Why Your B2B Clients Shouldn’t Pay By Credit Card. And Why a Growing Number of Them Won’t.

Why Your B2B Clients Shouldn’t Pay By Credit Card. And Why a Growing Number of Them Won’t.

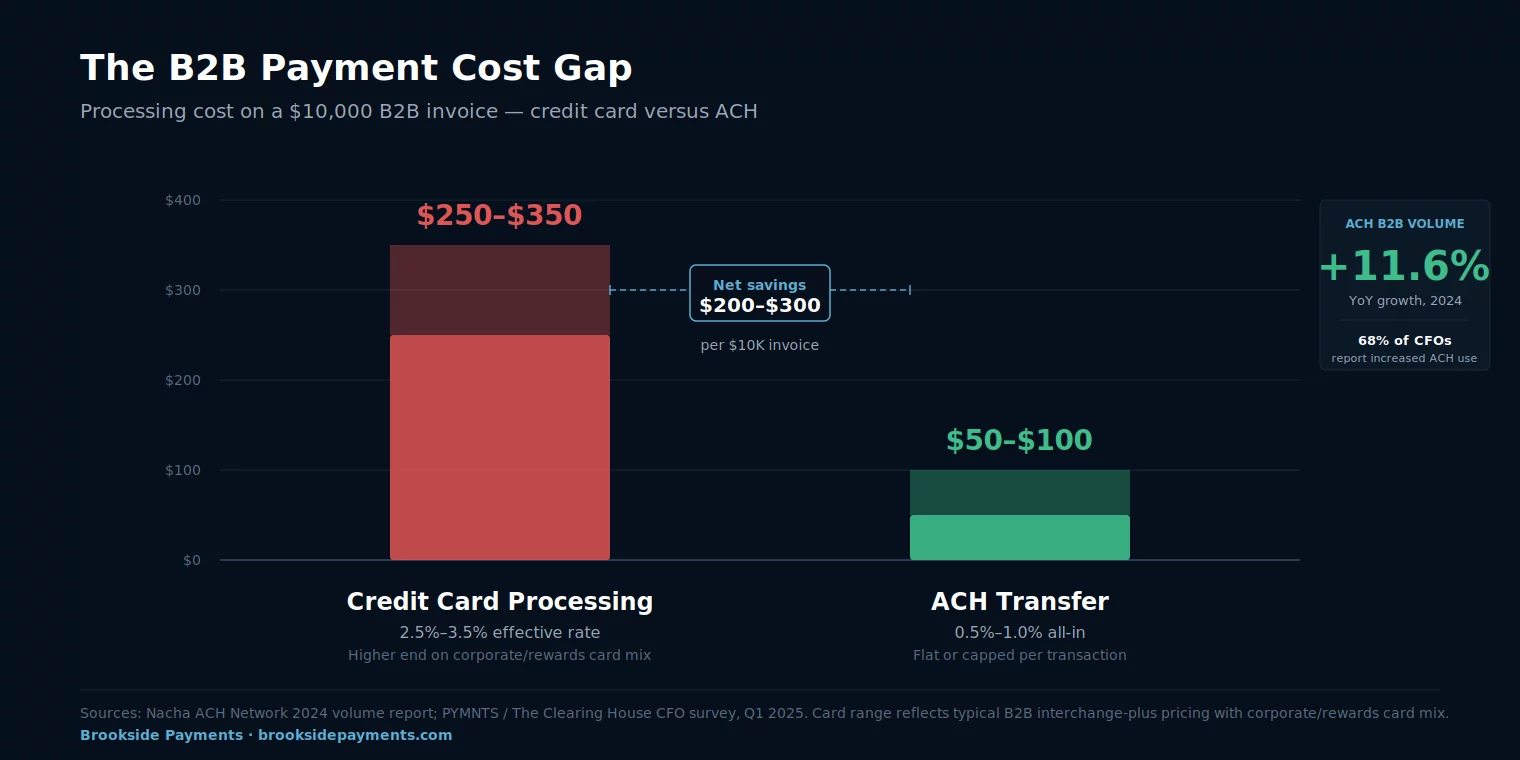

On a $10,000 B2B invoice, credit card processing costs the merchant $250 to $350 in fees. ACH costs $50 to $100. That’s a $200 to $300 gap. Per invoice. Every invoice. On a B2B operation with $4 million a year in card-paid invoices, the gap compounds to roughly $80,000 a year — straight off the bottom line, for no functional benefit to the business.

