34% of Small Businesses Now Surcharge. The Question Isn’t Whether You Should — It’s Whether You Can Afford Not To.

34% of Small Businesses Now Surcharge. The Question Isn’t Whether You Should — It’s Whether You Can Afford Not To.

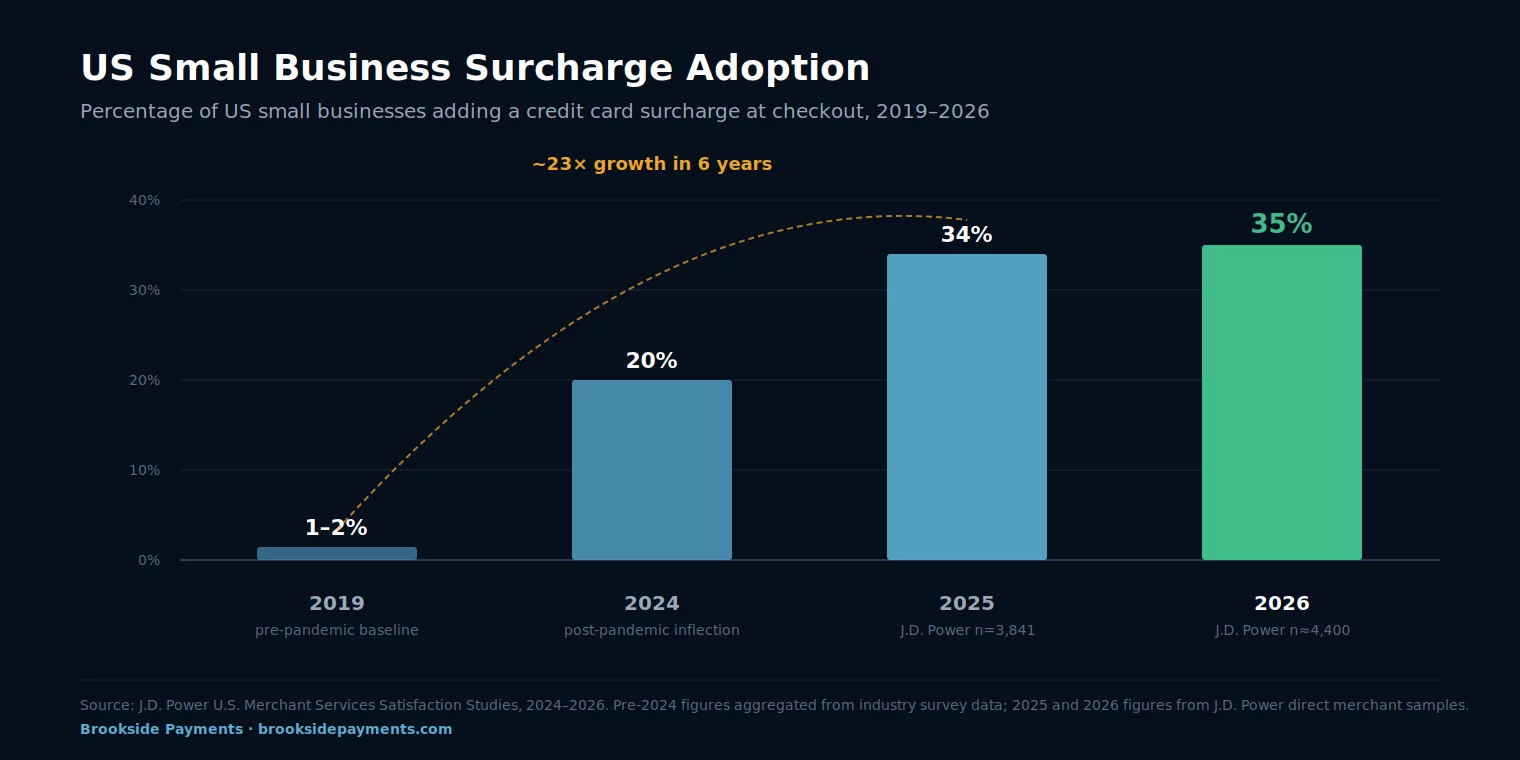

Small business surcharge adoption in the United States has tripled in twenty-four months. Six years ago, almost no small business in the United States passed credit card processing costs to the customer. The model was technically legal in 40-plus states, but adoption sat in the low single digits — somewhere between one and two percent of merchants. The remaining 98% absorbed card processing as a cost of doing business, treating it the way they treated rent and electricity.

That math has now broken.

