In Tree Service, the Big Removal Belongs on a Bank Transfer — Not a Card

In Tree Service, the Big Removal Belongs on a Bank Transfer — Not a Card

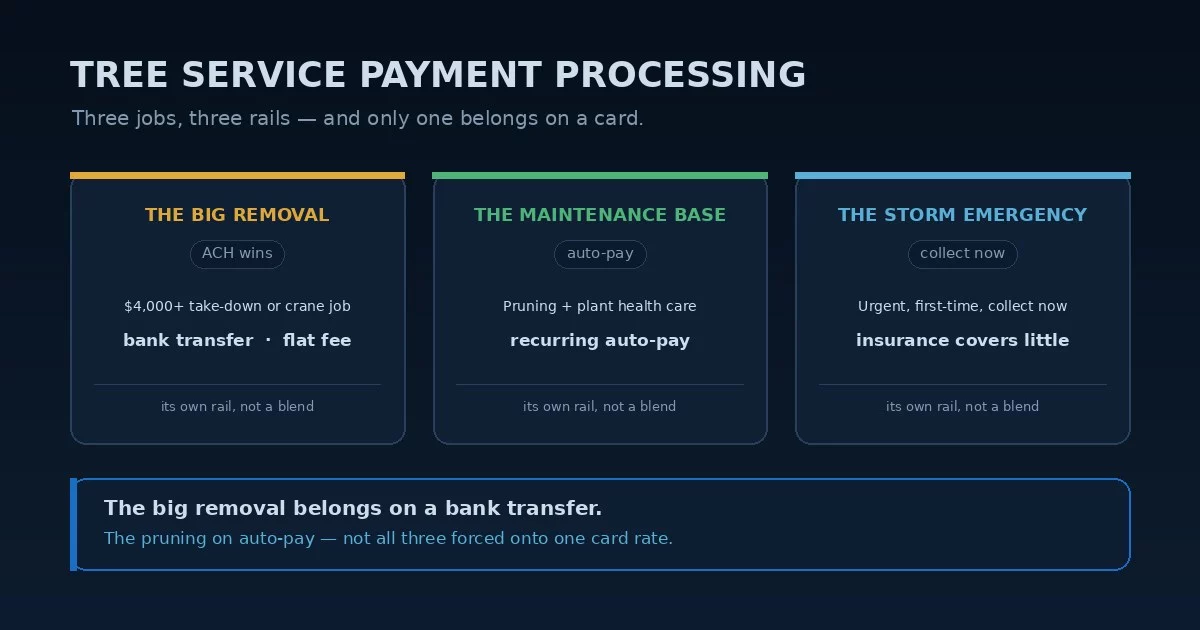

Tree service payment processing collects three different ways, and only one of them really belongs on a credit card. There’s the big removal — a large, infrequent ticket, often a few thousand dollars and sometimes well into five figures for a crane job — where a card’s percentage is brutal and a bank transfer or a financing plan fits far better. There’s the maintenance base — recurring pruning, plant-health-care treatments, and seasonal programs that want auto-pay, not a fresh swipe every visit. And there’s the storm emergency — urgent, often a first-time customer, collected on the spot. A single blended card rate is built for none of those, which is exactly why tree service payment processing tends to run on whatever came bundled with the software.

That mix changes what matters. The whole tree-care industry has quietly moved toward bank transfers for a reason: a flat fee on a $4,000 removal beats a card percentage by hundreds of dollars, every job. Get tree service payment processing wrong and you hand a processor a few hundred dollars on every large removal you run, on top of overpaying the recurring work. Get it right and each of the three streams is on the rail that actually fits it.

Your Tree-Care Software Usually Picks Your Processor

Most tree service payment processing decisions get made by accident. Almost every operator runs a tree-care platform — Arborgold, SingleOps, Jobber — and most ship with an integrated payments product that bundles card processing right into the estimate-to-invoice flow. The convenience is real: the quote, the deposit, the removal invoice, and the recurring pruning plan all reconcile in one place, and the crew collects from the field.

The cost of that convenience is leverage, and in tree care it’s expensive in a specific way. When the processor comes attached to the software, every payment defaults to a card at a single blended rate — including a $4,000 removal that never should have touched a card at all. It means your tree service payment processing rate, and your default payment rail, were set by whoever your software vendor partnered with, not by you. As with any home services payment processing setup, the bundled default is rarely the cheapest path, and the only way to know is to put it next to an interchange-plus quote — and a bank-transfer option — on your real mix of removals and maintenance.

A blended rate charges the same padded percentage on a $90 pruning visit and a $4,000 removal. On the removal, that percentage is real money a flat bank transfer would have avoided. Interchange-plus and an ACH option break the cost apart so the big removal stops paying card economics it never needed. It’s the clearest place tree service payment processing leaks.

Where the Percentage Bites — and the Bank Transfer Wins

The removal is where tree service payment processing leaks the most, because it’s the largest and least frequent ticket. A few points on a $4,000 take-down — or a $9,000 crane job — is real money, every time, and unlike a small pruning charge there’s no fixed-fee tradeoff to muddy the math: on a big ticket, the percentage is the whole cost. This is why tree care has leaned into ACH bank transfer harder than almost any trade. A bank transfer runs at a flat fee regardless of the amount, so on a five-figure removal it can beat a card by an order of magnitude, and the savings show up on every large job.

