SurchargeCredit Card Surcharge Definition & Guide

Surcharge — Definition & Guide

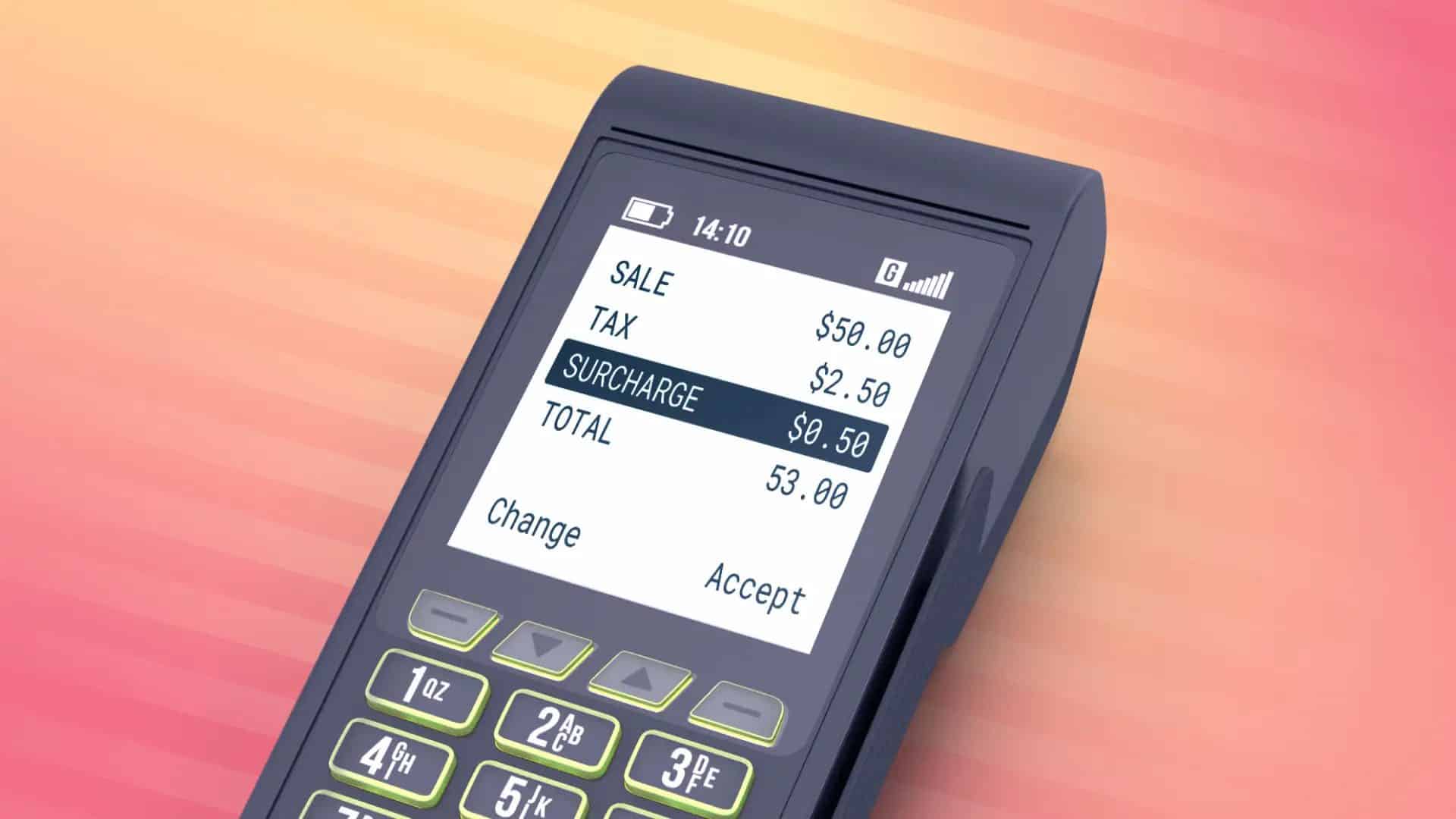

A credit card surcharge is an additional fee added to the purchase price when a customer pays by card. Unlike a cash discount — which reduces the price for cash-paying customers — a surcharge adds on top of the posted price for card users. Card network credit card surcharge rules cap the fee at 3% and require advance notice and signage. Some states prohibit them entirely. According to the Federal Reserve’s interchange fee data, actual credit card acceptance costs vary by card type — the rate must not exceed what you actually pay to process.

A surcharge is one of three primary strategies merchants use to offset processing costs. The other two — cash discount programs and dual pricing — achieve a similar outcome through different pricing structures and disclosure requirements. The right choice depends on your state, your card mix, and how you want to present pricing at checkout.

The key distinction: a cash discount lowers the price for customers who pay cash. Adding a fee raises the price for customers who pay by card. Both shift processing costs to the card-paying customer, but they are disclosed and structured differently under card network rules.

Adoption trend: 34% of US small businesses added a surcharge in 2025 and 35% in 2026 (J.D. Power), up from 1–2% in 2019 — the fastest-growing pricing model shift in US payments. See the full adoption analysis and decision framework.

These programs are governed by both card network rules and state law. The requirements are specific and non-negotiable:

- 30-day advance notice — Notify your processor in writing at least 30 days before implementing

- Entrance signage — Post notice at the store entrance that a fee applies to card payments

- Point of sale disclosure — Disclose the amount before the transaction is completed

- Receipt disclosure — The amount must appear as a separate line item on the receipt

- Rate cap — Cannot exceed 3% (Visa and Mastercard) or your actual cost of acceptance, whichever is lower

- Credit cards only — Debit cards cannot be included, even when processed as credit

Most U.S. states allow this following legal rulings that struck down state-level prohibitions. As of 2024, Connecticut and Massachusetts still prohibit them. Puerto Rico also prohibits them. All other states permit it subject to card network rules. The CFPB’s guidance on credit card fees and card network rule documents are the authoritative sources for current requirements.

In most states, yes. Connecticut and Massachusetts still prohibit them. Card network rules also require specific disclosure procedures — advance notice, entrance signage, point of sale disclosure, and receipt itemization — regardless of state.

No. Card network rules prohibit it on debit cards, even when processed as credit. The fee applies only to credit card transactions.

You must notify your processor 30 days in advance, post signage at the entrance and point of sale, and itemize the charge separately on the receipt. The rate cannot exceed 3% or your actual processing cost, whichever is lower.

Improper Surcharge Implementation Triggers Card Brand Penalties. The Rules Are Specific.

Send us your last processing statement. We will assess whether surcharging makes sense for your card mix, walk through the specific signage, disclosure, and 4% cap requirements, and show you what your effective rate would be after a compliant surcharge implementation.

Request a Free Statement ReviewNo obligation • For glossary readers comparing pricing models and processor options • Response within one business day