Why Smoke Shop Payment Processing Breaks on Stripe, Square, and PayPal

Why Smoke Shop Payment Processing Breaks on Stripe, Square, and PayPal

Smoke shop payment processing almost always starts the same way: a new shop signs up for Stripe, Square, or PayPal in a few minutes, runs sales for weeks, and assumes payments are handled. Then one morning the account is frozen, the funds are held, and there is no one to call. It is not bad luck. Those platforms are aggregators — they run thousands of businesses under one master merchant account and approve signups with automated rules. Their acceptable-use policies explicitly prohibit tobacco, vape, and nicotine products, and their systems flag the category the moment they recognize it.

What makes aggregators effortless for a gift shop is exactly what makes them dangerous for a tobacco retailer. They do not really underwrite you up front; they let you sign up and run “back-end” underwriting once your volume or product mix trips a rule. When it does, the response is automatic: termination, and a balance held for up to 180 days against potential chargebacks, with rarely a meaningful appeal. Being fully licensed and age-gated does not help, because the objection was never to how you operate — it was to the category. Stable smoke shop payment processing has to start somewhere else entirely.

An aggregator gives you a shared merchant ID and instant, automated approval — fine for low-risk retail, a liability for tobacco and vape. A dedicated smoke shop merchant account gives you your own merchant ID, underwritten by people who actually expect nicotine volume. The first is built to onboard fast; the second is built to keep you on.

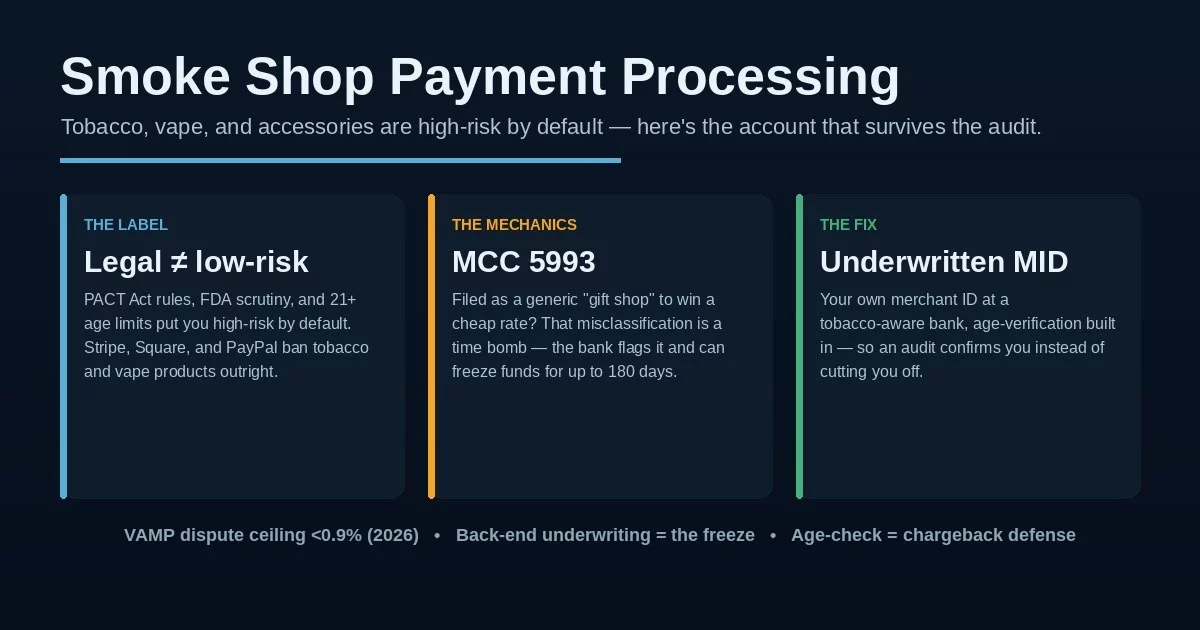

A Legal Smoke Shop Is Still “High-Risk”

Selling tobacco, cigars, and vape products is legal and licensed — so why do banks treat it as high-risk? Because “legal” and “low-risk” are not the same thing to an acquiring bank. The classification stacks up from three pressures. First is regulatory volatility: the FDA’s evolving deeming rules and PMTA review, the PACT Act’s reporting and shipping requirements, and a federal 21+ purchase age mean the rules can shift under an account at any time. Second is age-restriction liability and elevated disputes — underage buyers using a parent’s card and friendly fraud on higher-ticket glassware and devices push dispute rates up. Third is reputational and political scrutiny, with state attorneys general and activists pressing card networks to cut off non-compliant sellers, which makes conservative banks cautious about the whole category.

None of that is a judgment about whether you run a clean shop. It is a structural classification, the same one that covers other regulated categories — our overview of high-risk payment processing lays out how these accounts differ from ordinary ones. One trigger catches shops off guard: product adjacency. If you also carry hemp, CBD, or kratom, a conservative bank may de-risk the entire account over the cannabis association — the same trap the CBD and hemp world lives in. Understanding the label is the first step to building smoke shop payment processing that lasts instead of getting blindsided.

When an aggregator terminates a tobacco account, it does not just stop new sales — it can hold the money already in the pipeline for up to six months. That is payroll, inventory at the distributor, and rent locked away with no appeal, often arriving with zero warning. For most independent smoke and vape shops, a single freeze is an existential event, not an inconvenience.

