Pharmacy Payment Processing: The Rule No Other Store Has

Pharmacy Payment Processing Has a Rule No Other Retailer Has

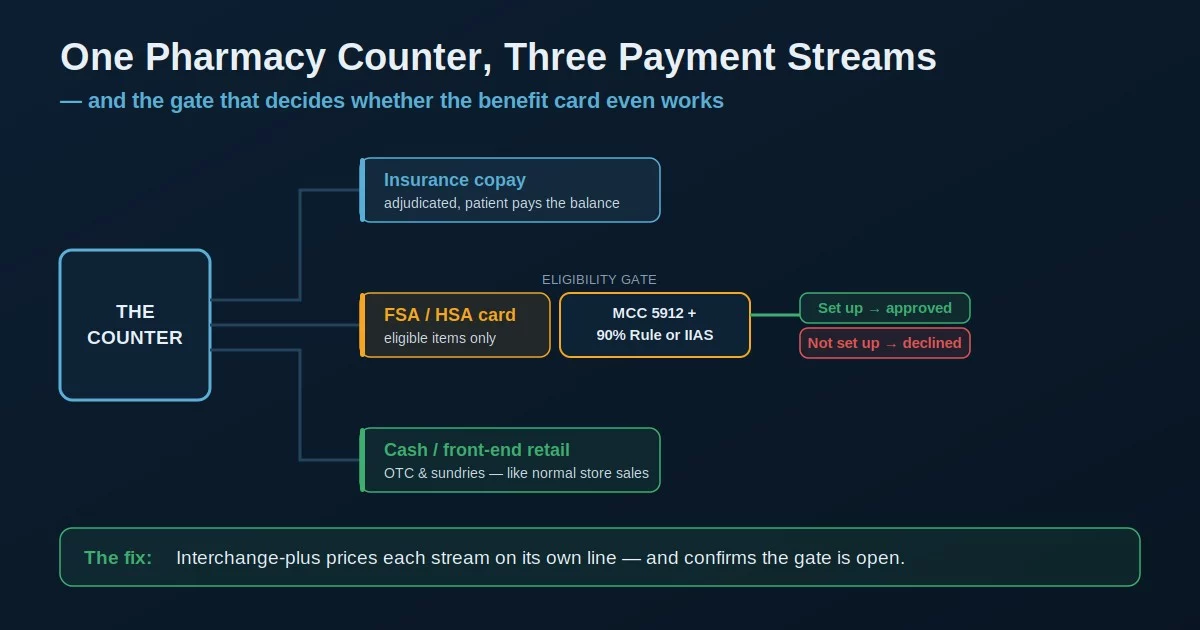

Pharmacy payment processing looks like ordinary retail and runs on rules ordinary retail never touches. A drugstore takes money in three different ways at the same counter — an insurance copay, a cash sale on the front-end shelf, and a patient paying out of pocket — and one of those payment types, the flexible-spending and health-savings card, will be declined at your register unless your store is set up a very specific way. The rate you pay per swipe matters, but it is the smaller half of the story. The bigger half is whether your system is even allowed to take the card the customer is holding.

That single fact reshapes how an independent owner should think about the whole setup. Get the setup wrong and you lose sales you should have captured and pay more than you should on the ones you do. Get it right and the same counter quietly runs cleaner and cheaper, without changing a thing about how you fill prescriptions.

Your Pharmacy System Usually Picks Your Processor

Most of these decisions get made by accident. Almost every independent runs a pharmacy management system — PioneerRx, BestRx, PrimeRx, Liberty, Rx30 — and most of them ship with an integrated point-of-sale that bundles or steers a card processor. The convenience is real: the front-end sale, the copay, and the prescription all reconcile inside one system, and there is nothing separate to wire up.

The cost of that convenience is leverage. When the processor comes attached to the software, the rate is usually a single blended number — one percentage averaged across debit, rewards cards, and the rest — and you rarely get to shop it against anyone else without the vendor’s blessing. It means your pharmacy credit card processing rate was set by whoever your software vendor partnered with, not by you. A blended rate is the opposite of what these stores want, because the card mix here is unusually varied, and averaging it together hides exactly where the money goes. The only way to know whether the bundled rate is fair is to put it next to an interchange-plus quote on your real volume.

Blended pricing charges the same percentage on every card, so a low-cost debit transaction and a high-cost rewards card look identical on your statement. Interchange-plus breaks out the network cost and the processor’s markup as separate lines — the only view that lets you see what each stream of the business actually costs.

The FSA and HSA Cards Won’t Work Unless You’re Set Up for Them

This is the part of pharmacy payment processing that has no equivalent in normal retail. Flexible spending account and health savings account cards — FSA and HSA cards, plus their HRA cousins — can only be used on items the IRS counts as qualified medical expenses under Section 213(d). To honor that, the card networks require the merchant to prove eligibility before the charge goes through. A pharmacy has two real paths to that proof.