According to J.D. Power’s 2026 U.S. Merchant Services Satisfaction Study (sample size approximately 4,400 merchants), 35% of US small businesses now add a credit card surcharge or dual-price their goods and services at checkout. The 2025 figure was 34%. The 2024 figure was 20%. Pre-pandemic, the figure was 1-2%. This is the single largest pricing-model shift in US payments history, and it happened in roughly five years.

This is a strategic decision framework, not a how-to. We cover what 34% really means, why adoption accelerated this fast, which verticals lead and lag, the customer-pushback data that should temper the enthusiasm, the state-by-state legal map, and how to think about whether surcharging fits your specific business. The mechanics of implementing a surcharge program — terminal setup, signage requirements, processor disclosures — are separate operational topics covered in the linked resources below.

How One-In-Fifty Became One-In-Three in Six Years

The inflection point was 2020. Before that, surcharging was technically permitted in most US states but practically rare — a fringe practice associated with bodegas, taxi drivers, and small operators who didn’t have the leverage to negotiate processor rates and didn’t have the customer trust to risk pushing back. The 1-2% adoption figure stayed remarkably stable from roughly 2013 (when Visa and Mastercard’s surcharging restrictions were loosened by litigation settlement) through 2019.

Three things changed simultaneously between 2020 and 2024.

First — interchange rates kept climbing. Visa and Mastercard’s network-level fee increases compounded with the post-pandemic shift toward premium rewards cards, which carry interchange categories 50-80 basis points higher than basic credit cards. Effective rates that sat at 2.4% in 2019 were 2.8% by 2023 for the same merchant on the same processor with no contract renegotiation.

Second — labor costs went up faster than pricing power. A 5% increase in card processing cost is invisible when wages are stable. When the front-office staff just got a 12% raise and the food cost is up 18%, the 5% on top is suddenly a real number on a payroll-week spreadsheet.

Third — peer adoption removed the social risk. The 2019 small business owner who put up a “3% surcharge for credit card” sign was an outlier. The 2024 owner was doing what the deli, the dry cleaner, the auto shop, and the dentist across the street had already done. The customer pushback that owners feared in 2019 had largely been absorbed by the broader market by 2024.

By 2025, 34% of US small businesses had moved. By 2026, it was 35% — meaning the curve has flattened from the steep 2020-2024 climb, but the new baseline is locked in.

The J.D. Power 35% figure aggregates three related but legally distinct mechanisms: surcharging (adding a fee at checkout to the card price), cash discounting (lowering the price for cash payment), and dual pricing (displaying both prices simultaneously). Each carries different state-law obligations, different network rules, and different customer reactions. The mechanics matter once you implement; for adoption-trend purposes, J.D. Power groups them under one umbrella because the operator intent is the same — pass card cost to the card user.

Who Adopted First, Who Adopted Hardest, Who Held Back

Small business surcharge adoption hasn’t been uniform across the economy. Some verticals jumped quickly; some are still nearly entirely absorbing card costs. Five categories drove the bulk of the 2020-2025 climb.

Restaurants and quick-service food. Restaurants led the adoption wave for two reasons. First, the average ticket is small (often under $30) and the processor fee on a $25 ticket is invisible to the customer but meaningful to the operator at scale. Second, restaurants live and die on labor cost and food cost — the third major variable cost (card processing) became the obvious lever once labor and food costs spiked post-pandemic. By 2025, restaurant adoption was estimated above 50%, well ahead of the 34% national average.

Home services and field service. HVAC, plumbing, electrical, landscaping. Large average tickets ($500-$5,000) where card processing fees can run $15-$150 per job. These trades adopted dual pricing aggressively — particularly the cash discount variant — because the customer is typically already getting a written estimate and the cash-vs-card conversation is natural to have at signoff.

Healthcare practices that don’t take insurance directly. Dental, chiropractic, optometry, cash-pay aesthetic medicine. Larger tickets, patients already discussing payment methods at checkout. Dental in particular leans toward dual pricing because the practice has HSA/FSA conversations in flow anyway — the card-vs-cash framing fits the existing patient interaction.

Specialty retail and small storefronts. Higher AOV retail with a regular customer base — bike shops, audio-video, jewelry, art galleries. Where the customer relationship is durable and the average ticket is large enough that the savings justify the implementation friction.

Trade and B2B service. Plumbing wholesalers, HVAC distributors, small commercial accounts. B2B specifically pushed harder toward ACH adoption rather than surcharging, but for the card volume that remains, surcharging is common.