What MCC 5993 Means for Your Account

Every business is assigned a Merchant Category Code that tells the card networks what it sells. Tobacco retailers are meant to ride under MCC 5993, the code for cigar stores and tobacco sellers. The problem is what happens when a processor files you somewhere else. To win your business on a cheaper rate, some processors slot a smoke shop under generic “retail” or “gift shop” — and that misclassification is a ticking time bomb. The lower rate looks like savings for a few months, until the card networks or the sponsor bank notice that your transaction pattern reads as tobacco and vape.

When that mismatch surfaces, the account can be shut down without warning and funds held for up to 180 days while the bank sorts out the exposure. A “prohibited product” flag — selling vape or kratom volume on an account approved only for cigars, for example — produces the same result. The fix is not a cheaper code; it is the correct one. Proper categorization under MCC 5993 from the start, on an account underwritten for exactly what you sell, is what makes smoke shop payment processing stable instead of fragile. Transparency at the underwriting table is cheaper than a freeze.

A processor that promises low-risk retail rates for a smoke shop is usually planning to file you under the wrong MCC. It looks like a deal until an audit catches the mismatch and the account is terminated. Correct categorization under MCC 5993 prices higher than vanilla retail — and it is the difference between an account that survives and one that disappears overnight.

What a Real Smoke Shop or Vape Merchant Account Looks Like

The durable answer for smoke shop payment processing is a dedicated, underwritten account placed with an acquiring bank that actually wants the category — not an aggregator that tolerates you until its system notices. That means your own merchant ID, individual underwriting by analysts who expect tobacco and nicotine volume, and a processor that has already cleared the risk with its sponsor bank. The same structure scales across the storefront and the website: a vape shop payment processing setup, a tobacco merchant account for a cigar lounge, or a combined smoke shop merchant account all sit under the same high-risk underwriting umbrella, with age-verification and compliance tooling built in rather than bolted on.

An underwritten vape merchant account costs more than vanilla retail, and that is expected — plan for it rather than chasing a headline rate that will not survive underwriting. Per-transaction pricing typically runs above standard retail, there is usually a monthly gateway fee, and many setups carry a rolling reserve, where the processor holds back a percentage of sales for a set period against chargebacks. None of that is a scam; it is the cost of stability. What you can control is transparency: insisting on interchange-plus pricing so the processor’s markup is a visible line item, and running any offer through an effective rate calculator so you compare true all-in costs, not the rate on the first page.

Your own merchant ID, underwriting that already accounts for tobacco and vape, correct MCC categorization, integrated age verification, and chargeback tools built for disputed device sales. You trade a slightly higher rate for the thing that actually matters — an account that is still processing next quarter.

Staying Approved — and What to Ask Before You Sign

Getting approved is the easy part; staying approved is where smoke shops get hurt. Acquiring banks keep monitoring an account long after onboarding, and the heaviest pressure is on disputes — the card networks’ dispute-ratio ceiling tightened to under 0.9% in 2026, and crossing the network thresholds can get an account terminated and land the business on the MATCH list, an industry blacklist that makes the next account far harder to open. Age verification is your best defense on both fronts: integrated ID scanning in store and identity checks online keep you compliant with the PACT Act and Tobacco 21, and they filter out the underage-buyer disputes before they ever hit your ratio. The same discipline keeps a rolling reserve from ballooning.

Whether you are opening a first account or replacing one that just got frozen, the vetting questions are concrete. Will you get your own merchant ID, individually underwritten — or are you being slotted into a shared aggregator account? Are you categorized under MCC 5993, or filed cheap under a generic retail code? Does the account cover everything you actually sell, including vape, hemp, or kratom, so nothing trips a “prohibited product” flag later? What is the reserve structure, what percentage, and when does it release? Is the pricing interchange-plus, with the markup spelled out? And read the merchant agreement closely — term length, early-termination fee, and reserve language matter most when something goes wrong. Done right, smoke shop payment processing stops being the thing that could end your business overnight and becomes just another part of running it.

Frequently Asked Questions

Not reliably. All three are aggregators whose acceptable-use policies prohibit tobacco, vape, and nicotine products, and their automated systems freeze or terminate accounts when they detect the category — often holding funds for months with no real appeal. Many shops get approved, process for weeks, and then get cut off in a back-end review. A dedicated smoke shop merchant account is the stable path to durable smoke shop payment processing.

MCC 5993 is the Merchant Category Code for cigar stores and tobacco sellers. If a processor files you cheap under generic retail or “gift shop” instead, the lower rate is a trap: when the card networks see tobacco and vape activity on a misclassified account, the bank can flag the mismatch and shut you down, holding funds for up to 180 days. Correct categorization from the start is what keeps the account stable.

It can. Carrying hemp-derived or kratom products alongside tobacco raises the account’s risk profile, and a conservative bank may de-risk the whole relationship over the cannabis association. The fix is to disclose everything you sell during underwriting and place the account with a processor that covers the full mix, so nothing trips a “prohibited product” flag later. Our guide to CBD and hemp payment processing covers that side in depth.

Keep Reading Before You Choose a Processor

Get a smoke shop processing setup built to last — not one waiting to be frozen.

Send us your current setup or a recent statement and we will show you whether you are on an aggregator that could freeze you, whether your account is categorized correctly, what a properly underwritten tobacco and vape account would cost, and how to structure it so approval actually holds — no obligation, no sales pressure. Learn more about payment processing consumer protections from the CFPB.

Review My Smoke Shop Processing SetupNo obligation • No pressure • Response within one business day