Two more levers belong on the removal. A deposit up front — standard on crane-assisted and hazardous work, where you’re committing equipment and permits before the first cut — keeps you from floating the job, and a card on file carries the balance to completion. And for a homeowner who can’t pay a large removal at once, financing lets them spread it while you’re paid upfront. Surcharging is a further option on the card portion, though it’s state-regulated, capped, disclosure-bound, and never allowed on debit; we keep those rules in the surcharge legality guide. The point is that the big removal deserves a deliberate rail and a deposit, not a default swipe — on the large ticket, tree service payment processing rewards a deliberate hand.

Running a $9,000 crane removal through a bundled card processor at a blended rate can hand over two or three hundred dollars that a flat-fee bank transfer would have saved — on the single job where the percentage hurts most and a fixed fee fixes it.

Pruning and Plant Health Care Want Auto-Pay

Underneath the removals is the steady floor of a tree-care business: recurring pruning, plant-health-care treatments, and seasonal programs that repeat on a schedule. That part of tree service payment processing wants a different setup entirely — recurring auto-pay on a card or bank account on file, billed automatically each cycle, so you’re not re-collecting from the same customer every visit and not chasing renewals. Recurring bank-transfer auto-pay is the cheapest version of this, and it’s why a tree service merchant account built for the work pairs one-off removal billing with a recurring engine for the maintenance base.

The basics there are worth getting right: a card or account on file captured when the plan starts, clean recurring billing on whatever cycle you sell, and failed-payment handling so an expired card doesn’t silently drop a maintenance customer and the renewal revenue with it. It’s the unglamorous half of tree care payment processing, and it’s the half that smooths the cash flow between storm seasons.

Re-swiping a maintenance customer every visit wastes the rate and risks the renewal. Recurring auto-pay — ideally by bank transfer — on a plan set up once keeps the maintenance base steady and cheap, and lets you focus the card terminal on the work that actually needs it. That split is where tree service payment processing gets cheaper.

The Emergency — and the Insurance Most Homeowners Assume They Have

Storm season is when tree service payment processing gets tested. Demand spikes overnight, the customer is usually new with no card on file, and the work has to be collected on the spot — a pattern where a card tapped at the site beats one keyed in over the phone on both rate and fraud risk, and where having repeat customers already set up on bank transfer lets you start work without chasing a payment method. There’s also an expectation to manage: many homeowners assume their insurance will cover storm tree removal, when in practice a homeowner’s policy generally pays only when the tree strikes a covered structure, often with a low per-tree cap. The contractor usually collects the bulk from the homeowner regardless, so letting “insurance will get it” stall the conversation just delays your own payment.

One classification detail is worth a look. A tree service usually codes under MCC 0780, Landscaping and Horticultural Services — the same family as landscaping, not a special-trade contractor code — a standard-risk classification. Confirming you’re coded as the tree-care business you are is a free check, since a miscode can carry the wrong interchange profile. The money is in the rail and the rate structure on top of the code — clean tree service credit card processing on the storm work and disciplined arborist payment processing across removals and maintenance beat any code tweak. On a storm-driven book, tree service payment processing rewards the rail discipline, not the code.

What Actually Lowers a Tree Company’s Card Cost

The levers that move tree service payment processing are structural, not a tenth of a percent on the swipe. Done right, tree service payment processing puts each of the three streams on the rail that fits it instead of forcing all of them onto one blended card rate.

- Put the big removal on a bank transfer — a flat-fee ACH payment on a four- or five-figure removal beats a card percentage by hundreds, with a deposit up front on crane and hazardous work.

- Run the maintenance base on recurring auto-pay — pruning, plant-health-care, and seasonal plans on a card or account on file, ideally by bank transfer, so the recurring floor stays steady and cheap.

- Set storm repeat customers up before the storm — a card or bank account on file, captured card-present, so you can start emergency work without chasing payment in the chaos.

- Move whatever card volume remains to interchange-plus so the deposits and one-off charges are priced on true cost, not a padded blend.

Tree service payment processing is a three-rail problem before it’s a rate problem. The owner who audits the whole book — the removals that should be bank transfers, the maintenance that should be auto-pay, the storm work, and the code underneath — almost always finds more in the rails nobody chose deliberately than in the one card rate that gets all the attention.

Frequently Asked Questions

A bank transfer, almost always. ACH runs at a flat fee regardless of amount, so on a $4,000 removal — let alone a five-figure crane job — it beats a card’s percentage by hundreds of dollars. Card has its place for deposits and smaller balances, but the full removal is a bank-transfer job. Pairing that with a deposit up front on hazardous work is where tree service payment processing saves the most.

Usually far less than the homeowner expects. A homeowner’s policy generally pays for tree removal only when the tree strikes a covered structure — a house, a fence, a shed — and often caps what it pays per tree. A tree that simply falls in the yard is frequently not covered at all. In practice you collect the bulk from the homeowner, so it’s worth setting payment expectations up front rather than letting an assumed insurance claim delay collection.

No. Tree service usually codes under MCC 0780 (Landscaping and Horticultural Services), the same standard-risk family as landscaping — no high-risk fork. The savings come from putting removals on bank transfer, maintenance on recurring auto-pay, and whatever card volume remains on interchange-plus — the way tree service merchant account economics actually work — not from a special account.

Keep reading on payment rails, seasonality, and the field-service verticals

Send Your Statement. We’ll Get the Removal on the Right Rail.

If your processor came bundled with Arborgold, SingleOps, or another tree-care platform, send Brookside one recent statement. We’ll break it into an interchange-plus view, show you how much your big removals are losing to card percentages that a bank transfer would save, and set up recurring auto-pay for the maintenance base. The review takes about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day