.

It is not. The processing commitment fee and the monthly minimum fee live on the same statement, sound like the same idea, and are charged for related-but-different reasons. A third sibling fee — the minimum processing volume fee — sits in the same family and gets confused for both. Processors rarely explain the differences. The result is a fee family that confuses every merchant who sees it, gets paid by most of them, and is almost never disputed.

This post explains what a processing commitment fee actually is, how it differs from the monthly minimum fee, where to find it on your statement, why processors include it in contracts, and what to do when you discover you are paying one. The short answer at the top: the monthly minimum fee penalizes you for under-generating processor revenue in a given month. The minimum processing volume fee penalizes you for falling below a dollar-volume threshold in a given month. The processing commitment fee penalizes you for missing a contractual commitment over a longer cycle — usually quarterly or annual — that you signed up to when you first opened the account.

What a processing commitment fee actually is

A processing commitment fee is a penalty charged when a merchant fails to meet a transaction count or dollar volume threshold that is written into the merchant processing agreement. The threshold can be monthly, quarterly, or annual. The penalty amount is determined by the contract clause that established the commitment — there is no industry-standard formula for how it is calculated. Some processors charge a flat penalty. Others charge a percentage of the shortfall. Others apply liquidated-damages math similar to an early termination fee.

The key word is commitment. When you signed your merchant processing contract, somewhere in the terms section there was a number — a transaction count, a monthly card volume, an annual processing total — that you committed to meeting. The processor priced your account based on that commitment. If you fall short of it, the processing commitment fee is how the processor recovers the difference between what you committed to and what they actually got.

This is structurally different from a per-transaction fee, an authorization fee, an interchange fee, or any other line item that is calculated based on what actually happened in a given month. The processing commitment fee is calculated based on what you promised in the contract, not what your business actually did.

Most merchants never read the commitment clause in their contract. Most do not even know it exists. Some never trigger the fee — their volume comfortably exceeds the commitment. But seasonal businesses, businesses going through a slow patch, and businesses whose volume has shifted to a different payment method (ACH, cash, financing) discover this fee the hard way — usually months after the trigger event, when the penalty appears on a statement.

How a processing commitment fee differs from a monthly minimum fee

The two fees get conflated because they are both triggered by low processing activity. They are not the same. The differences matter for how you respond when you see one of them.

