In Moving, the Deposit Is the Easy Part — the Balance and the Chargebacks Aren’t

In Moving, the Deposit Is the Easy Part — the Balance and the Chargebacks Aren’t

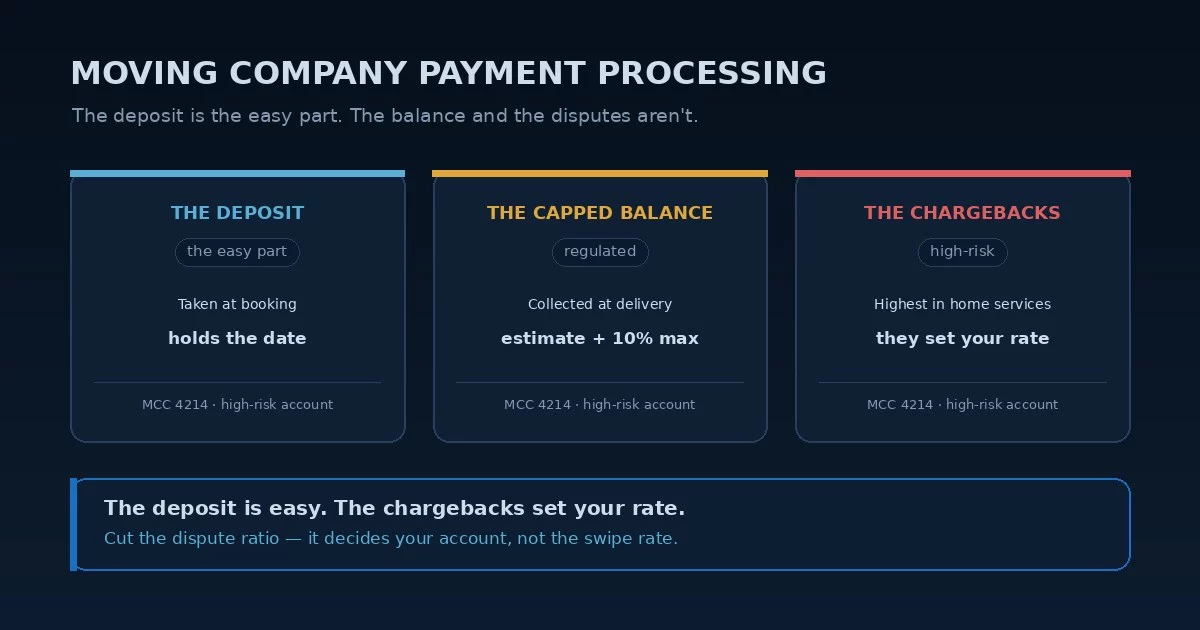

Moving company payment processing is paid in two parts — a deposit at booking and a balance at delivery — but two things set it apart from every other field-service trade. First, a federal rule caps what you can collect at the truck: on a non-binding interstate estimate, a mover can’t require more than a hundred and ten percent of the estimate at delivery, so the amount you charge at the end isn’t fully yours to set. Second, moving carries one of the highest chargeback rates in all of home services — damaged-goods claims, delay disputes, “they charged more than the quote” — and that single fact lands most movers in a high-risk merchant account. The deposit is the easy part; the capped balance and the disputes are where moving company payment processing actually lives.

That changes the whole problem. For a plumber or an electrician the account is a commodity and the only question is the rate. For a mover, the question is first whether you can get a stable account at all, and then how to keep the chargebacks that set your rate from piling up. Get moving company payment processing wrong and you’re not overpaying by a few points — you’re risking a frozen account in peak season.

Movers Don’t Just Inherit a Rate — They Inherit Whoever Will Take Them

Most field-service businesses back into a processor bundled with their software. Moving company payment processing has a harsher version of the same trap: because the industry is classified high-risk, a lot of movers end up on whatever processor was willing to approve them, at whatever rate and reserve that processor set, and they stay there because re-applying feels risky. The moving CRM — SmartMoving, Supermove, MoveitPro, Elromco — bundles a payments option, and the path of least resistance is to take it and never look again.

The cost of that is steep in two directions. The rate is rarely shopped, because the owner assumes high-risk means take-what-you-get — and the reserve terms, which matter more than the rate for a mover, are usually never negotiated at all. It means your moving company payment processing terms were set by the first processor that said yes, not by you. As with any home services payment processing setup the bundled default is rarely the best one, but for a mover the stakes are higher: the wrong account doesn’t just cost margin, it can hold your funds.

High-risk classification narrows your options, but it doesn’t erase them. Processors that genuinely underwrite movers compete on rate, reserve percentage, and rolling-reserve release terms — and those terms vary widely. Treating the first approval as the only option is how movers end up overpaying on a rate and over-reserved on cash flow at the same time. It’s the costliest default in moving company payment processing.

What the Binding Estimate Lets You Collect

The structure of moving company payment processing is shaped by the estimate before a card is ever run. A deposit at booking holds the date and covers your commitment, but it comes with refund obligations a mover has to honor, and a deposit taken weeks before the move is exactly the kind of charge a customer later disputes. The balance at delivery is governed by the estimate type: a binding estimate fixes the price, while a non-binding estimate is settled on actual weight or hours — but under the federal hundred-and-ten-percent rule, on an interstate non-binding move you can only require the estimate plus ten percent at delivery, with anything above that billed later. The old cash-on-delivery norm has given way to cards and bank transfers, which is better for the customer and for your records, but it also moves the balance onto rails where disputes are possible.