The laggards are equally instructive. Mass-market chain retail has barely moved — when you compete with Target and Costco on price, you can’t add 3% to checkout. E-commerce is a special case — surcharging at checkout in an online flow has its own legal and conversion-rate issues, and most platforms haven’t tooled for it. Hospitality at the upscale tier — fine dining, boutique hotels — has stayed away from surcharging to avoid the perceived friction with high-spend guests.

What Customers Actually Do When You Add a Surcharge

The 34% adoption number is half of the story. The other half — and this is the underused half — is what happens at the customer side of the transaction.

The same J.D. Power 2025 study found that 41% of US credit card users report having walked away from a purchase at least once because of a credit card surcharge. Not “felt annoyed.” Not “complained to the merchant.” Walked out without buying.

That same study found a separate but related figure: 32% of credit card users report having canceled a planned transaction at the point of payment after seeing the surcharge total. These two figures overlap heavily — most of the 32% are also in the 41% — but they measure slightly different things. The 41% is lifetime; the 32% is recent transactions.

This is the data point that surcharge enthusiasts skip past and that surcharge skeptics over-weight. Both readings miss the actual signal.

If you implement a 3% surcharge and 5% of your card customers walk away over it, you’ve broken even — the 3% you save on the 95% who paid covers the lost margin on the 5% who left, roughly. If 10% walk away, you’ve lost money. If 2% walk away, you’ve netted ~2.5% on every transaction. The J.D. Power 41% and 32% figures are not measuring your business — they’re measuring the lifetime card-using population. Your actual walk-away rate depends on your vertical, your customer demographics, your average ticket, and whether you’re surcharging or dual-pricing (these get reacted to very differently). Most merchants who run the math properly land somewhere between 0% and 4% measurable walk-away — well inside the break-even zone.

The honest read: customer pushback to surcharging is real, but it’s smaller than the J.D. Power top-line numbers suggest at the merchant level, because customers who hate surcharging cluster at certain business types and price points. The customer who walks out of a $42 dinner over a $1.26 surcharge would have walked out anyway. The customer who pays $4,200 for a dental implant rarely cancels over $126.

Where You Can Surcharge, Where You Can’t, and Where the Rules Are Quiet

State-by-state surcharge legality matters because the penalty for getting it wrong is meaningful — civil suits, state attorney general enforcement, and in two states, low-level criminal exposure for the operator.

As of 2026, surcharging on credit card transactions is legal in 46 US states and DC with disclosure requirements. The four state-specific situations to understand:

| State | Status | Practical workaround |

|---|---|---|

| Connecticut | Surcharging prohibited | Cash discount programs legal — same economics, different mechanics |

| Massachusetts | Surcharging prohibited | Cash discount programs legal |

| Maine | Disclosure-restricted (4% cap, written notice required) | Surcharge with 4% cap and posted signage |

| Colorado | 2% cap on surcharge amount | Surcharge legal up to 2% — typical processing cost is ~2.3%, so cap is binding |

| Other 46 jurisdictions | Surcharging legal with disclosure | Generally cap at processor cost (typically 3-4%) |

The two outright bans — Connecticut and Massachusetts — both permit cash discount programs. Operationally this matters: a Connecticut merchant can’t show “$100 + 3% credit card fee” but can show “$103 / $100 cash.” Same economics, different legal mechanics, different signage rules. Cash discount programs have no state bans anywhere in the US.

Beyond state law, two network-level rules apply nationally. Visa and Mastercard cap surcharges at 3% of the transaction amount (4% as of 2023, lowered). Debit card surcharges are prohibited under the Durbin Amendment regardless of state law — so any surcharge program needs the terminal configured to apply only to credit cards.

The states that permit surcharging require disclosure at the entry of the establishment and at the point of sale. Most enforcement actions against surcharging merchants stem from disclosure failures, not the surcharge itself. Network rules require disclosure on the receipt and 30 days’ advance notice to the acquirer (your processor) before implementing. If you’re considering a surcharge program, the legal exposure is overwhelmingly on the disclosure side — get the signage and the receipt language right and you’ve eliminated 95% of the risk.

Should You Surcharge? Five Questions That Decide It.

The 34% adoption number tells you small business surcharge programs are now mainstream. It doesn’t tell you whether the option fits your specific business. Five questions decide it.

1. What’s your average ticket size? Surcharging works best where the surcharge dollar amount is small enough to feel reasonable but the savings to you are large enough to justify the implementation cost. Under $20 average ticket: surcharging is hard — the customer notices a $0.60 surcharge on a $20 transaction. $20-$100: works in some verticals, harder in others. $100-$1,000: surcharging works in most verticals where the customer has a transactional relationship rather than a discount-shopping relationship. Over $1,000: surcharging is well-tolerated almost universally.

