In Restoration, the Carrier Pays the Claim — the Card Covers the Deductible and the Rest

In Restoration, the Carrier Pays the Claim — the Card Covers the Deductible and the Rest

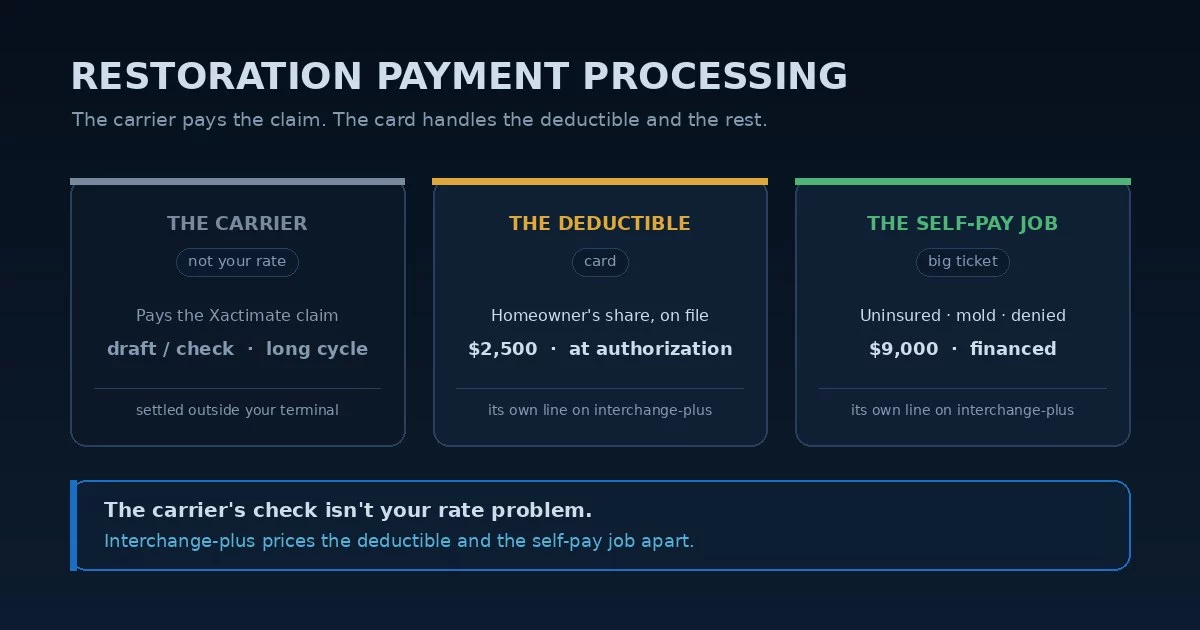

Restoration payment processing is unusual because the biggest payer never touches a card. On a water or fire job, the insurance carrier pays the bulk of the claim — priced line by line in Xactimate, settled in drafts over a long cycle. What runs through the card terminal is everything the homeowner owes on top of that: the deductible, the betterments and upgrades the policy won’t cover, and the fully self-pay job — the mold remediation, the small loss below the deductible, the denied claim. That card stream is narrow next to the claim, which is exactly why it gets ignored, and exactly why restoration payment processing tends to run on whatever blended rate came bundled. The headline percentage nobody shopped is quietly overcharging the one stream the homeowner actually swipes.

That single fact reshapes how an owner should think about the setup. Get restoration payment processing wrong and a rate that looks irrelevant against a $40,000 carrier claim is silently expensive on every $2,500 deductible and every self-pay mold job you run all year. Get it right and the card stream is priced on what it actually costs, instead of an average nobody ever questioned.

Because the Card Is the Small Half, Nobody Prices It

Most restoration payment processing decisions get made by accident, and for a specific reason: all the attention goes to the claim. The estimating happens in Xactimate, the fight is with the adjuster over scope and supplements, and the big money arrives from the carrier — so the deductible and the self-pay work feel like an afterthought, collected on whatever processor came attached to the field or billing software. The convenience is real, and the card volume looks small enough that shopping the rate never reaches the top of the list.

The cost of that convenience is leverage. When the processor is whatever was bundled and the card stream is treated as a rounding error, the rate is usually a single blended number nobody ever questioned. It means your restoration payment processing rate was set by default, not by you — and across a year of deductibles, betterments, and self-pay remediation, that default adds up. As with any home services payment processing setup, the bundled processor is rarely the one you’d have chosen, and the only way to know whether the rate is fair is to put it next to an interchange-plus quote on your real card volume — small as it feels against the claim.

A blended rate charges the same percentage on a $2,500 deductible and a $9,000 self-pay mold job, even though those cost the processor very different amounts. Interchange-plus breaks out the network cost and the processor’s markup as separate lines — the only view that shows what the part of the work the carrier doesn’t pay is actually costing you.

The Deductible and the Self-Pay Job Are Priced as One

Here is the structural problem at the center of restoration payment processing. The deductible is the homeowner’s required share of a covered claim — sometimes a few hundred dollars, sometimes the five figures of a percentage-based windstorm deductible — collected by card, ideally on file at the work-authorization stage. The self-pay job is different: an uninsured loss, a denied claim, or a mold remediation the policy excludes, paid entirely out of pocket and often large enough to finance. And the betterment sits between them — the upgrade beyond like-kind-and-quality that the carrier won’t fund. A blended rate is a single compromise stretched across all of it, so it is never actually right for any one piece.

On interchange-plus, those pieces stop fighting each other. The deductible shows up on its own line, the financed self-pay remediation shows up on its own line, and you can read and shop each instead of trusting one number to cover all of it. For a restoration contractor running steady deductible volume alongside uninsured work, separating them is where restoration payment processing stops leaking. A restoration merchant account priced this way shows the card stream honestly instead of burying it under the claim. Priced apart, restoration payment processing stops letting the deductible and the self-pay job blur into one rate.

