Childcare Payment Processing: Card vs ACH on Tuition

The Payment Method Decides What Tuition Costs You

Childcare payment processing is shaped by one fact most centers underestimate: tuition is a large, recurring charge. A monthly payment of $1,000 to $2,000 per child, billed to the same families every month, behaves nothing like a $40 retail sale — and at that size, whether a family pays by card or by bank transfer is the single biggest cost decision a director makes. It has very little to do with the rate on a statement and almost everything to do with which rail the money travels.

The gap is stark. A $1,200 tuition payment on a card at the standard 2.9% plus $0.30 costs about $35. The same payment by ACH bank transfer is a flat fee — often a dollar or two, and commonly capped near $5 by the billing platforms. Multiply that difference across a full enrollment and twelve months and it climbs into the thousands, on a margin that centers rarely have to spare.

Billing platforms charge one fee for cards and a much lower one for ACH. Unless you actively steer families toward bank transfer, the convenient default is the card — and you quietly absorb the most expensive way to collect every month.

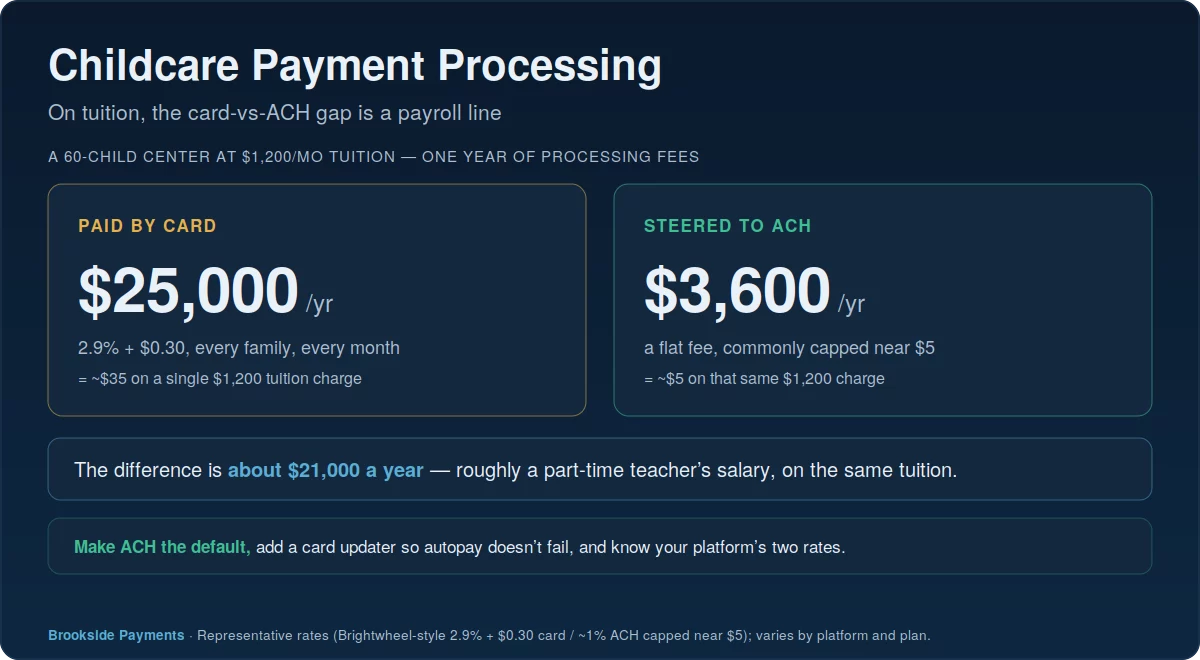

The Card-vs-ACH Gap Is a Payroll Line

Run the arithmetic at center scale and the stakes become obvious. A sixty-child program at $1,200 a month, collecting entirely by card, pays roughly $25,000 a year in fees. The same program steering families to ACH pays closer to $3,600. That $21,000 difference isn’t a rounding error on a spreadsheet — on a childcare budget it’s a part-time teacher, a classroom of supplies, or the cushion that keeps the doors open in a slow enrollment season.

This is why ACH should be the default rail for tuition, not an option buried three taps deep. Because it’s a flat fee rather than a percentage, its cost doesn’t grow as tuition rises — a five-dollar transfer is five dollars whether the payment is $900 or $2,000. Cards still have a role for families who prefer them, but they should be the deliberate exception, not the path of least resistance that erodes your margin every first of the month.