This isn’t new. The math has been roughly the same for fifteen years. What’s new is that B2B customers — particularly CFOs and AP departments — are finally moving. ACH B2B payment volume grew 11.6% year-over-year in 2024 per Nacha (the ACH network operator), and grew another 10.8% in Q1 2025. 68% of CFOs report increased ACH use at their company in the past twelve months, per the PYMNTS / Clearing House CFO survey. The shift away from B2B card payments is happening at scale, and the operators who don’t restructure their billing to make ACH the default are losing margin every quarter to operators who do.

This post is for business owners who invoice other businesses — accounting firms, law firms, contractors, B2B service providers, SaaS resellers, wholesalers, agencies. The question isn’t whether to accept ACH; most of you already do. The question is whether ACH should be the default and card payment should be the exception, or vice versa.

B2C card payments have legitimate consumer-protection rationale: dispute rights, chargeback protections, fraud liability shifts. B2B card payments rarely use those features — disputes between businesses go to the contract and to court, not to the card network. Yet B2B card transactions still pay full retail-card interchange rates, which exist to fund those consumer protections the B2B transaction doesn’t use. The mismatch is where the savings hide.

What Card Acceptance Actually Costs You on B2B Invoices

B2B card processing runs higher than B2C card processing for two reasons, both structural.

First — card mix. B2B clients pay with corporate cards, purchasing cards, and commercial rewards cards. Each carries higher interchange than a consumer’s basic Visa or Mastercard. A Visa Business Card runs 2.50% + $0.10. A Visa Corporate / Purchasing Card runs 2.65% + $0.10. A Visa Signature Business runs 2.70% + $0.10. The basic consumer credit interchange is around 1.65% + $0.10. Your B2B mix is structurally 50-100 basis points more expensive than your B2C mix would be.

Second — Level 2 and Level 3 data. Visa and Mastercard offer reduced interchange rates for B2B transactions where the merchant submits enriched transaction data (tax amount, shipping ZIP, customer code, line-item detail). The reductions are real — 50 to 100 basis points off the base interchange — but only when the processor and POS system actually capture and transmit the required fields. Most accounting software and most processors don’t. Transactions get downgraded — billed at non-qualified rates — and the merchant pays full retail-plus interchange instead of the discounted B2B rate.

Stack the two together and a typical B2B merchant accepting cards pays 2.7% to 3.5% effective on card-paid invoices. The same invoice paid by ACH costs 0.5% to 1.0% — typically a flat per-transaction fee of $0.25 to $5.00, sometimes a low percentage capped at $5 or $10.

A B2B law firm with $4 million a year in card-paid client invoices loses roughly $80,000 to processing fees. Move half to ACH and the savings is $30,000 to $50,000. Move 80% to ACH and the savings is $55,000 to $80,000. For a 10-partner firm, that’s $5,500 to $8,000 per partner per year — recovered, with no client lost. Most firms don’t run this math because processing cost shows up as one line on the merchant statement, not 10,000 line items in QuickBooks. The aggregate hides the size of the savings until someone makes the comparison explicit.

The Verticals Where B2B Clients Now Default to ACH

Adoption hasn’t been uniform. Some B2B verticals have moved aggressively; others are still mostly card-paid.

Accounting and bookkeeping firms. Most progressive. CPAs see the math viscerally on their clients’ statements every month. The recent wave is firms migrating their own AR collection. QuickBooks and Xero both support native ACH; resistance is usually inertia, not technical.

