AllPaid Alternatives for Courts and County Agencies: What Switches, What Stays

What You’re Actually Shopping For When You Look at AllPaid Alternatives

Most agencies start looking for a way out for one reason: a resident complained about the fee. Pay a court fine, a probation cost, or a bail amount through the county page and a service charge of roughly 4 to 5% lands on top at checkout, paid by the person clearing the obligation, not the office collecting it. AllPaid — formerly GovPayNet — is the company behind thousands of those pages, and once a clerk or finance director hears the complaint enough times, the question becomes what else is out there.

The trap is treating it as a vendor swap. The thing you are actually shopping for is not a different logo charging a slightly lower percentage — it is a different arrangement: who bears the cost, who owns the payment data, whether acceptance is exclusive, and how tightly the payment page is wired into your case-management system. Get those four variables right and the fee takes care of itself. Get them wrong and you have traded one pass-through markup for another.

What AllPaid Alternatives Actually Look Like

There are two families. The first is the other aggregators — Catalis (which absorbed nCourt), Point & Pay, Paymentus, InvoiceCloud, and the rest of the govtech field. Most of them run the same model the incumbent does: the agency pays little or nothing, and the entire cost is loaded onto the payer as a “convenience fee.” Switch from one to another and a $200 fine might cost the resident $7 instead of $8 — a rounding error, not a fix.

The second family is the one that changes the arrangement instead of the brand: your own merchant account behind a payment page the agency controls. With a merchant account in the county’s name, you set the terms — absorb the cost into the budget, hold any charge to the true cost of acceptance, or offer a low-flat bank-debit lane. That is the real government payment alternative, and it is the difference between renting a toll booth and owning the road.

Trading one aggregator for another percentage-fee aggregator leaves the structure intact: your residents still pay the markup, an outside vendor still owns the data, and the rate still has no downward pressure. A lower percentage is not a different model.

