Handyman Runs on Small Tickets — Where Flat-Rate Pricing Quietly Costs the Most

Handyman Runs on Small Tickets — Where Flat-Rate Pricing Quietly Costs the Most

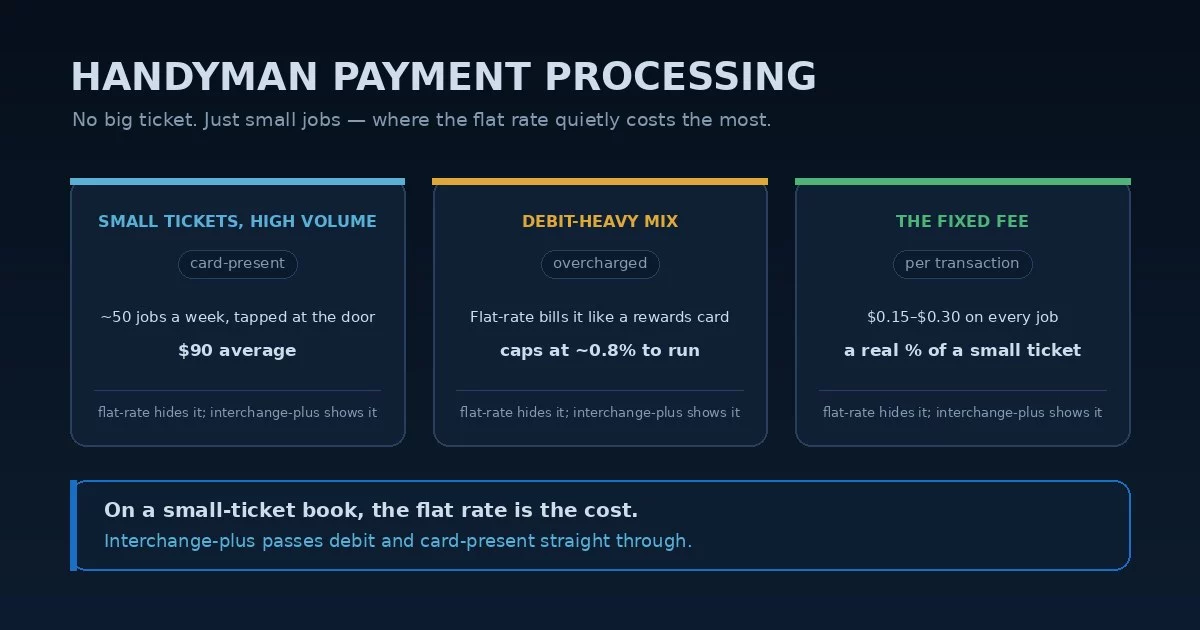

Handyman payment processing is the opposite of every other trade’s problem. There’s no five-figure install to finance and no big percentage to fret over — just a high volume of small jobs, a mounted TV here, a patched wall there, fifty tickets a week between seventy-five and five hundred dollars, most of them tapped on a phone at the door. When every ticket is small, the percentage stops being the thing that hurts. The fixed per-transaction fee and the pricing model do. That’s the half of handyman payment processing nobody quotes: a busy small-ticket shop on the wrong pricing model leaks money on volume, not on any single job.

That single fact reshapes how an owner should think about the setup. Most handymen reach for a flat-rate app — Square, Stripe, PayPal — because it’s simple and there’s no monthly fee, and at low volume that’s a fine call. But as the job count climbs, flat-rate quietly becomes the most expensive option for exactly this profile, and getting handyman payment processing right means knowing when simple has started costing you. For a busy shop, handyman payment processing is won or lost on the pricing model, not the rate on any one job.

You Reached for Square Because It Was Simple

Most handyman payment processing runs on a flat-rate aggregator, and for a good reason: Square, Stripe, and PayPal are simple, predictable, have no monthly fee, and let you tap a card on a phone the day you start. One rate, no statement to read, money in the bank. For a brand-new handyman doing a few jobs a week, that simplicity genuinely outweighs the cost premium.

The cost of that convenience shows up later, and quietly. A flat rate charges one padded percentage on every card no matter what it actually costs to run — and that markup is invisible because there’s no itemized statement to question. Square raised its rates roughly fourteen percent at the start of 2026, and most merchants only noticed when the deposits got smaller. It means your handyman payment processing rate is set by the aggregator and re-set by the aggregator, with no contract markup you agreed to. As with any home services payment processing setup, the simple default is rarely the cheapest one once you have volume, and the only way to know is to put flat-rate next to an interchange-plus quote on your real mix of cards.

Flat-rate pricing bundles the network cost, the assessment, and the processor’s markup into one number you can’t see inside. On a debit-heavy book of small jobs, most of that bundle is markup. Interchange-plus breaks the three apart, so you can finally see how much of every small ticket is the actual card cost and how much is the processor.

Flat-Rate Charges a Debit Card Like It’s a Rewards Card

Here is the structural problem at the center of handyman payment processing, and it’s specific to a shop with lots of small, in-person tickets. Debit-card interchange is capped low by law — often a small fraction of what a rewards credit card costs to run — but flat-rate pricing charges the same padded percentage on both. So when a customer taps a debit card for a ninety-dollar job, a flat-rate processor still bills the full rate and pockets the difference between that and the real, capped debit cost. The more of your work is paid by debit and card-present — which describes most handyman work — the more a flat rate overcharges you.

On interchange-plus, that stops. The low capped-debit cost is passed straight through, the card-present discount is passed through, and you pay the processor only a small fixed markup on top. The savings aren’t dramatic on any one ticket; they’re dramatic across a year of them. For a handyman running real weekly volume, that pass-through is where handyman payment processing stops leaking, and a handyman merchant account priced this way charges a debit tap like the cheap transaction it actually is.