That’s the practical heart of it: the deposit and the balance are two different charges with two different risk profiles, and on a large interstate move the balance is big enough that a bank transfer often beats a card percentage outright. A mover payment processing setup that handles a clean deposit, a compliant capped balance, and an ACH option for the big jobs is doing the real work — not the swipe rate alone.

A deposit charged at booking, for a move that then goes sideways, is a classic chargeback. Without a signed estimate, a clear cancellation policy, and a record of authorization on file, that dispute is one you lose — and every lost dispute pushes your chargeback ratio toward the threshold that gets an account shut down.

The Disputes Are What Set Your Rate

For most trades, chargebacks are a footnote. For movers they’re the main event, and they’re why moving company payment processing is priced and underwritten the way it is. A mover handles a customer’s entire material life, under deadline, often after a price that grew between the quote and the truck — fertile ground for damaged-goods claims, delay complaints, and “I never agreed to that amount” disputes. A high chargeback ratio doesn’t just cost you the disputed jobs; it raises your rate, grows your reserve, and at the extreme ends your account. So the most valuable thing a mover can do for moving company payment processing isn’t shaving the rate — it’s cutting the dispute rate.

That’s concrete work: a signed binding or capped estimate the customer can’t later claim they didn’t agree to, card-present capture or a documented authorization on the deposit, condition photos and signed delivery receipts, and the dispute-evidence discipline covered in the compelling evidence standards that let you actually win the disputes you do get. Every chargeback you prevent or win protects the rate and the account, which is why dispute control is the center of moving company credit card processing, not a side issue.

For a mover, the chargeback ratio is the number that sets the price. Signed estimates, authorized deposits, delivery documentation, and clean dispute evidence aren’t just customer-service hygiene — they’re the most direct lever you have on what your account costs and whether you keep it. That makes dispute control the heart of moving company payment processing.

Moving Is a Trade Where the Account Itself Is the Decision

Most field-service trades can treat the merchant account as a commodity. Moving can’t, and that’s the defining fact of moving company payment processing. A moving company codes under MCC 4214, Motor Freight Carriers and Movers — a transportation code that, combined with deposits taken before delivery and the industry’s dispute history, puts most movers in the high-risk bucket. That isn’t a verdict on your business; it’s a category, and the answer to it is a processor that actually underwrites movers rather than a generic high-risk processor that will approve anyone and price for the worst. That choice is where moving company payment processing is won or lost.

What you’re shopping for is different from what a standard trade shops for. The headline rate matters, but the reserve percentage, the rolling-reserve release schedule, and the processor’s tolerance for your deposit-and-balance pattern matter more, because those decide your cash flow and whether your funds are available when payroll is due. A moving company high-risk merchant account chosen deliberately — underwritten by someone who understands the trade — is worth far more than a tenth of a percent on the swipe. This is the one vertical where the account is the decision, not a default.

What Actually Stabilizes a Mover’s Payments

The levers that move moving company payment processing are structural, not a tenth of a percent on the swipe. Done right, moving company payment processing pairs a stable, properly underwritten account with the dispute discipline that keeps it stable.

- Get an account underwritten for movers — a processor that knows the trade and competes on reserve terms, not a generic high-risk approval that prices for the worst and freezes funds when volume spikes.

- Cut the chargeback ratio — signed binding or capped estimates, authorized deposits, condition photos, and signed delivery receipts, because the dispute rate is what sets your price and your survival.

- Structure the deposit and balance cleanly — a documented deposit at booking and a compliant balance at delivery, so neither becomes the dispute that pushes your ratio over the line.

- Put the big interstate balance on a bank transfer — a flat-fee ACH payment beats a card percentage on a large long-distance move, and a bank transfer is harder to charge back than a card.

Moving company payment processing is an account-stability and dispute problem before it’s a rate problem. The owner who fixes the reserve terms and the chargeback ratio almost always gains more — in available cash and an account that doesn’t freeze in peak season — than any rate cut alone could deliver.

Frequently Asked Questions

Two reasons stack up. Movers take deposits weeks before delivering the service, and the industry has one of the highest chargeback rates in home services — damaged-goods claims, delay disputes, and price disagreements between the quote and the final bill. Combined with the MCC 4214 transportation code, that puts most movers in the high-risk category. It’s a classification, not a judgment, and the right answer is a processor that underwrites movers specifically.

On an interstate non-binding estimate, the federal rule limits what you can require at delivery to a hundred and ten percent of the estimate; charges above that are billed afterward rather than collected at the truck. A binding estimate fixes the price instead. The takeaway for moving company payment processing is that the balance you collect at delivery is shaped by the estimate type, so your deposit-and-balance structure has to match the estimate you gave.

Cutting the chargeback ratio. For a mover the dispute rate sets the price and decides whether the account survives, so signed estimates, authorized deposits, delivery documentation, and clean dispute evidence move the cost more than rate-shopping alone. Beyond that, a properly underwritten moving company merchant account with fair reserve terms and ACH for big interstate balances does more than chasing a lower swipe rate.

Keep reading on high-risk accounts, chargebacks, and payment rails

Send Your Statement. We’ll Look at the Rate and the Reserve.

Movers get approved once and stay put — usually overpaying on the rate and over-reserved on cash flow. Send Brookside one recent statement and we’ll show you what the rate and the reserve terms actually compare to among processors that underwrite movers, where your chargeback exposure is costing you, and whether ACH on big interstate balances would help. The review takes about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day