PayGov Calls It a Flat Fee. A Lawsuit Says It Isn’t.

The “Flat” Fee That Wasn’t

Most PayGov complaints start in the same place: the final screen of a utility payment, where a “convenience fee” lands on top of a water or electric bill and turns out larger than the round number people expected. PayGov.US is the third-party processor behind thousands of municipal payment pages, and that fee — how it is set, how it is disclosed, and how it grows — is now the subject of a class action.

For a resident it reads as a one-time irritation on the way to keeping the lights on. For a utility director or city finance officer it is something to understand carefully, because the page carrying that fee has your seal on it even when the company collecting it does not.

What the Indiana Class Action Alleges

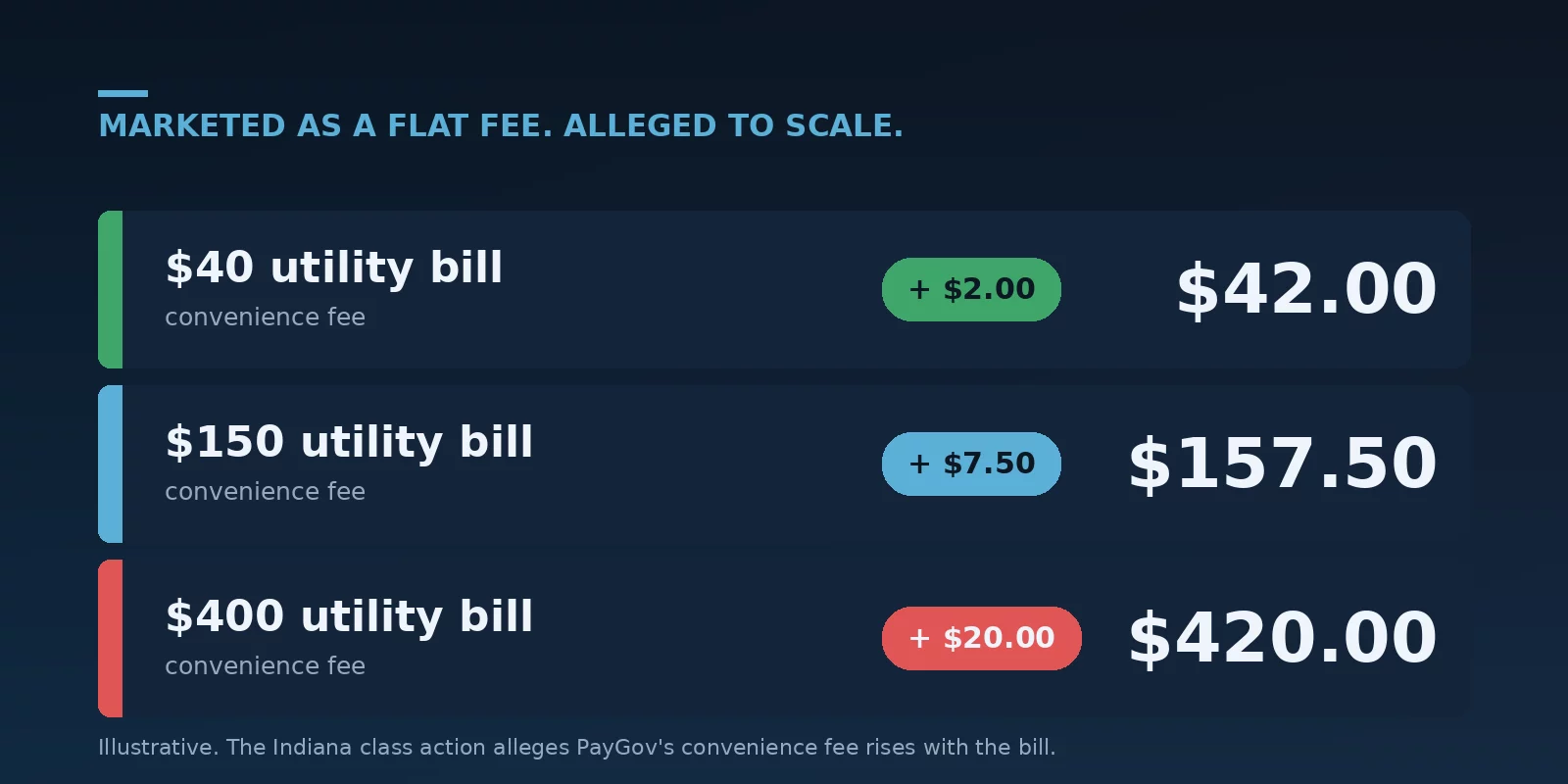

In late 2025, two Indiana residents filed a class action in Marion Superior Court against PayGov.US. The complaint alleges the company charges undisclosed, variable convenience fees on utility bills — fees presented as flat but that in practice climb with the size of the bill, so the largest bills carry the largest charges. It further alleges PayGov does not disclose the base fee or that it scales, and that the company uses a domain and flag imagery resembling an official government site. The claims are brought under the Indiana Deceptive Consumer Sales Act and a theory of unjust enrichment.