A flat rate optimized for the aggregator’s margin charges roughly the same on a capped-debit tap as on a premium rewards card, even though the debit costs a fraction as much to run. On a small-ticket, debit-heavy book, that gap is the single biggest avoidable cost — and it’s invisible without an itemized statement.

Where Simple Starts Costing You

Flat-rate isn’t wrong — it’s wrong at the wrong volume. Below roughly five to ten thousand dollars a month in card volume, the simplicity of a flat-rate app usually beats the small premium, and handyman payment processing isn’t worth re-engineering. Past that, the math flips, and it flips hardest for a profile like the handyman’s: lots of transactions, card-present, debit-heavy, low average ticket. Each of those is a place flat-rate overcharges and interchange-plus pays back. On that profile, handyman payment processing is almost always cheaper on interchange-plus than on a flat rate.

Two specifics matter at the crossover. The first is the fixed per-transaction fee: a flat fifteen or thirty cents is nothing on a $4,000 job but a real percentage of a $90 one, so a shop full of small tickets pays a hidden surcharge in fixed fees alone. The second is small-ticket interchange — the card networks publish reduced rates for merchants with low average tickets and high transaction counts, and an interchange-plus account can actually reach those where a flat rate never will. Knowing your numbers — average ticket, monthly volume, debit share — is what tells you which side of the crossover you’re on; our effective-rate guide walks through calculating it.

A flat-rate app’s “no monthly fee” pitch hides the trade: you skip a small fixed cost and pay a larger variable one on every card. Once your volume is real, the monthly subscription on an interchange-plus account is usually far less than the markup you’re handing the aggregator — the fee you can see is smaller than the one you can’t.

When Every Job Is Small, How You Take the Card Is the Cost

Because there’s no big ticket to anchor the account, the small disciplines are the whole game in handyman payment processing. Taking the card present — tapped or dipped on a phone reader at the job — is accepted at a meaningfully lower rate, and with less fraud exposure, than the same card keyed in from a text or read over the phone, where aggregators charge their highest rate. For the repeat customers every handyman builds — the “my guy” relationships that are half the business — a card on file turns the next booking into a one-tap charge instead of another keyed entry. And where you take tips, making sure they run on the same card-present footing keeps them from quietly costing more.

One classification detail is worth a look. A handyman business typically codes under MCC 1799, Special Trade Contractors — a standard code, not a high-risk one. Confirming you’re coded for the work you do is a free check, since a miscode can carry the wrong interchange profile. But it’s standard-risk either way; nothing about handyman payment processing freezes accounts the way a true high-risk vertical can. The money is in the pricing model and the card-present discipline on top of the code, not the code itself — clean handyman credit card processing on a tap and a smart handyman merchant account beat any code tweak, and the same logic carries any handyman service payment processing setup.

What Actually Lowers a Handyman’s Card Cost

The levers that move handyman payment processing are structural, not a tenth of a percent on the swipe. Done right, handyman payment processing prices a debit tap as a debit tap instead of bundling it into one padded flat rate.

- Move to interchange-plus once your volume justifies it — past roughly five to ten thousand a month, a debit-heavy small-ticket book almost always beats flat-rate, because the capped-debit and card-present costs finally pass through to you.

- Take the card present — tap or dip on the phone at the door instead of keying it in later, for the lower rate and the lower fraud risk on every job.

- Keep repeat customers on file — a card on file for the “my guy” bookings turns the next job into a one-tap charge at card-present economics.

- Know your debit share — the more of your book is debit and in-person, the more a flat rate is overcharging you, and the more interchange-plus gives back.

Handyman payment processing is a pricing-model problem before it’s a rate problem. The owner who audits the whole book — the flat-rate markup, the debit share, the fixed per-transaction fees, and the code underneath — almost always finds more in the parts that never appear on a flat-rate statement than in the one number that does. Our flat-rate pricing breakdown shows exactly where that markup hides.

Frequently Asked Questions

At low volume, yes — the simplicity and no monthly fee usually outweigh the premium. But Square, Stripe, and PayPal are flat-rate, which charges the same padded percentage on a capped-debit card as on a rewards card. Once a handyman is doing real weekly volume — debit-heavy, card-present, small tickets — that’s exactly the profile where flat-rate overcharges most, and where comparing it to an interchange-plus quote on your real mix tells you what handyman payment processing is actually costing you.

The rough crossover is somewhere around five to ten thousand dollars a month in card volume, and it comes sooner if your mix is heavy on debit and card-present, low-ticket work. The clean way to decide is to calculate your effective rate — total fees divided by total volume — and compare it to an interchange-plus quote. If the gap is more than the small monthly subscription on a real merchant account, the simple app is costing you.

No. Handyman work typically codes under MCC 1799 (Special Trade Contractors), a standard code, not a high-risk one — worth confirming you’re coded for the work you do. It’s standard-risk, so there’s no high-risk fork that freezes accounts. The savings come from the pricing model and taking cards present — the way handyman business payment processing should be run — not from a special account.

Keep reading on pricing models, effective rate, and the field-service verticals

Send Your Statement. We’ll Show You What the Flat Rate Is Really Costing.

If you’re running on Square, Stripe, or PayPal and the job count keeps climbing, send Brookside one recent statement. We’ll calculate your real effective rate, show you how much of your small-ticket, debit-heavy volume is markup, and tell you honestly whether you’ve hit the point where interchange-plus beats the simple app — or whether you’re better off staying put for now. The review takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day