Can Merchants Set Card Minimums?

Yes — But Only Up to $10, and Only on Credit

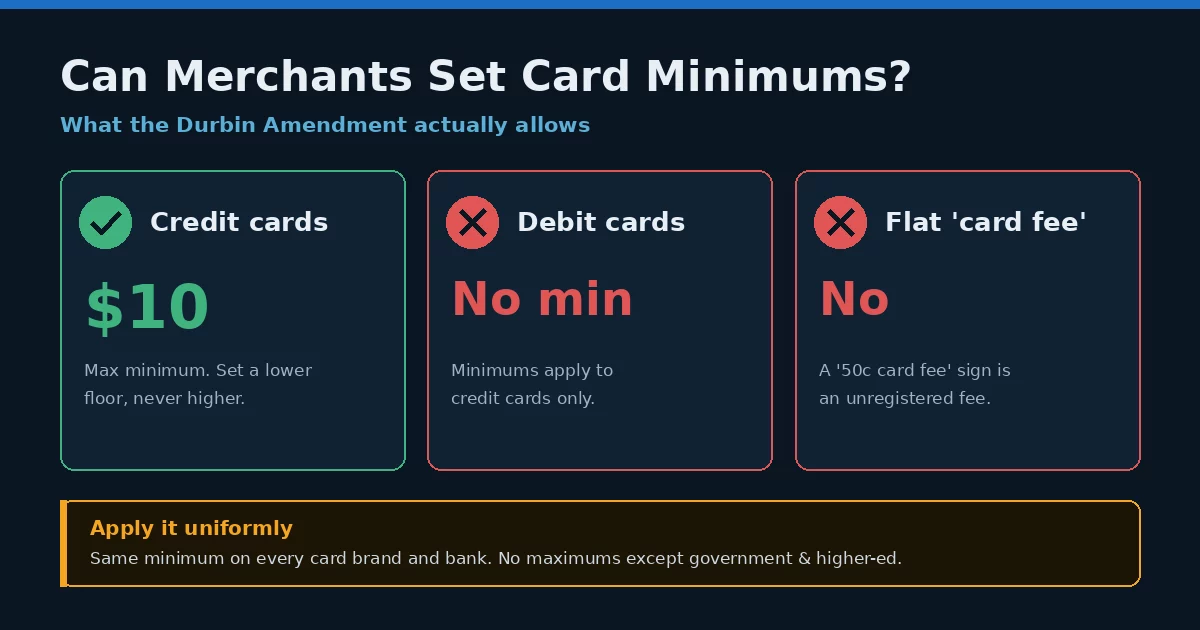

Merchants can set card minimums, but the rule is narrower than the handwritten signs taped to most counters suggest. Under the Durbin Amendment — part of the 2010 Dodd-Frank Act — you may require a minimum purchase before a customer pays by credit, and that floor is capped at $10. You can post a lower threshold; you cannot go above it.

This was not always allowed. Before Durbin, all four major networks flatly prohibited the practice in their merchant agreements — you were expected to honor a valid card for a pack of gum. The law overrode that ban and handed the Federal Reserve authority over the ceiling, which the Fed set at $10, where it remains. So the headline answer is yes — with conditions that matter more than the yes.

It helps to be precise about the words. A credit card minimum is a floor on the purchase amount before someone may pay with plastic — not a fee, not a surcharge, and not anything you can attach to a debit card. The rule sits in its own narrow corner, and that corner is well defined: how high you can go, which products it covers, and how evenly you have to apply it.

The Four Conditions Your Card Minimums Have to Meet

The allowance is real, but it comes wrapped in conditions written into both the law and your merchant agreement. Get any one of them wrong and a legal practice becomes a violation.

- Credit only — debit transactions may never carry one.

- $10 ceiling — you can require less, never more than $10.

- Same across brands — you cannot require it for Visa but waive it for Mastercard.

- Same across banks — you cannot apply it to one issuer’s customers and not another’s.

American Express does not spell this out the way the others do, but the safe practice is to treat Amex identically. The theme across all four conditions is consistency: the floor has to be identical for every brand and every issuing bank you take. Singling one out — a higher bar for one network, or a requirement that lands on only some issuers — breaks your merchant agreement even when the dollar figure itself is perfectly legal.

