Tattoo Shop Payment Processing: You’re Not High-Risk

A Licensed Studio Is Legitimate — Your Processor May Not Treat It That Way

A licensed tattoo or piercing studio is a real, regulated business — health-inspected, permitted, often more compliant than the coffee shop next door. Yet the way it gets paid is a minefield. Sign up with an instant-approval processor like Square, Stripe, or PayPal and you can be accepting cards in minutes — and frozen out just as fast, weeks later, when an automated system decides a licensed body-art business is “high-risk,” or flags a volume spike, or sees a disputed deposit. That mismatch — a legitimate shop treated as a liability — is the whole story of tattoo shop payment processing.

It cuts the other way too: some processors slap a blanket “high-risk” label on a clean, licensed studio and charge high-risk rates and rolling reserves it doesn’t deserve. Between the aggregators that freeze without warning and the processors that overcharge on reputation alone, a tattoo shop can lose access to its own money or quietly overpay for years. Good tattoo shop payment processing starts by refusing both traps: get classified correctly, and get an account that actually stays open.

Instant Approval, Instant Freeze — the Aggregator Trap

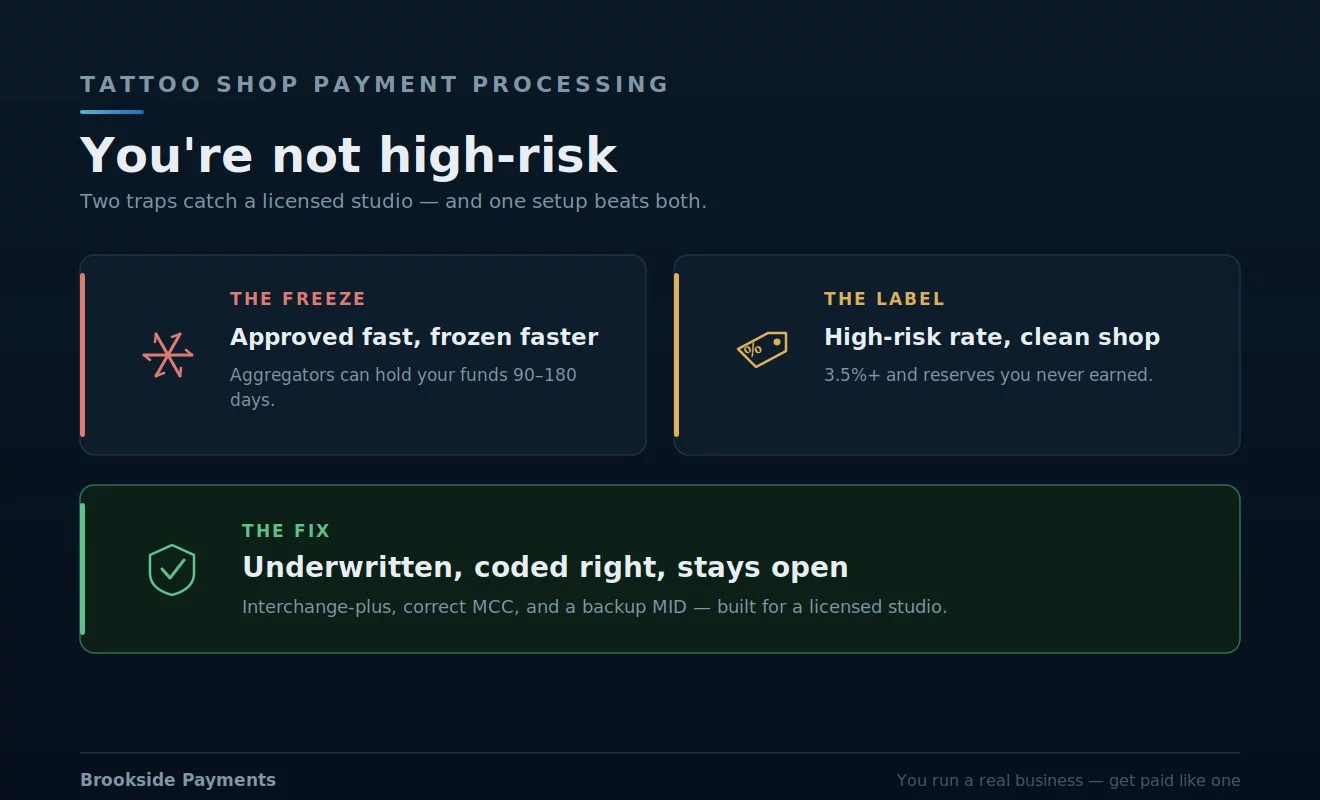

Square, Stripe, and PayPal approve you in minutes because they don’t really underwrite you up front — they let you start processing, then review your business afterward. For a tattoo shop, “review later” is a landmine: these platforms are known to flag businesses that require licensing, to treat a busy month or a few disputed deposits as fraud signals, and to freeze the account or hold funds for 90 to 180 days with no warning and little recourse. A studio mid-booking-season can suddenly find a month of revenue locked up. This is the single biggest risk in tattoo shop payment processing, and it has nothing to do with whether your shop did anything wrong.

The defense in tattoo shop payment processing is structural, not hopeful. A real, underwritten merchant account — where an acquiring bank reviews your licensed body-art business and assigns your own Merchant ID before you process a dollar — stays open precisely because the risk was assessed up front, not flagged after the fact. Serious shops run a backup MID as well, so a freeze on one account never stops the chairs. A proper tattoo merchant account trades five minutes of instant approval for the thing that actually matters: an account that doesn’t vanish in your busiest week.

