Locksmith Payment Processing: Why Emergency Work Gets You Frozen

Why Locksmiths Get Flagged as High-Risk — and Frozen

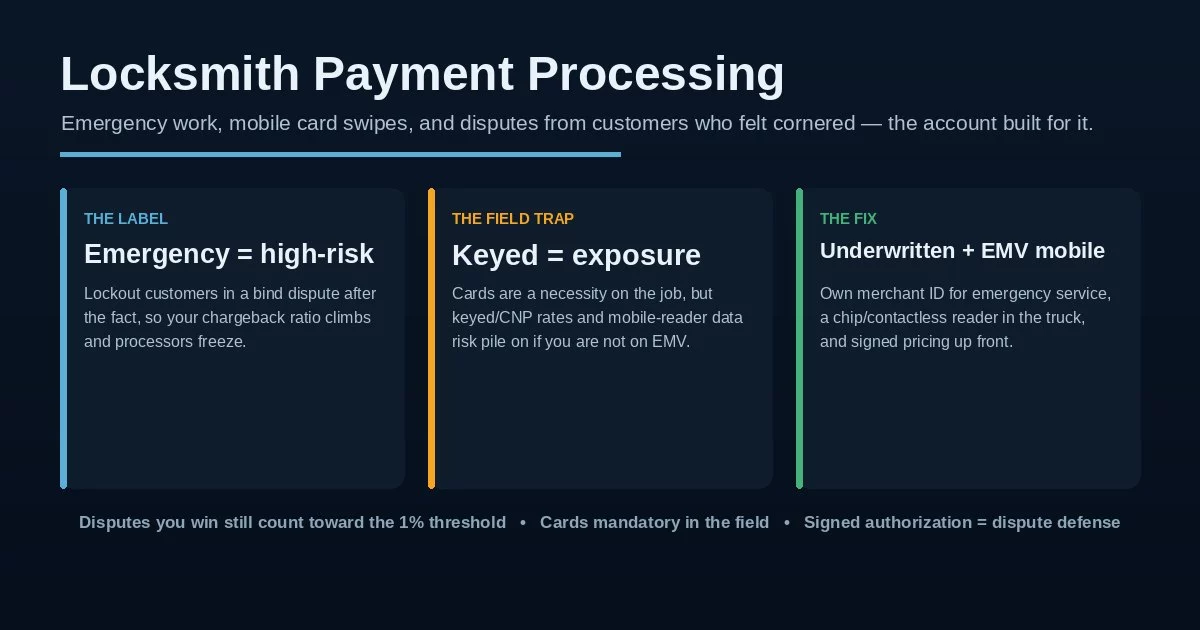

Locksmith payment processing tends to break in a way most trades never see. You open a standard merchant account — or sign up with an aggregator like Square or Stripe — and start taking cards on emergency lockout calls. Then a handful of customers dispute the charge after the fact, your chargeback ratio creeps up, and the processor responds with a hold, a reserve, or a frozen account. Nothing about the work was wrong; the business model itself looks like risk to an underwriter who never planned for it.

That is the trap. Locksmithing sits in a small group of emergency, come-to-you services — alongside towing and roadside help — where the customer is often stressed, sometimes feels cornered, and reaches for a dispute later even on legitimate work. A locksmith merchant account has to be built for that reality from the start, not bolted onto a vanilla account that panics the first time the dispute rate ticks up.

Standard accounts assume a calm, in-store buyer who chose to be there. A locksmith’s customer is locked out of a car or a house, often at night, paying under pressure — the exact conditions that produce after-the-fact disputes. The same emergency that wins you the job is what makes a conventional processor nervous about the account.

The Distress-Purchase Dispute Problem

Here is the heart of it. A customer locked out at midnight is not in a buying mood — they are relieved to be back in, then they see the bill and some of them feel taken advantage of. A share of those customers dispute the charge, framing a fair emergency call as “I was overcharged” or “I didn’t authorize that.” The hard part is the math: even when you win, the dispute still counts. Most locksmith disputes are decided in the merchant’s favor, but every one of them lands in your chargeback ratio first — and that ratio is what the card networks watch.

Cross the networks’ line and the consequences are real. Sitting above the chargeback ratio thresholds — roughly 1% for Visa — puts the account into a monitoring program, then toward termination and the high-risk merchant account world, where a fresh start is harder. Add in that a lot of locksmith work is quoted over the phone and keyed in, which reads as card-not-present and carries its own friendly-fraud exposure, and you can see why locksmith credit card processing gets the high-risk label even when every job is clean. Sound locksmith payment processing starts by naming the business as emergency service at underwriting, so the dispute pattern is expected rather than alarming.

It is not the individual dispute that hurts — it is the ratio. A run of even winnable disputes during a busy month can push you over the line, and the processor doesn’t wait for the rulings. The account gets monitored, reserved, or frozen on the trend, which means working capital locked up exactly when your call volume is highest.