Law firms. Mixed but moving. LawPay’s market dominance means most firms accept cards out of habit, but Trust Account compliance is easier with ACH. Firms whose AP teams have started actively offering ACH to clients are recovering meaningful margin.

Architecture, engineering, design firms. Project-based billing with large invoices ($25K-$250K) makes the card-vs-ACH math huge per invoice. A 3% fee on a $100K invoice is $3,000; ACH on the same invoice is roughly $5. The decision usually gets made the first time a project manager sees a processing fee line on the monthly statement.

Wholesale distributors and trade B2B. Plumbing supply, HVAC distribution, restaurant equipment, building materials, and freight and trucking. High volume, low margin, sensitive to every basis point. These verticals were on ACH and check long before the current wave; smart distributors push back on virtual-card pressure with ACH discounts.

SaaS and recurring B2B services. The fastest adoption curve. Recurring billing on a card carries chargeback risk, card-expiry friction, and rate-update overhead. ACH recurring is more stable. SaaS billing in 2026 increasingly defaults to ACH for any contract above $1,000/month.

Construction and general contracting. Slow movers — but progressing. Construction has been check-heavy with cards for materials supply. The migration is from check to ACH, with cards a minority share. Biggest blocker: long payment cycles (30/60/90 day terms) where changing methods adds operational friction.

The laggards are equally instructive. Marketing agencies and consultants often default to cards because clients prefer paying small invoices ($1K-$10K) on a corporate card for expense-tracking. Small B2B service providers ($100-$2K invoices) accept cards because the convenience outweighs the percentage cost at that ticket size. Professional services with mixed B2B/B2C revenue keep card acceptance because their B2C side requires it.

Three things predict whether a B2B vertical has moved aggressively to ACH: average invoice size (bigger = faster adoption), recurring-versus-one-time billing mix (recurring = faster), and whether the operator sees the processing fee line on their own statements (visibility = faster). Verticals that score high on all three are 5-10 years ahead. Verticals that score low — small-ticket marketing services, individual practitioners, mixed B2C operations — are still mostly card-paid and likely to stay that way for another 3-5 years.

“But My Clients Want to Pay By Card.” Here’s What That Usually Means.

The most common reason business owners give for not pushing harder on ACH adoption is that “clients prefer cards.” In our experience auditing merchant statements, that statement is rarely accurate. Three things are usually going on instead.

Habit, not preference. Your client’s AP department has been paying you by card for three years because that’s how it was set up. Nobody on either side has revisited it. Asked directly — “would you prefer ACH instead?” — most B2B clients say yes, especially after you mention it’ll save you both time at month-end reconciliation.

Rewards capture on a corporate card. The AP person may genuinely like paying by card because the corporate card earns rewards or cashback for their company. This is a real preference, and matters more in some industries than others. The trade-off is direct: your client’s rewards are your processing cost. The fix is pricing differentially (cash discount style, where ACH price is 2-3% lower than card), or accepting that some clients will keep paying by card and you’ll keep absorbing that cost.

You haven’t actually offered ACH. A surprising number of B2B merchants will say “my clients prefer cards” while not actually having a clear ACH payment option in their invoicing flow. The invoice goes out with a “Pay Now” button pointing at a card processor and no displayed alternative. Of course clients pay by card — it’s the only frictionless option offered. Adding a visible “Pay by ACH (saves us both money)” link next to the card button changes the mix dramatically.

Roughly 60% of B2B card transactions we audit could move to ACH without any client friction — the client wasn’t expressing a preference, just paying the way the invoice presented. Another 25% would move with a small structural nudge (visible ACH option, two-line note on invoice). The remaining 15% are genuinely card-preference clients where the rewards capture justifies it for them and the trade-off needs explicit pricing handling. That’s a 60-85% ACH migration ceiling for most B2B merchants — and the gap between the 60% and the 85% is purely an operational design choice.

How To Actually Move Your B2B Receivables to ACH

Three paths, ordered roughly by implementation cost.

