Appliance Repair Gets Paid Twice — the Diagnostic Fee, Then the Repair

Appliance Repair Gets Paid Twice — the Diagnostic Fee, Then the Repair

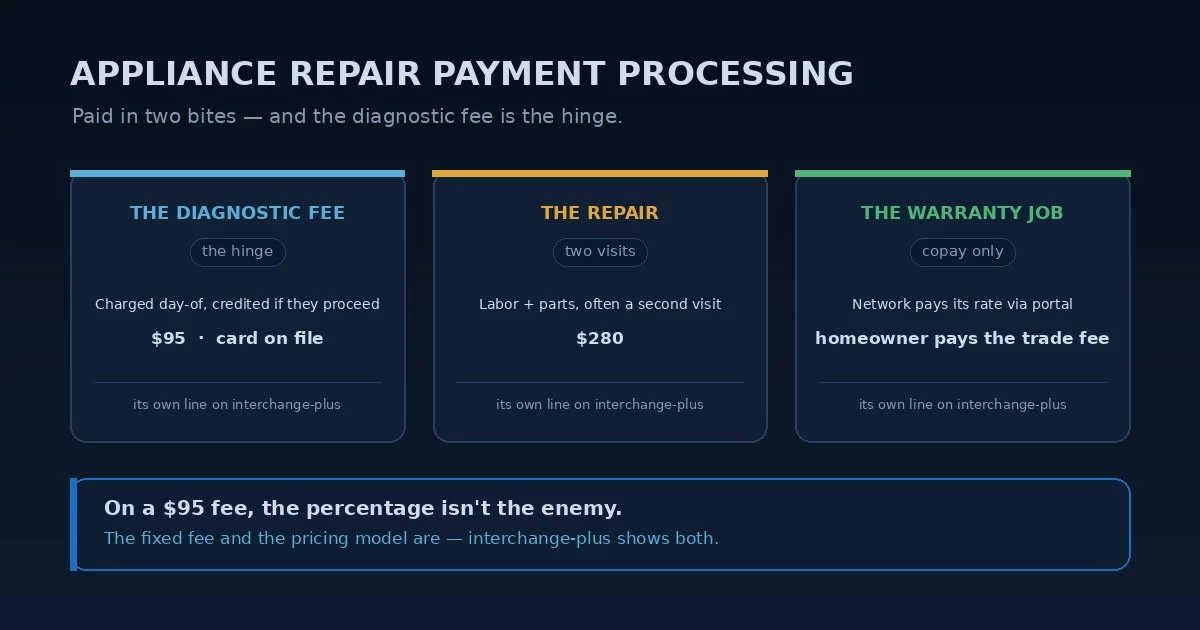

Appliance repair payment processing has a rhythm no other trade shares: you get paid in two bites. First the diagnostic fee — a flat charge to send a tech out and figure out what’s wrong, taken on the day of service — and then, if the customer approves the work, the repair itself, often on a second visit once the part comes in. The diagnostic fee is usually credited toward the repair when the job goes ahead and kept when it doesn’t, which makes it the hinge the whole payment flow turns on. None of that is a big-ticket story; it’s a high-frequency, small-and-mid-ticket one, which is exactly why appliance repair payment processing tends to run on whatever blended rate came bundled with the dispatch software.

That rhythm changes what matters. With a roof or a solar array, the percentage on one giant ticket is everything. With appliance repair, the money leaks across hundreds of small charges a year — diagnostic fees, copays, parts — where the fixed per-transaction fee and the pricing model matter more than the rate. Get appliance repair payment processing wrong and a rate that looks fine on a single $95 service call is quietly expensive across a year of them.

Your Dispatch Software Usually Picks Your Processor

Most appliance repair payment processing decisions get made by accident. Almost every shop runs a field-service platform — Workiz, Housecall Pro, Service Fusion, ServiceTitan — and most ship with an integrated payments product that bundles card processing right into the app, alongside the parts inventory and the warranty tracking. The convenience is real: the diagnostic fee, the parts order, the repair invoice, and the follow-up all live in one place, and the tech swipes a card in the driveway.

The cost of that convenience is leverage. When the processor comes attached to the software, the rate is usually a single blended number, padded and unexamined, and a high-frequency book of small tickets is the worst place to leave a blended rate unquestioned. It means your appliance repair payment processing rate was set by whoever your software vendor partnered with, not by you. As with any home services payment processing setup, the bundled processor is rarely the one you’d have chosen, and the only way to know whether the rate is fair is to put it next to an interchange-plus quote on your real volume.

On a high-frequency book of $95 diagnostic fees and $250 repairs, the fixed per-transaction fee and the padded percentage on debit cards add up fast — and a flat blended rate hides both. Interchange-plus breaks out the network cost and the processor’s markup so you can see what each small ticket actually costs instead of trusting one padded number. On a book this size, appliance repair payment processing lives or dies on the per-transaction structure.

The Charge You Take First and Sometimes Give Back

The diagnostic fee is the part of appliance repair payment processing with no equivalent elsewhere. You charge it to roll a truck and diagnose the appliance, and then its fate depends on the customer’s decision: credited toward the repair if they approve the work, kept if they decline. That conditional life has two consequences for how you take the money. First, it’s worth pre-collecting — a card on file captured when the appointment is booked turns a no-show into a covered visit instead of a wasted truck roll, the single biggest revenue leak in the trade. Second, because the fee is often credited or refunded into the larger repair charge, you want a processor whose pricing doesn’t punish you twice — a fixed fee on the diagnostic charge and again on the refund or adjustment.