These are allegations; the matter has not been decided, and PayGov has not been found liable. But the shape of the grievance is worth understanding because it is structural, not a one-off billing error.

The core claim is simple: the charge is sold as a flat convenience fee but billed as a variable one. The residents with the biggest bills — often the ones already stretched — end up paying the most for the privilege of paying.

Why Utility Bills Are Built for This

The reason a fee like this survives is the same reason it is hard to notice. The utility pays the processor little or nothing; the entire charge is shifted onto the resident at checkout. That removes the one force that normally pushes a price down — a customer who feels the cost — because the agency that signed the contract never sees the fee on its own books.

The payer has no leverage either. You cannot route your water bill through a cheaper processor; you pay whatever the city’s page presents, on a bill you cannot skip. A non-discretionary payment plus a fee at the only available checkout is precisely where an inflated, poorly disclosed charge can live for years. Calling it a convenience fee only helps — it sounds like a courtesy rather than the cost of paying a bill you owe.

There is no shopping around for your own water bill. Whatever the municipal page charges to take a card is what you pay — which is why the disclosure on that page matters more than usual.

PayGov Isn’t the Only One

It would be a mistake to read this as one bad actor. PayGov is one of several processors that run government and utility payment pages, and the convenience-fee model is industry-wide. Paymentus, a publicly traded platform used by tens of millions of consumers, and InvoiceCloud are the larger names cities route water, sewer, and electric billing through; municipalities switch between them regularly. The lawsuit named PayGov, but the pattern — a third party collecting a percentage at the city’s checkout — is the norm across the category.

What the complaint highlights is less about one logo than about a design choice: when the vendor’s page looks like the government’s own, residents reasonably assume the fee is the city’s, set by the city, going to the city. Often none of that is true. It is also why PayGov complaints tend to rhyme with the gripes about every other vendor in the category — the logo on the page changes, but the percentage skimmed at checkout does not.

The suit points to government-resembling domains and flag imagery. Whatever a court makes of it, the lesson for an agency is plain: residents should never have to guess whether they are dealing with the city or a contractor.

What a Utility Can Do Instead

An agency is not stuck with whatever its current vendor presents. With its own merchant account and a payment page it controls, a utility can disclose the fee honestly — the amount, and whether it varies — which addresses the exact deception the Indiana complaint describes. It can hold the charge to the true cost of acceptance or absorb it into the budget, offer a low-flat-fee bank-debit option for residents who cannot take a percentage on top of a utility bill, and make sure the page plainly identifies who is being paid.

That is the work behind utility payment processing run in-house, and the broader principle behind government payment processing an agency owns rather than rents. The goal is not to make card acceptance free; it is to make sure a resident paying a bill they owe is not quietly charged more, on a page they were led to believe was the city’s. For a household already watching every dollar on a water or power bill, that distinction is not cosmetic — it is the difference between a fee a resident understands and the one that becomes the next complaint filed against the city.

Even keeping a fee, simply showing it honestly up front — the dollar amount, and that it scales with the bill — answers most of what the lawsuit alleges. Transparency costs nothing and is the one thing a captive payer is actually owed.

Questions a Utility Should Ask

If your agency runs payments through PayGov, Paymentus, InvoiceCloud, or a similar contract, a few questions surface what residents actually experience. What is the all-in fee on a $50 bill versus a $500 bill — is it genuinely flat, or does it climb? Is that fee shown clearly before the final screen? Does the payment page identify the processor as a third party rather than the city itself? Who owns and secures the payment data? And is there a no-fee bank-debit path for residents who cannot absorb a percentage?

The answers tell you whether you are offering a service or quietly hosting a toll on people who have no choice but to pay it.

Frequently Asked Questions

They center on cost and transparency: the convenience fee charged on utility and government payments, which an Indiana class action alleges is undisclosed and variable — rising with the bill rather than the flat fee it is presented as — along with government-resembling branding on the payment page.

PayGov presents it as a flat fee. The class action alleges that in practice the charge scales with the size of the payment and that this is not disclosed up front. That allegation has not been decided in court.

No. PayGov.US is its own Indianapolis-based processor. AllPaid (formerly GovPayNet), Paymentus, and InvoiceCloud are separate vendors operating in the same government and utility payments space.

Yes. By running its own merchant account and payment page, a utility can disclose or absorb the fee, hold it to the true cost of acceptance, and add a low-flat-fee bank-debit option — while keeping control of the data and the branding.

Find Out What Your Residents Actually Pay at Checkout.

If your utility or agency runs payments through PayGov or a similar vendor, send Brookside the contract and a recent statement. We’ll show you the true all-in cost a resident pays on a small bill versus a large one, what the same volume would cost with a page you control, and how to disclose or cut the fee before a contract renews. The review takes about fifteen minutes and commits you to nothing. For background on surprise-fee protections, see the CFPB’s consumer guidance.

Get Your Free Payment Cost ReviewNo obligation • No pressure • Response within one business day

See what a statement review looks like →