A blended rate optimized for a small deductible is quietly expensive on a $9,000 self-pay mold job; one tuned for the big self-pay ticket overpays on every deductible. There is no single percentage that is fair to both, which is exactly what a bundled blended price hides.

Where the Percentage Actually Bites

The card stream is small against the claim, but it has its own big ticket: the self-pay job. A few points on a $9,000 uninsured remediation — or a large non-covered balance the homeowner has to absorb — is real money, which is why the self-pay side is where restoration payment processing deserves the most attention. The first lever here is consumer financing: letting a homeowner spread an uninsured remediation, a denied-claim repair, or a betterment over monthly payments while you get paid upfront. On work the carrier won’t fund, financing is often what turns a “we can’t afford that right now” into an approved job instead of a deferred one.

Two more levers belong on the self-pay side. On a larger out-of-pocket balance, paying by ACH bank transfer instead of card turns a percentage into a flat fee. And surcharging passes the card cost to the customer on a large credit-card payment, though it is state-regulated, capped, disclosure-bound, and never allowed on debit — and it generally does not belong on a deductible you want collected without friction; we keep the rules in the surcharge legality and dual-pricing guides. The point is that financing, ACH, and surcharging are real decisions on the self-pay side, not defaults your software flips for you. On the big self-pay ticket, restoration payment processing rewards a deliberate hand.

When the financing offer and the surcharge button live inside whatever software you bill from, they apply the vendor’s partner, rate, and rules — not necessarily the ones that fit your margin or your state. Financing, ACH, and surcharging are all legitimate self-pay levers; the decision should be yours, not a default toggle.

The Carrier Money Is a Cash-Flow Problem, Not a Card Problem

It’s worth being clear about what restoration payment processing can and can’t fix. The largest number on a restoration job — the carrier’s share — arrives as a draft or check, often co-payable to a mortgage lender, after an adjuster signs off on the Xactimate scope, with depreciation held back until the work is documented complete and supplements fought for along the way. That money lands on a long cycle, and whether you collect it through direct billing or an assignment of benefits, it is an accounts-receivable and working-capital question, not a card-processing one. No merchant account changes how fast a carrier pays.

What the card does is narrower and entirely yours to run well: collect the deductible cleanly, ideally on a card on file captured at the work-authorization stage so it isn’t chased after the trucks leave, and handle the betterments and self-pay work with financing where the homeowner needs it. One classification detail is worth a look while you’re at it. A restoration contractor typically codes under MCC 1799, Special Trade Contractors, with the mitigation and cleaning side sometimes coded 7349 — both standard-risk, neither a high-risk fork that freezes accounts. The money is in the rate structure on top of the code, not the code itself — clean restoration contractor payment processing on the deductible and disciplined restoration credit card processing on the self-pay side beat any code tweak, and the same holds for water damage restoration payment processing specifically, where deductible volume is steadiest.

What Actually Lowers a Restoration Company’s Card Cost

The levers that move restoration payment processing are structural, not a tenth of a percent on the swipe. Done right, restoration payment processing prices the deductible and the self-pay job on separate terms instead of one blended average nobody questioned.

- Move to interchange-plus so the deductible and the financed self-pay job are each priced on their true cost — the only model where a small required share and a large uninsured ticket aren’t forced under one number.

- Price the self-pay side deliberately — decide financing, ACH, and surcharging (where compliant) on the uninsured and betterment work yourself, instead of letting your software’s defaults decide.

- Keep the processor shoppable — a restoration merchant account you control rather than one rented from your billing software — so the rate stays your call even though the card stream feels small.

- Capture the deductible at authorization — a card on file taken when the work authorization is signed, so the homeowner’s share is collected up front instead of chased after the claim settles.

Restoration payment processing is a card-stream problem hiding behind a claim. The owner who audits the part the carrier doesn’t pay — the embedded rate, the deductibles, the self-pay financing, and the code underneath — almost always finds more in the part nobody priced than in the one number that never got questioned.

Frequently Asked Questions

Yes — just on a stream you may be overlooking. The carrier’s share arrives by draft or check, so it never touches your rate, but the deductibles, the non-covered betterments, and the fully self-pay jobs run through your terminal all year. Because that volume feels small next to the claim, it’s usually on an unshopped blended rate. Comparing it against an interchange-plus quote is the only way to see what restoration payment processing is actually costing on the part the homeowner pays.

All three are legitimate on the self-pay side. Financing lets a homeowner spread an uninsured remediation or a non-covered balance over monthly payments while you get paid upfront; ACH on a larger out-of-pocket balance turns a card percentage into a flat fee; and surcharging passes the card cost to the customer, though it’s state-regulated, capped, disclosure-bound, never allowed on debit, and usually not worth the friction on a deductible (see our surcharge-legality and dual-pricing guides). Choose deliberately rather than let a default decide.

No. Restoration typically codes under MCC 1799 (Special Trade Contractors), with the mitigation and cleaning side sometimes under 7349 — both standard-risk, not a high-risk fork that freezes accounts. The savings come from pricing the deductible and the self-pay work separately — the way restoration contractor payment processing should be run — not from a special account.

Keep reading on rates, insurance-job payments, and the field-service verticals

Send Your Statement. We’ll Price the Deductible and the Self-Pay Job Apart.

The carrier’s share isn’t your rate’s problem — but the deductibles and the self-pay remediation you run all year are. Send Brookside one recent statement and we’ll break the card stream into an interchange-plus view by card type, show you what the deductibles and uninsured jobs are really costing, and lay out whether financing or ACH fits the self-pay side. The review takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day