Taking that fee card-present, tapped or dipped at the door rather than keyed over the phone, earns a better rate and lower fraud exposure on every visit — and across a full schedule of diagnostic calls, that gap is real money. The diagnostic fee is small, but it’s the most frequent transaction you run, so it’s the one where the structure of appliance repair payment processing matters most.

A blended rate optimized for a mid-size repair is quietly expensive on a $95 diagnostic fee — and when that fee is later credited into the repair, a poorly structured account can ding you on the adjustment too. High frequency turns a few cents and a padded percentage into a meaningful annual number. It’s the clearest place appliance repair payment processing leaks.

The Second Visit, and the Part You Float

When the customer approves the work, appliance repair payment processing moves to its second bite: labor plus parts, frequently on a return visit after the part is ordered in. You float the cost of that part between visits, and the repair charge — usually a few hundred dollars — is where the percentage starts to matter more than the fixed fee. Keeping the customer’s card on file from the diagnostic visit makes the second charge a one-tap close instead of a chase, and it ties the credited diagnostic fee cleanly into the final repair total.

One classification detail is worth a look. An appliance repair business usually codes under MCC 7623, Refrigeration and Air-Conditioning Repair, or 7629, Electrical and Small Appliance Repair — the repair-services family, not the special-trade contractor codes the building trades use, and shops that also sell parts or units may carry 5722 on a second account. All standard-to-moderate risk; none is a high-risk fork. Confirming you’re coded as the repair business you are is a free check, since a miscode can carry the wrong interchange profile. The money is in the rate structure and the card-present discipline on top of the code — clean appliance repair credit card processing on the diagnostic and repair charges beats any code tweak. On a high-frequency book, appliance repair payment processing rewards the structure, not the code.

The diagnostic visit and the parts-install visit are one job paid in two steps. A card on file from the first visit lets you credit the diagnostic fee, charge the repair, and close on the second visit without re-keying — better rate, less friction, fewer uncollected balances.

When the Network Pays the Repair and the Card Only Sees the Copay

A large share of appliance repair runs through home-warranty networks — American Home Shield, HWA, Fidelity National, and the rest — and that flips the payment picture. On a warranty job the homeowner pays only the trade-call fee, often their single out-of-pocket cost, while the warranty company pays the approved repair on its own rate through its portal, typically by direct deposit within a week or two. Manufacturer warranty work runs differently again: sometimes the homeowner pays you directly and the manufacturer reimburses them. Either way, the card in your terminal mostly sees the homeowner’s small share, not the covered repair. That split reshapes appliance repair payment processing more than any single rate line.

That’s worth being honest about: appliance repair business payment processing can’t change what a warranty network pays you, any more than a merchant account changes an insurer’s check. What it can do is make sure the homeowner-paid side — the trade-call fees, the retail out-of-warranty repairs, the upsells the network doesn’t cover — is priced on what it actually costs. For shops running a mix of network and retail work, the retail card stream is usually where the margin and the mispricing both live, which is exactly where appliance repair service payment processing earns its keep.

What Actually Lowers an Appliance Repair Shop’s Card Cost

The levers that move appliance repair payment processing are structural, not a tenth of a percent on the swipe. Done right, appliance repair payment processing prices the high-frequency diagnostic fees and the retail repairs on their true cost instead of one padded blended rate.

- Move to interchange-plus so the diagnostic fee, the repair, and the copay are each priced on true cost — the only model that doesn’t bury the fixed per-transaction fee that bites hardest on small, frequent tickets.

- Pre-collect the diagnostic fee — a card on file at booking cuts no-shows and carries cleanly across the two visits, crediting into the repair without re-keying.

- Take every charge card-present — tapped or dipped at the door instead of keyed over the phone, for the better rate and lower fraud risk on a high-volume schedule.

- Price the retail side, not the network rate — focus the account on the homeowner-paid trade-call fees and out-of-warranty repairs, where your margin and any mispricing actually sit.

Appliance repair payment processing is a high-frequency, small-ticket problem before it’s a rate problem. The owner who audits the whole book — the blended markup, the fixed fees on diagnostic charges, the refund handling, and the retail-versus-warranty mix — almost always finds more in the parts that never appear on a flat statement than in the one number that does.

Frequently Asked Questions

Not necessarily. A bundled processor in Workiz, Housecall Pro, or ServiceTitan is built for convenience and usually priced on a blended rate that averages your card types together. On a high-frequency book of small diagnostic fees and mid-size repairs — the worst place to leave a padded rate unexamined — the only way to know is to compare it against an interchange-plus quote on your real volume.

Pre-collect it with a card on file when the appointment is booked — that turns a no-show into a covered visit and keeps the card available for the repair. When the customer approves the work, credit the fee into the repair total on the same card rather than refunding and re-charging, so you’re not paying fixed transaction fees twice. Card-present capture at the door beats keying it in for both rate and fraud risk. Handled this way, appliance repair payment processing stops leaking on the most frequent charge you run.

No. Appliance repair usually codes under MCC 7623 (Refrigeration and A/C Repair) or 7629 (Electrical and Small Appliance Repair) — the repair-services family — with 5722 sometimes used if you also sell parts or units. All standard-to-moderate risk, no high-risk fork. The savings come from pricing the high-frequency small tickets correctly and taking cards present — the way appliance repair merchant account economics actually work — not from a special account.

Keep reading on pricing models, small-ticket economics, and the field-service verticals

Send Your Statement. We’ll Price the Diagnostic Fee and the Repair Right.

If your processor came bundled with Workiz, Housecall Pro, or another dispatch platform, send Brookside one recent statement. We’ll break it into an interchange-plus view by card type, show you what the high-frequency diagnostic fees and the retail repairs are really costing once the fixed fees are counted, and flag whether your setup handles the diagnostic-fee credit cleanly. The review takes about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day