In tattoo shop payment processing, aggregators (Square, Stripe, PayPal) approve fast but underwrite later — then freeze or close licensed body-art shops on a licensing flag, a volume spike, or a disputed deposit, holding funds 90–180 days. A real underwritten merchant account assesses your shop up front and stays open. Run a backup MID so one freeze never stops the chairs.

You’re Probably Not High-Risk — Don’t Pay Like You Are

The flip side of the freeze is the overcharge. Some processors lump every tattoo and piercing shop into a blanket “high-risk” bucket — rates of 3.5% and up, rolling reserves, extra fees — citing the personal-services nature, tip-heavy tickets, and “perceived” chargeback risk. For a licensed studio with a clean chargeback history, that classification is usually outdated and unnecessary. A legitimate shop coded correctly under its proper merchant category (MCC 7299) should price like the standard service business it is, not like an adult or gambling account. Accepting a high-risk label you didn’t earn is one of the most expensive mistakes in tattoo and piercing payment processing.

The move is to ask directly. Before you sign, ask any processor explicitly whether they classify tattoo shops or MCC 7299 as high-risk, and what rate and reserve that triggers. A clean, licensed studio doing normal volume should land on transparent interchange-plus pricing — typically a 1.6% to 2.1% effective rate on total card volume including tips — not a high-risk tattoo merchant account with a 3.5% floor and a chunk of every sale held in reserve. In tattoo shop payment processing, if a processor insists you’re high-risk with no chargeback problem to point to, that’s a reason to walk, not a fact to accept.

In tattoo shop payment processing, a clean, licensed studio is usually not high-risk. Ask any processor explicitly whether they treat tattoo shops or MCC 7299 as high-risk, and what rate/reserve it triggers. Coded correctly, you should land on interchange-plus (~1.6–2.1% effective, tips included), not a 3.5%+ high-risk rate with rolling reserves. No chargeback problem to point to means no reason to accept the label.

No-Show Deposits, Per-Artist Payouts, and Tips on Everything

Beyond the classification fight, a tattoo shop has real operational payment needs. No-shows are brutal — a missed four-hour custom session can cost an artist $400 to $1,000 in lost time — so deposits taken at booking are standard practice. But deposits create their own exposure: a client who no-shows and then disputes the deposit charge hands you a chargeback, which is exactly the kind of mark that gets an aggregator to freeze you. Handling deposits well — clear policy, card-on-file, the deposit applied to the final bill — is core to tattoo shop payment processing, not an afterthought.