2. What’s your customer’s transactional alternative? If the customer can pay you by check, ACH, or cash without serious friction, the cash-vs-card price comparison feels fair. If your only realistic payment method is card (e-commerce, phone orders, recurring billing), surcharging feels like a hidden fee even when fully disclosed. Verticals with realistic non-card payment options adopt easily; verticals where card is the only practical method struggle.

3. What’s your competitor’s pricing model? In a vertical where 60% of competitors surcharge, you’re the laggard absorbing cost. In a vertical where 5% of competitors surcharge, you’re the outlier and you’ll lose customers to the 95% who don’t. The decision is partly local-market and partly vertical-norms. Field service trades hit the tipping point first; mass-market retail hasn’t tipped at all.

4. What’s your customer demographic? Surcharge sensitivity varies sharply by demographic. Older customers (60+) often prefer surcharging because they remember when card use was rare and they associate cash with discipline. Younger customers (25-40) are more likely to react negatively — they grew up assuming card was free and treat the surcharge as a punishment. High-income customers care less; price-sensitive customers care more. Local markets in Florida, Arizona, Texas have higher tolerance; markets in Massachusetts, New York, California have lower tolerance.

5. What’s your operational complexity tolerance? Surcharging adds disclosure obligations, receipt-language requirements, signage maintenance, network compliance audits, and customer-service conversations. Cash discount programs have fewer obligations but still require disclosure. Dual pricing has the least operational lift but requires menu/price-list maintenance. The right answer depends on whether your operation has the bandwidth to add a small ongoing compliance burden in exchange for the savings.

If your average ticket is over $100, your vertical has 25%+ surcharge adoption among competitors, and your customer base has a non-card payment alternative, surcharging or dual pricing is almost certainly the right move — and the longer you delay, the more peer competitors gain a margin advantage you’re not capturing. If your average ticket is under $30, your vertical hasn’t tipped (chain retail, e-commerce), or your customers have no realistic non-card alternative, surcharging probably isn’t your best lever — focus on interchange-plus pricing renegotiation and ACH for any B2B portion of your volume.

Frequently Asked Questions

No. Surcharging adds a fee to the card price at checkout — the customer sees one price and a fee added. A cash discount program lowers the price for cash payment — the customer sees a higher posted price and a discount applied for paying cash. The economics are similar but the legal mechanics, network rules, and customer reactions differ. Surcharging is restricted in two states (CT, MA); cash discount programs are legal everywhere. Cash discount programs also avoid the 3% network cap and the debit-card surcharge prohibition because the discount is given for non-card payment, not a fee added to the card payment. Dual pricing is a third variant — displaying both prices simultaneously — and is the easiest to implement compliance-wise.

Failing to disclose properly at the point of sale. Network rules and most state laws require disclosure at the entry of the establishment (sign at the door), at the point of purchase (signage at the register or on the menu), and on the customer receipt (line item showing the surcharge amount and rate). The second most common mistake is surcharging debit card transactions — the Durbin Amendment prohibits this regardless of state law, and most modern POS systems require explicit configuration to apply surcharges only to credit transactions. Get these two right and your compliance exposure drops to near zero.

Because the 41% figure measures the lifetime card-using population across all businesses, not the actual walk-away rate at any individual merchant. The customers who hate surcharging cluster at specific business types (low-ticket retail, e-commerce) and specific demographics (younger, urban, price-sensitive). Merchants in the verticals adopting surcharging — restaurants over $40 average ticket, dental practices, home services trades, B2B service operations — experience walk-away rates in the 0-4% range, well inside the break-even threshold where the savings on the 95%+ who pay cover any lost margin from the small minority who walk. The aggregate 41% is real but it’s not what any individual operator sees in their own transaction data.

More on pricing models, surcharge mechanics, and alternative strategies

Send Us Your Statement. We’ll Run the Walk-Away Math on Your Actual Card Mix.

The small business surcharge decision isn’t generic — it depends on your average ticket, your vertical, your customer demographics, and what your competitors are already doing. Send Brookside one recent merchant statement and we’ll calculate your break-even walk-away rate, identify whether surcharging or dual pricing fits your business better, and pull state-specific compliance requirements for your location. We don’t push surcharging on every merchant — about 40% of the businesses we audit are better served by interchange-plus repricing or ACH migration instead. The math takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for Free ReviewNo obligation • No pressure • Response within one business day