Path 1 — Add ACH as a visible option on your existing invoicing. If you bill through QuickBooks, Xero, FreshBooks, Wave, or Bill.com, native ACH collection is built in. Turn it on. Add invoice template language mentioning ACH as the preferred payment method. Test on three to five clients before rolling out broadly. Implementation: a few hours. Cost: $0-$3 per ACH transaction. Best for small to mid-size B2B operations with existing accounting-software billing.

Path 2 — Dual pricing on your invoices. The B2B version of the consumer dual-pricing model. Your invoice shows two prices: cash/ACH price and card price (typically 2.5-3% higher). Done as a blanket B2B surcharge, though, it can cost you the account — here is where surcharging your business customers backfires. Client picks. Works well when card payments are a meaningful share of your volume and you want to recover the cost without losing the client option. Implementation depends on your invoicing software; some platforms make this one-click, others require manual customization. Best for service businesses with large invoices and price-sensitive clients.

Path 3 — Move to a dedicated B2B payment platform. Bill.com, Melio, Stripe Treasury, Modern Treasury, and similar offer purpose-built B2B AR/AP infrastructure with ACH as the default rail. These platforms handle invoicing, payment, and reconciliation in one place. Implementation: 2-4 weeks for a typical B2B service business. Cost: subscription with low per-transaction fees. Best for B2B operations with $500K+ annual AR volume.

For most B2B service operations under $2M in card volume, Path 1 captures 70-80% of available savings. Path 2 adds 10-15%. Path 3 is the right answer for larger operations where AR/AP infrastructure has become a meaningful operational concern beyond just processing cost.

Under $500K annual AR: Path 1 (native ACH in your existing accounting platform) is almost always right. $500K to $2M: Path 1 with Path 2 added once you see how clients respond. Over $2M: evaluate Path 3 platforms, especially if your AR/AP workflow has become a real operational concern beyond just processing cost. Most B2B operations overestimate how complex the implementation needs to be and underestimate how much of the savings is captured by Path 1 alone.

What ACH Actually Costs, How It Settles, and the Risks Worth Knowing

ACH (Automated Clearing House) is the US bank-to-bank transfer network operated by Nacha, moving roughly $80 trillion a year — more than card networks combined. The mechanics differ enough from card payments to be worth understanding.

Settlement timing. Standard ACH settles in 1-3 business days. Same-day ACH (introduced 2016, expanded 2021) settles in hours and handles the majority of B2B ACH volume. Wire transfers — sometimes confused with ACH — settle in hours but cost $15-$50; ACH at $0.25-$5.00 is the right tool for most B2B payments.

Returns and reversals. Business-to-business ACH transactions have a 2-banking-day return window in most cases. Returns happen for insufficient funds (most common), closed accounts, or authorization disputes. Return rates for established B2B clients are typically under 0.5%.

Fraud and chargeback comparison. ACH has materially lower fraud rates than cards — account-and-routing-number theft is harder to monetize than card-number theft. ACH has no “chargeback” mechanism in the card sense — disputed B2B ACH transactions go through bank-level processes that take longer but are typically more predictable. For most B2B operations, the fraud/chargeback shift from cards to ACH is a net positive.

Authorization requirements. ACH debits require explicit client authorization — a signed form, a checkbox on an online invoice, or a stored recurring authorization. The compliance bar is real but routine; most B2B invoicing platforms handle it automatically.

Most B2B ACH disputes that go badly for the merchant trace back to a missing or unclear authorization record. The fix is simple: store a dated, client-signed (or checkbox-affirmed) authorization for every account on file, and re-authorize annually for ongoing recurring billing. Your invoicing platform almost certainly already does this — but verify before you scale up. The cost of getting authorization wrong is occasional reversed transactions and zero criminal exposure; the cost of getting it right is ten minutes of platform configuration.

Should Your B2B Receivables Default to ACH? Four Questions That Decide It.