Then there’s the shop’s structure. Many studios run on a booth- or chair-rental model where artists are effectively independent operators, which means your setup has to tag every transaction to the artist who did the work and produce clean per-artist reports — gross, fees, tips, and net payable — at month-end. Tips ride on top of nearly every ticket and, handled poorly, cause tip-adjustment downgrades. A tattoo studio credit card processing setup that gets deposits, per-artist reporting, and tips right is the part of tattoo shop payment processing that turns payday and bookkeeping from a monthly headache into a non-event.

Deposits protect against costly no-shows but can boomerang as chargebacks if disputed — use a clear policy, card-on-file, and apply the deposit to the final bill. Booth/chair-rental shops need every charge tagged to the artist for clean per-artist payout reports (gross, fees, tips, net). And handle tips so gratuity added after service doesn’t cause adjustment downgrades.

Get Classified Right, Stay Open, Price It Fairly

Put together, the fix for a tattoo or piercing studio is straightforward: a real, underwritten merchant account that codes your licensed shop under the correct category and stays open instead of freezing, transparent interchange-plus pricing instead of an undeserved high-risk rate, and clean handling of the deposits, per-artist payouts, and tips your shop runs on. Online deposits collected through a virtual terminal or payment link process at card-not-present interchange rates — cheaper than the flat 2.9% an aggregator charges — and a backup MID keeps you running if anything ever goes sideways. That’s the difference between tattoo shop payment processing that fights you and a setup that simply works.

A real underwritten merchant account (correct MCC, stays open), interchange-plus instead of a high-risk rate, online deposits at CNP interchange rates rather than a flat 2.9%, clean per-artist and tip handling, and a backup MID. That combination ends both traps — the surprise freeze and the undeserved high-risk markup — at once.

Stop Being Treated Like a Risk You’re Not

A licensed tattoo or piercing studio loses money two ways: to the aggregator that freezes a month of revenue without warning, and to the processor that charges high-risk rates on a clean, legitimate shop. Tattoo shop payment processing done well closes both — a properly underwritten account coded under the right category, interchange-plus pricing you can actually see, deposits and per-artist payouts and tips handled cleanly, and a backup account so a freeze never stops the chairs. You run a real, regulated business. Get paid like one.

Frequently Asked Questions

Mostly out of habit, not fact. Some processors bucket all tattoo and piercing shops as “high-risk” citing the personal-services nature, tip-heavy tickets, and perceived chargeback risk — and aggregators like Square avoid businesses that require licensing. But a licensed studio with a clean chargeback history, coded correctly under MCC 7299, usually doesn’t warrant high-risk rates or reserves. These classification questions are where tattoo shop payment processing starts: ask any processor explicitly how they classify tattoo shops before you sign.

Yes, and it’s a known pattern in tattoo shop payment processing. These aggregators approve instantly but underwrite afterward, so a licensing flag, a sudden volume spike, or a disputed no-show deposit can trigger a freeze or closure with funds held 90 to 180 days and little recourse. The defense is a real, underwritten merchant account that assesses your business up front and stays open — plus a backup MID so one freeze never stops you from taking payment.

Take a deposit at booking with a clear, disclosed policy and a card on file, and apply the deposit to the final bill. That protects against no-shows that can cost an artist hundreds in lost time. The catch is disputes: a client who no-shows and challenges the deposit creates a chargeback, so keep your policy documented and your records clean — and route deposits through an account that won’t freeze you over a normal dispute.

Keep reading on high-risk labels, holds, and disputes

Get a Read on Your Studio’s Processing

Send Brookside one recent statement and we’ll show your real effective rate, whether you’re being charged high-risk pricing you don’t need, and whether your current setup could freeze your funds at the worst time. We’ll show what tattoo shop payment processing looks like done right for a licensed studio — a properly classified, interchange-plus account with deposits, per-artist payouts, and tips included. You can also review card payment protections from the CFPB.

Get Your Studio ReviewedNo obligation • No pressure • Response within one business day