The whole reason ACH wins on tuition is that its cost is fixed while a card’s scales with the payment. On a $1,200 charge that’s roughly $5 versus $35 — the same difference, repeated across every family, every month of the year.

Steering Families to ACH — and Who Covers the Card Fee

The most effective move in childcare payment processing isn’t negotiating a lower card rate; it’s making ACH bank transfer the obvious, default way families pay. When you set up autopay, lead with bank transfer, present it as the simplest option, and reserve cards for parents who specifically want them. Most families on autopay don’t have a strong preference — they want it handled — so the default you choose largely decides your blended cost.

Some centers go further and pass the card fee to the family who chooses to pay by card, which is allowed in many places but regulated: passing a credit-card surcharge is governed by state law and card-network rules, can’t be applied to debit cards, and should be disclosed clearly before payment. For most childcare programs the simpler, friendlier path is to make ACH free and effortless rather than to charge families a fee — but if you do pass it along, confirm what your state permits first. This isn’t legal advice.

Failed Autopays Cost More Than the Rate

On recurring tuition, the card rate isn’t the only number that bleeds. Cards kept on file for autopay expire, get reissued after fraud, or bounce — and every failed tuition charge means a missed deposit, an awkward “your payment didn’t go through” message to a parent, and staff time spent chasing money you already earned. For a small center where the director is often also the teacher, that follow-up is time taken straight from the classroom.

A card updater — which automatically refreshes expired or reissued card numbers behind the scenes — quietly prevents a large share of those failures before they happen, the same way it does for gyms and other recurring-billing businesses. When you evaluate a processor or platform, the card-updater and retry tools deserve as much attention as the headline rate, because tuition you don’t collect on time is more expensive than a slightly higher fee, and it’s the most overlooked cost in childcare payment processing.

A card updater recovers tuition that would otherwise fail silently and turn into a phone call. On autopay-heavy billing, your collection rate matters as much as your processing rate.

How to Audit Your Childcare Payment Processing

Start with your real effective rate, split by rail: what you actually pay to collect tuition by card versus by ACH, pulled from your processing statement and your platform’s payout reports. Then ask the questions that move money: is ACH the default, easy option for families; what exactly are your platform’s two rates; and is a card updater switched on for autopay. Centers that also run K-12 grade tuition have a related but different profile — school payment processing — while this is daycare payment processing specifically, built around recurring monthly tuition.

Make ACH the default, switch on a card updater, and know your platform’s two rates cold. Those three moves keep far more tuition than negotiating a card rate ever could — and on a thin margin, every point matters.

Frequently Asked Questions

ACH bank transfer. It’s a flat fee — often a dollar or two, commonly capped near $5 — instead of a percentage, so it doesn’t grow with the tuition amount. A card costs about $35 on a $1,200 payment; ACH costs a fraction of that. Make ACH the default and offer cards as an option for families who want them.

Yes — they bundle it into their billing, typically around 2.9% + $0.30 per card transaction and a lower flat fee for ACH. It’s convenient, but the bundled card rate is rarely the cheapest path. Know both of your platform’s rates, steer families to ACH where you can, and compare the all-in cost before assuming the built-in option is your only one.

Usually expired or reissued cards on file. When a parent’s card is replaced, the stored number stops working and the autopay charge fails silently. A card updater refreshes those numbers automatically, recovering most of those payments before they bounce — without it, you’re left chasing parents and waiting on tuition you already earned.

Tools to Keep More of Every Tuition Payment

Send Us One Statement. We’ll Split Card vs ACH.

Most childcare directors have never seen what they pay to collect tuition by card versus by ACH, side by side. Send Brookside a recent statement and your enrollment and we’ll compute your real cost on each rail, show how much you’d keep by steering families to bank transfer, and flag whether a card updater would stop the autopay failures eating your staff’s time. The read takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Check Our Center’s Real RateNo obligation • No pressure • Response within one business day

Figures shown are representative; Brightwheel, Procare, and other platforms set their own rates, which vary by plan and enrollment. Surcharge and convenience-fee rules vary by state. Confirm current pricing and rules directly before relying on them.