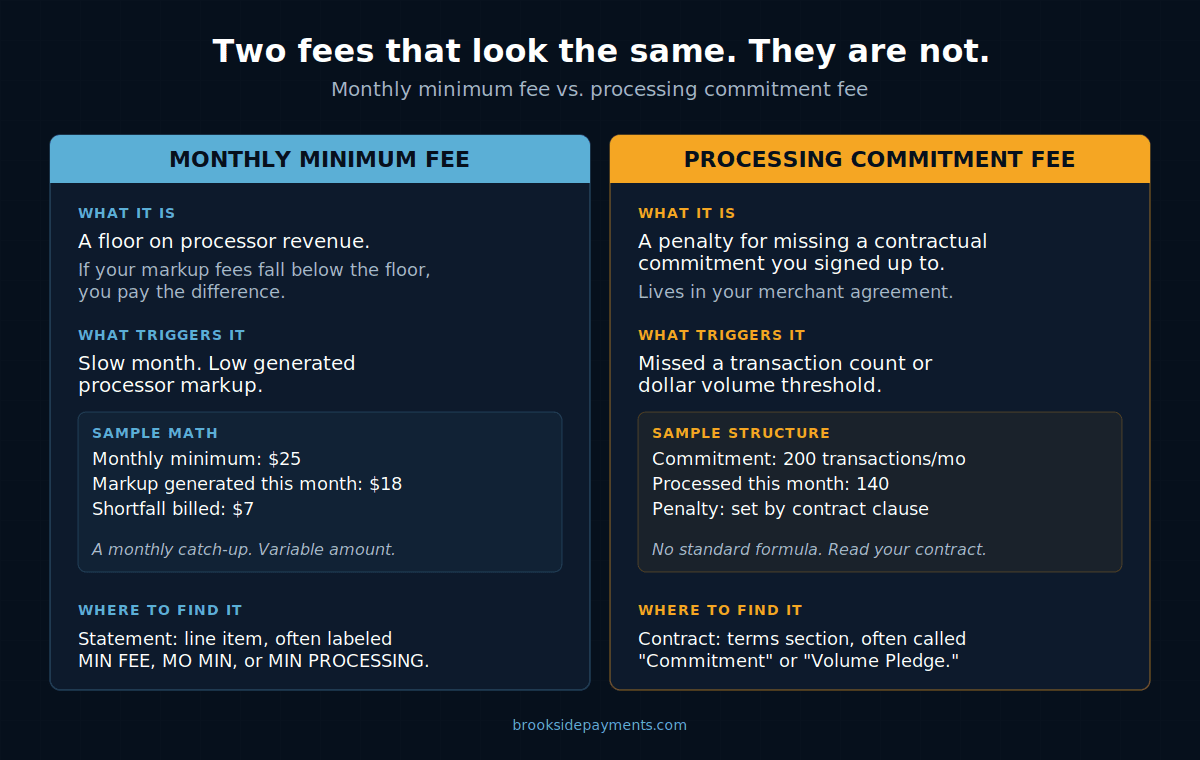

The monthly minimum fee is a floor on processor revenue. It sets a minimum dollar amount in processor markup that the processor expects to collect from your account each month. If the actual markup falls below that floor in a given month, you pay the shortfall. A typical monthly minimum is $25 to $50. The trigger is a slow month. The math is variable. The fee resets every month — a strong month wipes the slate clean.

A processing commitment fee is a penalty for missing a contractual commitment. The commitment is set at contract signing, not month-by-month. The trigger is a missed threshold — number of transactions, dollar volume, or both. The penalty amount is dictated by the contract clause, not by an end-of-month arithmetic calculation. And the fee is often quarterly or annual rather than monthly — meaning by the time it shows up, you have been under-performing the commitment for months without knowing it.

If the fee on your statement is small ($5 to $50) and varies month to month, it is almost certainly the monthly minimum fee. If a similar small fee appears month to month but seems to track your dollar volume rather than your processing-fee total, it is likely the minimum processing volume fee. If the fee is larger, appears quarterly or annually, and shows up unexpectedly, it is almost certainly a processing commitment fee. The first two you can probably negotiate out of your contract. The third requires reading the contract clause that created it.

The processing commitment fee can also stack on top of the monthly minimum fee and the minimum processing volume fee. A processor can structure all three into the same contract, and many do. You can pay a $25 monthly minimum every slow month, a $25 volume floor charge in months where your dollar volume dips below threshold, and a $300 processing commitment fee at the end of the year for missing your annual volume target. Reading the line items separately is the only way to know which is which.

How to find a processing commitment fee on your processing statement

Statement labels are not standardized. The same processing commitment fee can appear under any of the following names depending on the processor:

- Processing Commitment Fee — the canonical label, used by some traditional acquirers

- Volume Commitment Fee — common when the commitment is dollar-based

- Transaction Volume Commitment — common when the commitment is transaction-count-based

- Processing Volume Commitment — used interchangeably with the above

- Processing Shortfall Fee — emphasizes what triggered the charge

- Annual Volume Penalty — used when the commitment cycle is yearly

- Unmet Processing Commitment — descriptive long-form variant

- Merchant Services Commitment Fee — generic catch-all

To find it on your statement, do not search by label name first. Search by amount. Pull your most recent three to twelve months of statements and scan the fee section for any charge that meets all three of these criteria:

- Larger than your typical fixed monthly fees ($50, $100, $300, $500 are common ranges)

- Does not appear every month — shows up only on certain months

- Cannot be tied to a specific event (chargeback, equipment lease, PCI assessment)

If you find a charge matching that pattern, the description column on the statement is where to look next. The label may be obscured or abbreviated, but it will reference processing, volume, commitment, or shortfall in some form.

Statement design varies wildly across processors, so if you cannot decipher your statement, the guide to reading a merchant processing statement walks through the standard sections and what to look for in each.

Why processors include processing commitment clauses

From the processor’s side, a processing commitment fee exists to protect a pricing assumption. When the processor underwrites your account at contract signing, they price your rate based on expected volume. A merchant projecting $50,000 per month in card sales gets a different rate than a merchant projecting $5,000 per month. The processor’s per-account costs (account maintenance, statement generation, regulatory compliance, support) are roughly fixed. The economics work only if you generate enough volume to cover those fixed costs at the rate they offered.

The commitment clause is the processor’s insurance against a merchant who projected $50,000 per month and actually does $5,000. Without the clause, the processor loses money on the account and the merchant has no incentive to be honest about projections. With the clause, the projection becomes a contractual commitment, and the merchant either delivers the volume or pays a penalty that approximates what the processor would have made on the projected volume.