Mobile Acceptance Is a Necessity — and a Risk

Locksmiths can’t run a register. The work happens at the curb, the driveway, or the parking lot, and customers increasingly carry no cash and no checkbook — so taking cards in the field is not optional, it is the business. The problem is how that card gets taken. Keying a number into a phone or virtual terminal, or quoting and charging over the phone, runs the transaction as card-not-present: a higher interchange rate and weaker dispute protection. And accepting cards on a phone or tablet adds a data-security dimension at the point of capture that a fixed countertop terminal never had.

The fix is to make the field acceptance work for you instead of against you. A proper EMV chip-and-contactless reader paired to your phone runs the sale as card-present — lower cost and far stronger dispute footing, because a dipped or tapped card is hard for a customer to later call unauthorized. Pair that with on-the-spot mobile payment processing on a real account, and the field stops being the weak point. Locksmith payment processing done right treats the truck like a point of sale, not a workaround.

Every keyed or phone-quoted sale costs more and defends worse than a dipped or tapped one. If your current setup leans on a virtual terminal because the “card reader was a hassle,” that convenience is quietly raising your rate and weakening every dispute you’ll later have to fight. Locksmith payment processing that runs card-present in the field is cheaper and far easier to defend.

What the Right Locksmith Setup Looks Like

The durable answer is a dedicated locksmith merchant account placed with a processor that underwrites emergency, come-to-you services on purpose — a true emergency service merchant account, not a generic plan — your own merchant ID, not a slot in a shared aggregator pool that deplatforms first and asks later. Pair it with an EMV chip-and-contactless mobile reader so field jobs run card-present, and insist on interchange-plus pricing so the markup is a visible line you can audit rather than a blended rate that hides the keyed surcharge. Run any quote through an effective rate calculator to compare true all-in cost.

The other half of the fix is operational, and it is the part that actually lowers disputes: price the job before you do it. A signed or digitally agreed work authorization with the price on it — even a quick on-screen signature on the reader — converts “I didn’t agree to that” into a documented yes, which is exactly the evidence that wins a dispute. Clear upfront pricing, an itemized receipt, and a photo of the completed work give you a defense file before the chargeback ever arrives. Tools like Compelling Evidence 3.0 exist so a documented merchant can win — but only if the documentation exists.

Your own merchant ID the locksmith merchant account underwritten for your dispute pattern, an EMV/contactless reader that makes field sales card-present, interchange-plus you can audit, and a signed-authorization habit that turns disputes into wins. You trade a little setup effort for an account that doesn’t freeze the week your phone won’t stop ringing.

Staying Approved — and What to Ask Before You Sign

Approval is the easy part; keeping the account is where emergency-service merchants get hurt, and the whole game is the chargeback ratio. Keep it low operationally: quote and get agreement before the work, dip or tap instead of keying, hand over an itemized receipt, photograph the finished job, and fight the disputes you should win with documentation rather than eating them. When a customer does dispute, the chargeback process rewards the merchant who can show a signed authorization and proof of completion — and the same discipline keeps you clear of friendly fraud that would otherwise stick. If a processor is already holding your funds, that pattern is the reason and the fix.

Whether you’re opening a first account or replacing one that just froze, the questions are concrete. Will you get your own merchant ID, individually underwritten for emergency service — or a shared aggregator account that can drop you? Does the reader run EMV chip and contactless so field jobs are card-present? Is the pricing interchange-plus with the markup itemized? What is the reserve structure, if any, and when does it release? And read the merchant agreement closely — term length, early-termination fee, and reserve language matter most when a busy month spikes your dispute count. Done right, locksmith payment processing stops being the thing that freezes your cash flow and becomes just another tool on the truck.

Frequently Asked Questions

Mostly because of disputes. Emergency lockout customers are stressed and paying under pressure, and a share of them dispute the charge afterward even when the work was legitimate. Most of those disputes are decided in the locksmith’s favor, but every one still counts toward the chargeback ratio the card networks watch — and a lot of locksmith work is phone-quoted and keyed, which adds card-not-present risk. The combination earns the high-risk label even when the business is clean, which is why locksmith payment processing belongs on an account underwritten for it.

Price the job before you do it and get agreement. A signed or on-screen work authorization with the price on it, clear upfront pricing, an itemized receipt, and a photo of the finished work turn “I didn’t agree to that” into a documented yes — the exact evidence that wins a dispute. Dipping or tapping the card instead of keying it also makes the sale card-present, which is much harder for a customer to call unauthorized.

Almost always. Keying a number or charging over the phone runs as card-not-present: a higher interchange rate and weaker dispute protection. An EMV chip-and-contactless reader paired to your phone runs the sale card-present — lower cost and far stronger footing if the charge is ever disputed. For a come-to-you business, a real mobile reader on a proper account is the single biggest upgrade to your locksmith credit card processing.

Keep Reading Before You Choose a Processor

Get a locksmith processing setup that survives your busiest week.

Send us your current setup or a recent statement and we’ll show you whether you’re on an account that could freeze on a dispute spike, whether you’re overpaying on keyed sales that should be card-present, what a properly underwritten emergency-service account would cost, and how to build the dispute defense in before the next chargeback — no obligation, no sales pressure. Learn more about payment processing consumer protections from the CFPB.

Review My Locksmith ProcessingNo obligation • No pressure • Response within one business day