The 11.6% YoY ACH B2B growth tells you the market is moving. It doesn’t tell you whether the move fits your specific operation. Four questions decide it.

1. What’s your average B2B invoice size? The savings on a $200 invoice is $5-$10. The savings on a $20,000 invoice is $500-$700. The implementation cost is roughly the same either way. The ROI curve favors larger average invoices. Under $500: ACH is nice-to-have. $500-$5,000: significant. Over $5,000: ACH should already be your default.

2. What share of your AR is B2B versus B2C? Pure B2B operations (architects, law firms, B2B distributors, B2B SaaS) can fully restructure invoicing around ACH. Mixed operations (consultants who serve both individuals and businesses, professional services with both types of clients) need to keep card acceptance for the B2C side and can default the B2B side to ACH. Heavily B2C operations with occasional B2B work shouldn’t restructure for the small B2B portion.

3. How predictable is your client base? ACH works best with repeat clients on regular billing cycles. The authorization step is a small friction with first-time clients. Mostly one-time projects with new clients: ACH adoption is slower. Mostly recurring engagements with established clients: ACH is almost frictionless after the first invoice.

4. What does your accounting / invoicing platform already support? If you’re on QuickBooks, Xero, FreshBooks, Bill.com, or a similar major platform, native ACH is essentially turn-key. If you’re on a custom invoicing system or a niche platform without native ACH, the implementation cost is real — usually 1-3 weeks of setup and integration work. The platform-driven implementation cost is the most common reason B2B operations stay on cards longer than they should.

If your average B2B invoice is over $1,000, your AR is more than 60% B2B, your client base is mostly repeat, and you’re on a major accounting platform — ACH should be your default within 90 days. The math on staying card-default at that profile is hard to justify; you’re leaving 2-3% of every invoice on the table. If you’re under $500 average invoice, heavily B2C, or on a custom invoicing system, prioritize other levers first (interchange-plus repricing, Level 2/3 data optimization) and come back to ACH migration once the foundational pieces are in place.

Frequently Asked Questions

In our experience auditing B2B merchant statements, roughly 60% of card payments could move to ACH without any client friction — the client wasn’t expressing a preference, just paying the way the invoice presented. Another 25% will move when ACH is visibly offered as the preferred option. The remaining 15% genuinely prefer card payment for corporate-card rewards or expense-tracking convenience, and that group needs explicit pricing handling (dual pricing) or acceptance. Most B2B merchants who default to ACH see 60-85% adoption within a quarter.

Some clients are, particularly those using corporate cards with 1-2% cashback. The trade-off is straightforward: your client’s rewards are funded by your processing fees. The fair way to handle this is dual pricing — the ACH price is 2-3% lower than the card price, so the client capturing rewards pays for that capture directly. Most clients who do the math choose ACH. Some don’t, and that’s reasonable — they get rewards, you get reimbursed for the cost.

For established B2B clients, ACH return rates run under 0.5%. Returns happen for insufficient funds (most common), closed accounts, or rare authorization disputes. Business-to-business ACH transactions have a 2-banking-day return window in most cases, much shorter than the consumer ACH window. The dispute mechanism is materially less merchant-hostile than card chargebacks — most ACH disputes resolve through direct bank-to-bank processes rather than a card-network arbitration favoring the cardholder. Net of fraud and disputes, ACH is consistently safer for the merchant than cards on B2B transactions.

Send Us Your AR. We’ll Run the Card-vs-ACH Math on Your Actual Invoices.

If you invoice other businesses and haven’t had your card volume audited line by line, you almost certainly have $5,000 to $80,000 a year of recoverable margin sitting in card transactions that could move to ACH. Send Brookside one recent merchant statement plus a sample of your invoicing flow and we’ll calculate your specific savings, identify which clients are best candidates for ACH migration, and walk through the implementation path that fits your invoicing platform. The math takes us about thirty minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for Free ReviewNo obligation • No pressure • Response within one business day

See what a statement review looks like →