That logic is not unreasonable. But the implementation is where merchants get burned. Three patterns to watch for in a commitment clause:

An annual commitment of $600,000 in card volume looks reasonable on signing day. Eleven months in, you discover you are at $480,000 — short by $120,000 — and a processing commitment fee for the shortfall is calculated and billed in month 12. By the time you knew the problem existed, the cycle was already closed.

You committed to 200 transactions per month at signing. Two years later your business has shifted to ACH for B2B clients and you are processing 80 cards per month. The commitment did not adjust with the pivot. The penalty applies even though your business is healthier than it was at signing.

An evergreen contract clause renews the commitment automatically each year unless you cancel within a 30-day window. Most merchants miss the window, the commitment carries forward, and the penalty cycle resets.

None of the three patterns are illegal. All three are negotiable at signing, and most are negotiable at renewal. The first defense against the processing commitment fee is reading the clause before signing. The second is asking for it to be removed.

What to do if a processing commitment fee appears on your statement

If you have already been charged, the response sequence is the same regardless of which processor billed it.

Step 1 — Pull your contract. Find the commitment clause. It is usually in the Terms section, sometimes in a separate Schedule or Addendum, and occasionally in a Program Guide referenced by the main contract. The clause will state the commitment amount (transaction count, dollar volume, or both), the cycle (monthly, quarterly, annual), the penalty calculation, and the cancellation conditions. If you cannot find the clause, the contract is not complete — request the missing pages from the processor in writing.

Step 2 — Verify the math. Calculate the actual transaction count and card volume for the cycle in question. Compare to the commitment. If the math does not support the penalty (you actually exceeded the commitment, the cycle was misapplied, or the penalty calculation was wrong), dispute the charge with the processor in writing. Reference the contract clause and provide your calculation. Processors do bill these in error.

Step 3 — If the math is correct, ask for a one-time waiver. Processors will sometimes waive the fee once for a long-standing customer, particularly if the shortfall was small or driven by an explainable event (a slow season, a one-time disruption, a shift in your business model). The phrase to use is “I would like to request a one-time waiver of the processing commitment fee billed on [date].” If the processor refuses, escalate to the relationship manager or the account executive who originally signed you.

Step 4 — Renegotiate the clause for the next cycle. Even if the current penalty stands, you can usually negotiate the commitment downward, the cycle shorter, or the clause removed entirely for the next renewal. The processor would rather keep your account than enforce a penalty that drives you to switch.

Step 5 — Evaluate switching. If the contract has a long remaining term, the processing commitment fee is recurring, and the math no longer works for your business, switching processors becomes a real option. The merchant services early termination fee calculation tells you whether paying out of the contract makes sense compared to absorbing future processing commitment fees.

A modern interchange-plus pricing agreement with a transparent processor should not require a processing commitment clause at all. Interchange-plus pricing aligns the processor’s revenue directly with your actual processing — they make money when you make money, and there is no pricing assumption to protect with a penalty clause. If you are evaluating a new processor and the proposed contract still has a commitment clause, that is a negotiation point, not a deal-breaker.

Frequently Asked Questions

No. A monthly minimum fee charges you the difference when your processor markup falls below a monthly floor (typically $25 to $50). A processing commitment fee penalizes you for missing a transaction count or volume threshold that you committed to in your contract — usually quarterly or annually, with the penalty amount set by a specific contract clause.

There is no industry-standard formula. The calculation is determined by the commitment clause in your specific merchant processing contract. Some processors charge a flat penalty for missing the commitment. Others calculate a percentage of the shortfall between your committed volume and your actual volume. Others apply liquidated-damages math that approximates what the processor would have earned on the missed volume. The only authoritative source for your fee calculation is your contract.

Sometimes. Processors will occasionally waive the fee once for a long-standing customer, particularly when the shortfall was modest or driven by an identifiable cause. Request the waiver in writing, reference the specific charge by date and amount, and escalate to a relationship manager or account executive if the first response is a refusal. Renegotiating the commitment clause for the next cycle is a separate conversation worth having at the same time.

Found a processing commitment fee on your statement?

If a charge for processing commitment, volume commitment, or processing shortfall has appeared on a recent statement and you need help reading the contract clause that created it, request a free statement review. We will read the agreement, calculate whether the penalty was correctly applied, and tell you what your options are.

Get Your Free Statement ReviewNo obligation • No pressure • Response within one business day

See what a statement review looks like →