The Signs That Get Merchants Fined

The most common counter signs are the ones that quietly cross the line. A flat “card fee” — the “50¢ fee on all purchases” sticker — is not a floor at all. It is an unregistered surcharge, and charging it without following the formal surcharge rules violates both the network agreements and the spirit of the Durbin Amendment. A floor over $10 is out, and so is any maximum: with two narrow exceptions, you cannot cap how much a customer puts on a card.

Those exceptions are specific — federal government agencies and accredited institutions of higher education may set maximum amounts. Everyone else may not. And the penalty for getting this wrong is not theoretical: non-compliant fees and floors can trigger fines from the networks and, in repeat cases, termination of your merchant account.

None of this means card minimums are a bad idea everywhere — a coffee shop with a clearly posted $5 credit floor is well inside the rules. The trouble starts when the practice drifts: a bar above $10, a flat fee dressed up as a floor, or a rule quietly applied to debit. Those are the versions that turn a merchant’s right into a merchant-agreement violation.

The “$0.50 fee on purchases under $X” sign taped to the register is the classic trap. That flat charge is neither a legal floor nor a registered surcharge — it is the fastest route to a chargeback complaint, a network fine, or a processor that drops you.

What Actually Recovers Small-Ticket Cost

Here is the uncomfortable truth about card minimums: even done correctly, they mostly cost you sales. A customer told to spend $10 before they can use plastic often walks, and you have turned a small sale into no sale. The owners who actually claw back the cost of a $3 purchase use a different set of tools — ones that recover the fee instead of refusing the transaction.

The compliant options are dual pricing (posting a cash price and a card price), a properly registered and itemized credit-only surcharge, or steering small and recurring charges toward lower-cost rails like ACH. Each is legal when it is set up to the letter — registered, disclosed, and applied only where the rules permit — and unlike a $10 floor, each one keeps the sale and offsets the fee.

Put plainly, a posted floor is a defensive move: it heads off a money-losing sale rather than wins a profitable one. The alternatives are the offensive version — they let you take every sale and still come out whole. For a counter that runs a steady stream of small tickets, that difference is the whole argument against leaning on minimums at all.

Which lever fits depends on your state, your average ticket, and your processor. A registered surcharge program suits a business running mostly credit volume; dual pricing reads cleanly at a quick-serve counter; an ACH option earns its keep on recurring or higher-dollar invoices. Each one is a deliberate setup rather than a sign you tape up over the weekend — which is exactly why it holds up when a customer or an auditor questions it.

Dual pricing, a registered surcharge, or an ACH option recover the processing cost a $10 floor simply forfeits. Set up correctly, they let you keep the small sale and stop eating the fee on it.

Why a $3 Sale Barely Breaks Even

The reason owners reach for a floor in the first place is the per-transaction fee. Processing runs roughly 1.5% to 3.5% of the sale, but it also carries a fixed per-item charge — and on a tiny ticket that flat piece swallows the margin. The percentage is almost beside the point when the sale is small enough. That pressure is real, and it is exactly what these signs are reacting to — the only question is whether a floor is the right tool for the job.

A $3 sale at about 2.6% plus a $0.10 per-item charge costs roughly $0.18 to process — an effective cost near 6% of the sale, almost all of it the fixed per-item piece. That flat charge is what makes small tickets feel like they barely break even.

That is the math a floor is trying to dodge. But forcing the customer to spend more rarely happens; more often the sale just disappears. Recovering the fee — through dual pricing, a compliant surcharge, or an ACH option — keeps the $3 and offsets the $0.18, which is the outcome the sign was reaching for all along. A posted floor can still earn its place at a very small shop, but for most counters it is the blunt version of a problem the compliant options solve more cleanly.

Frequently Asked Questions

No. The Durbin Amendment allows a floor on credit transactions only. Applying one to debit is not permitted, even under $10.

$10. The Federal Reserve sets the ceiling, and it currently sits at ten dollars. You can require less, but never more.

No. An unregistered flat fee on card sales violates network rules and the Durbin Amendment. To pass on the cost, use a properly registered surcharge or dual pricing instead.

Generally no. Only federal government agencies and accredited institutions of higher education may cap how much a customer charges; other merchants may not.

Send Us a Statement. We’ll Build You a Compliant Way to Offset It.

A posted floor turns small sales away; a compliant surcharge, dual-pricing, or ACH setup keeps them and recovers the fee. Send Brookside one recent statement and we’ll show you what small-ticket processing is actually costing you and which of the legal options fits your state and your counter. The review takes about fifteen minutes and commits you to nothing. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day

See what a statement review looks like →