The first is the IRS 90% Rule: a drug store or pharmacy under MCC 5912 whose prior-year sales were at least 90% prescriptions and eligible health products can register through SIGIS and be treated as a healthcare merchant, so plan administrators approve the cards. The second is an Inventory Information Approval System — an IIAS — that checks each item at the register line by line and auto-substantiates the purchase. The trade-off is cost and paperwork: a SIGIS-certified IIAS historically starts around $10,000 and is overkill for most independents, while the 90% Rule is the affordable path but requires annual re-registration per location and does not auto-substantiate, so customers keep their receipts.

If a pharmacy hasn’t registered for the 90% Rule and hasn’t implemented an IIAS, card issuers are required to decline FSA and HSA cards outright. The customer is standing at your counter with a valid benefit card and your register turns it away — a lost sale and a frustrated patient, caused entirely by a setup gap most owners don’t know they have.

Your Merchant Category Code Is Doing More Than You Think

Behind all of this sits a four-digit number most owners never see: your merchant category code. Your store should be classified under MCC 5912, Drug Stores and Pharmacies. That code is what tells the benefit-card networks you’re a healthcare merchant in the first place, and it influences the interchange your card transactions are priced at. A store that was set up by a generalist and miscoded as ordinary retail can run into two problems at once — FSA and HSA cards that mysteriously decline, and an interchange profile that doesn’t reflect the business it actually is.

It’s a quiet, structural detail, and it’s exactly the kind of thing that gets missed when a processor is bundled into software and nobody audits the account setup. Confirming the code is correct costs nothing and occasionally fixes a problem an owner has been working around for years. It’s the cheapest fix on this list and one of the most overlooked.

When the processor arrives attached to your pharmacy management system, the account is often provisioned quickly and generically. Nobody’s job is to confirm the MCC, verify the 90% Rule registration, or check the interchange tier — so those settings drift to defaults that quietly cost you. An independent audit of the account is the only thing that catches it.

Where the Rate Actually Hides

The reason interchange-plus fits these stores so well comes back to those three streams. The insurance copay, the cash sale up front, and the out-of-pocket prescription each carry different card types and different true costs, and a blended rate flattens them into one number you can’t interrogate. The front-end retail — over-the-counter products, gifts, sundries — behaves like normal store sales and can even support a cash-discount or dual-pricing approach if you want it to. The pharmacy-counter transactions behave like healthcare. Pricing them as if they’re the same thing leaves money on the table in both directions.

Seen as an effective rate per card type rather than one blended average, an owner almost always finds that the parts they can’t see on the quote — the FSA and HSA setup, the MCC, the channel of each sale — are where the real cost and the real opportunity live. Put each on its own line and the picture finally makes sense.

What Actually Lowers a Pharmacy’s Card Cost

The levers that move the number are structural, not a tenth of a percent on the swipe.

- Move to interchange-plus so the copay, the cash sale, and the patient-pay prescription are each priced on their true cost instead of an average.

- Confirm MCC 5912 so you’re classified as the healthcare merchant you are — it’s what makes the benefit cards work and prices your interchange correctly.

- Set up FSA and HSA acceptance properly with the 90% Rule registration (or an IIAS if you genuinely need auto-substantiation) so those cards stop declining at the register.

- Keep the processor shoppable — a pharmacy merchant services account you control rather than one rented from your software — so the rate stays under your control.

Pharmacy payment processing is a setup problem before it’s a rate problem. The owner who audits the whole account — the embedded rate, the MCC, the benefit-card configuration, and the three streams — almost always finds more in the parts that never appear on the quote than in the one number that does.

Frequently Asked Questions

Because the store isn’t set up to accept them. A store needs MCC 5912 plus either a SIGIS 90% Rule registration or an IIAS at the point of sale. Without one of those, card issuers are required to decline FSA and HSA cards under IRS rules — even when the customer’s card is perfectly valid.

Not always. A bundled processor is built for convenience and usually priced on a blended rate that averages your card types together. It may be competitive, but the only way to know is to compare it against an interchange-plus quote run on your real mix of copays, cash sales, and patient-pay transactions.

An IIAS verifies each item’s eligibility at the register and auto-substantiates the purchase, but the certified systems are expensive. The 90% Rule is the affordable path for most independents — register through SIGIS, attest that 90% of sales are eligible, and the cards work — but it doesn’t auto-substantiate, so customers keep their receipts.

Keep reading on rates, setup, and the medical verticals

Send Your Statement. We’ll Check the Rate, the Code, and the Benefit-Card Setup.

If your processor came bundled with your pharmacy management system, send Brookside one recent statement. We’ll break it into an interchange-plus view by card type, confirm you’re coded MCC 5912, and check whether your FSA and HSA acceptance is actually set up — the gap that quietly declines benefit cards. The review takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day