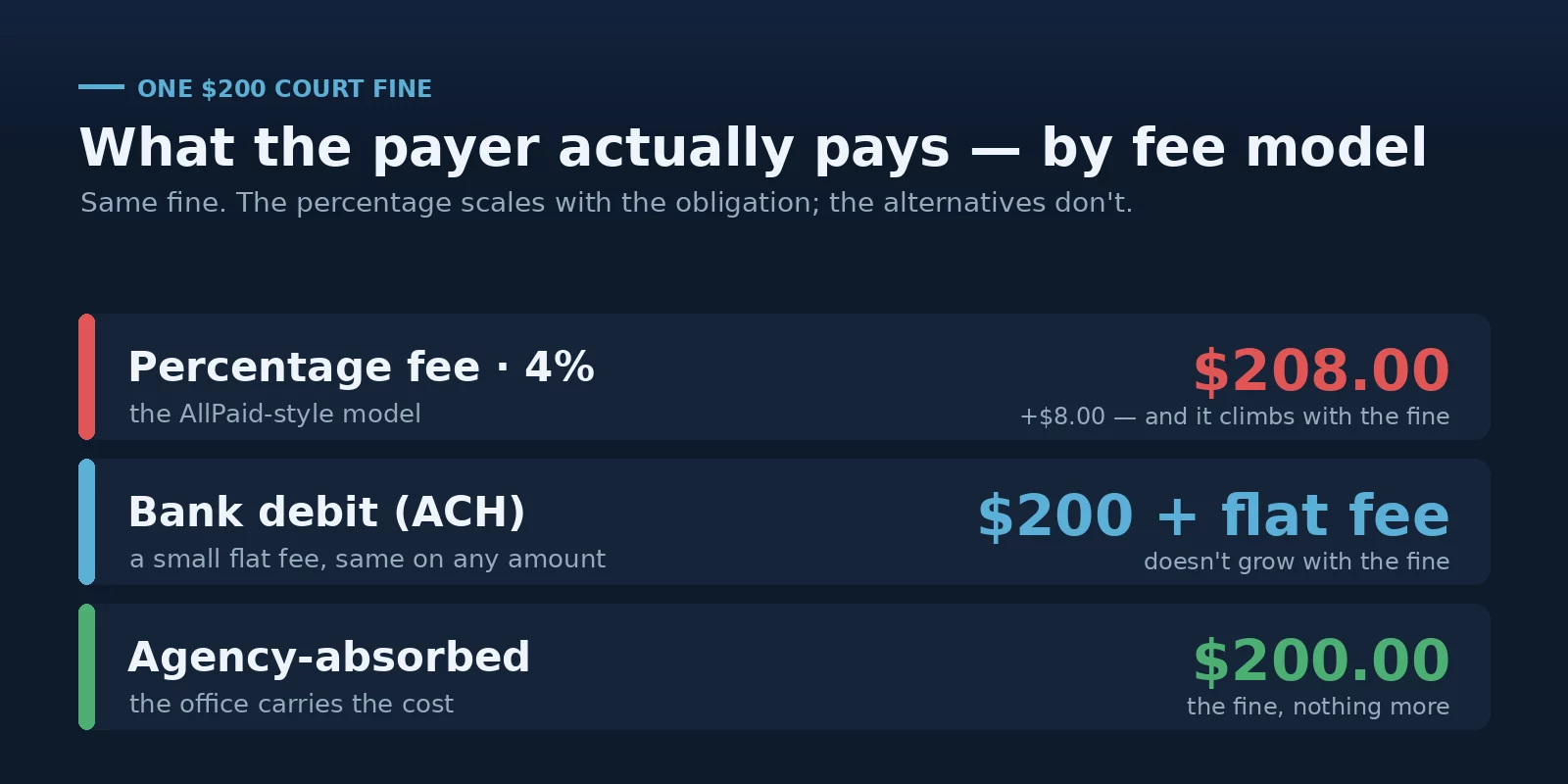

One $200 Fine, Three Fee Models

The clearest way to compare these options is to run the same payment through each model. Take a $200 court fine paid by card. Under a percentage convenience fee at 4%, the payer hands over $208 — and by phone, where rates reach 5.25% plus minimums, more. Under a low-flat bank-debit (ACH) option, the payer covers the fine plus a small fixed fee that doesn’t grow with the amount. And under an agency-absorbed model, the resident pays $200.00 flat — the office carries the processing cost the way a private business does.

The percentage model is the only one of the three where the cost rises with the size of the obligation, which means it falls hardest on the people paying the largest fines, restitution, or bail. The other three break that link. None of them is automatically right — absorbing cost has a budget line, flat fees need volume to pencil out — but seeing the four side by side is what turns a vague “AllPaid fees feel high” into a decision you can actually defend at a commission meeting.

In the absorbed and ACH models the agency, not the resident, decides how much the convenience of paying by card should cost — and keeps the option to make a phone payer’s rate humane instead of the highest of all.

When a Switch Makes Sense — and When It Doesn’t

A switch makes sense when the numbers and the timing line up: your card volume is high enough that residents are collectively paying real money in convenience fees, your current contract is at or near renewal, and the vendor is delivering nothing beyond a payment screen you could own. Those are the conditions under which moving off a court payment processor pays for itself quickly and quietly.

Staying makes sense, at least for now, when the term has years left with a stiff exit penalty, when the integration into your case system is genuinely deep, or when your volume is low enough that the fees residents pay are modest in absolute terms. Honest answer: if you process a handful of card payments a month, the savings will not justify the project. The point of evaluating the options is not to switch reflexively — it is to know, before the contract auto-renews, which situation you are actually in.

Most of these contracts auto-renew on a fixed term. The cheapest moment to move is the renewal window; the most expensive is the month after you miss it. Pull the agreement and find the date before anything else.

What Doesn’t Switch: The Case-Management Integration

The reason these vendors are sticky is rarely the payment processing itself — that is a commodity. It is the wiring. These vendors post payments back into the court or county case-management system in real time, clear the balance against the right case number, and carry the jurisdiction code residents have learned to enter. That integration is the moat, and it is the part a migration has to preserve, not the part it gets to ignore.

The good news is that the integration and the pricing are separable. A modern payment page on your own merchant account can post to the same case system through an API while the agency, not an aggregator, sets the rate and holds the data. What moves is the money flow and the margin; what stays is the citizen experience and the back-office posting. A real alternative keeps the moat and changes the toll.

Ask any candidate vendor to show how it posts to your case-management system and who sets the payer fee. If those two answers come from the same locked bundle, that is the lock-in — not the technology.

How to Evaluate an AllPaid Alternative

Whatever you are comparing against, the same short list separates a genuine AllPaid alternative from a re-skinned toll. What is the all-in cost to a payer online versus by phone, including every minimum and add-on? Who owns and secures the payment data once it leaves your page? Is acceptance exclusive, and what is the term and exit penalty? Can it post to your case-management system without locking the pricing to the platform? And is there a low or no-fee path — a flat bank debit — for residents paying a court debt they can barely cover?

Run those questions past your current contract first; the gaps are usually where the AllPaid fees you have been hearing about actually live. The companion read on this — the AllPaid complaints themselves — walks through the fee math and the GovPayNet track record in detail, and the broader picture sits with government payment processing run in-house and the government payment portal the agency owns outright.

Frequently Asked Questions

It depends on what you are optimizing for. Other aggregators — Catalis, Point & Pay, Paymentus, InvoiceCloud — are drop-in but usually keep the same percentage convenience fee passed to the payer. The structural fix is your own merchant account behind a page the agency controls, which lets you absorb, flatten, or cap the fee instead of inheriting a vendor’s rate.

It does not have to. The payment processing and the case-system posting are separable: a modern page on your own merchant account can post to the same system through an API while you set the rate. The integration is the part to preserve in a migration, not the reason to stay.

Yes — AllPaid is the rebranded GovPayNet, the court-and-jail payment vendor founded in the late 1990s and passed between owners since. Same platform and broadly the same convenience-fee model under a newer name.

Only if it changes the fee model, not just the vendor. Swapping one percentage-fee aggregator for another saves cents. Moving to an absorbed, flat, or low-fee bank-debit model is what meaningfully lowers what a resident pays on a fine or restitution.

See What a Real Alternative Would Cost — and Save.

If your agency is on AllPaid, Catalis, Point & Pay, or a similar contract, send Brookside the vendor agreement and a recent statement. We’ll lay your current all-in payer cost next to what the same volume would cost under a flat, absorbed, or in-house model — and flag the renewal date and any exit penalty before it auto-renews. The review takes about fifteen minutes and commits you to nothing. For background on surprise-fee protections, see the CFPB’s consumer guidance.

Get Your Free Payment Cost ReviewNo obligation • No pressure • Response within one business day

See what a statement review looks like →