SaaS Payment Monetization: The Three Routes and Which One Fits

Every software platform that touches a transaction eventually asks the same question: should we be earning on the payments our customers already run through us? SaaS payment monetization is the answer to that question — turning payment processing from a feature you pay for into a revenue line you earn from. The catch is that the routes to get there are wildly different in cost, risk, and time, and picking the wrong one can sink months of engineering into a payments business you never wanted to run.

This is a plain-spoken guide to the three ways a software company can monetize payments, what each actually costs, and how to tell which one fits where your platform is today. For the strategic backdrop on why payments became a SaaS revenue story at all, our piece on embedded payments for SaaS sets the stage; this page is about the mechanics of the decision.

The Three Routes to SaaS Payment Monetization

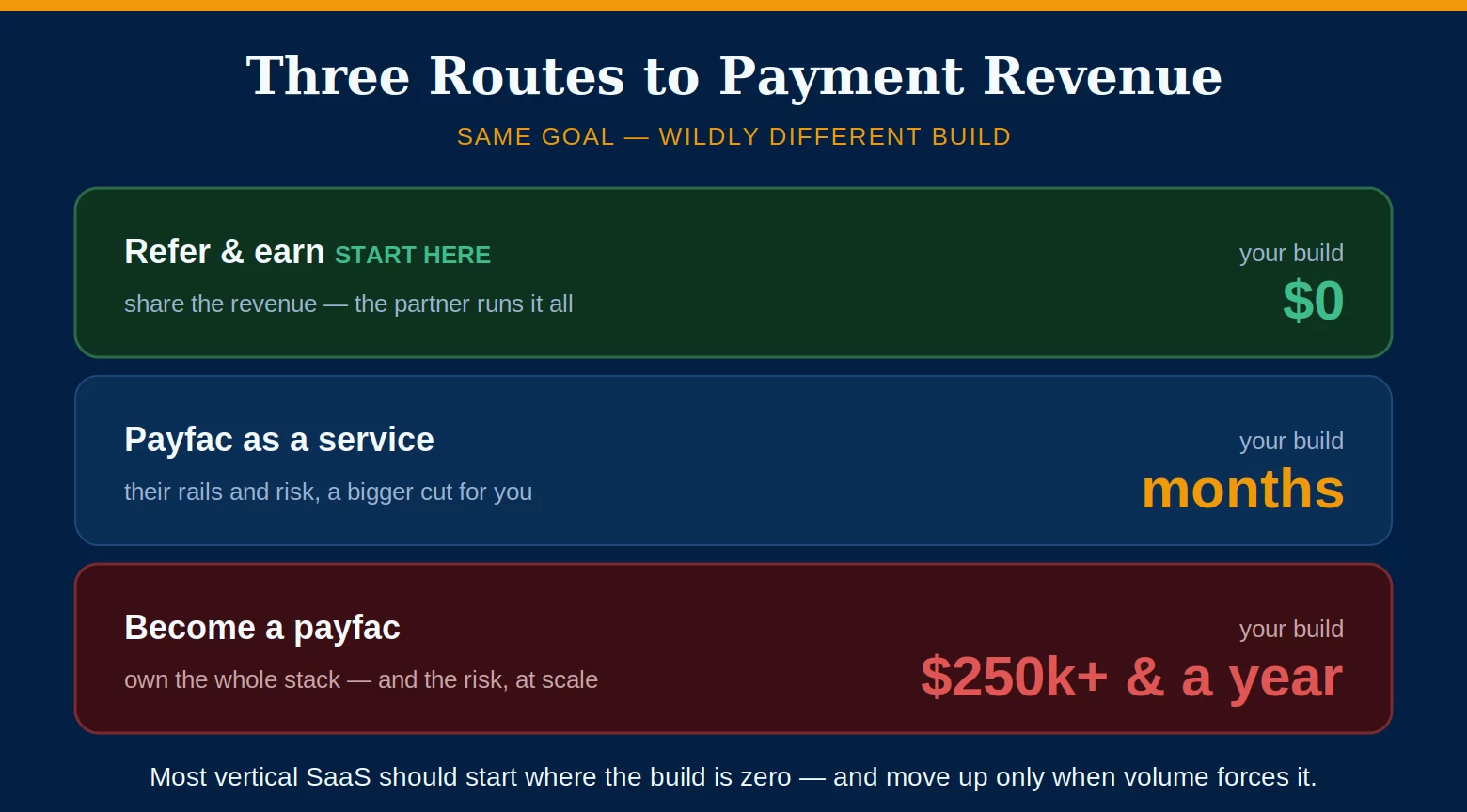

There is no single way to monetize payments. There is a spectrum, running from “build a payments company inside your company” to “refer your users and collect a share.” Three routes cover almost every platform.

You underwrite your own sub-merchants, own the risk and compliance, and take the largest slice of each transaction. It is the most lucrative route per dollar processed — and by far the heaviest. Registration with the card networks, PCI validation, underwriting, funding reserves, and ongoing risk operations turn your software company into a regulated payments business. It only makes sense at real scale.

Providers like Stripe Connect, Finix, and Payrix give you payfac-like economics without building the infrastructure yourself. You get a cut of processing and a faster path to live, while they carry the heaviest compliance and risk machinery. The trade is margin and control: you earn less than a true payfac and you are tied to their rails, pricing, and roadmap.

You refer your customers to a payments partner who underwrites and services them directly, and you earn an ongoing revenue share on the processing — with zero infrastructure to build and nothing to maintain. This is the lightest form of SaaS payment monetization, and for most vertical and subscription platforms it is where the math starts making sense long before a payfac ever would.

What Each Route Actually Costs You

The revenue side of these routes is easy to fall in love with. The cost side is where platforms get surprised, and it is what should actually drive the decision.

The payfac route routinely runs into six figures before a single transaction clears — network registration, a PCI Level 1 audit, underwriting and risk tooling, legal, and funded reserves — plus a year or more of build and a permanent risk-operations headcount. Below serious volume, the assessments and overhead swallow the extra margin, and the payments business becomes a distraction from the software. Payfac economics only pencil out once your processing volume is very large and very predictable.

Payfac as a service compresses that cost dramatically but does not erase it — you still integrate, you still shoulder some risk, and you still owe a chunk of the upside to the provider. The referral partner route inverts the equation entirely: no build, no reserve, no compliance burden, and payment revenue share that starts the month your first customer is placed. For a platform whose core business is software, not payments, that inversion is the whole point of practical SaaS payment monetization.

How to Choose the Right SaaS Payment Monetization Route

The right route is a function of two things: how much payment volume your customers already generate, and how much of a payments company you actually want to become.

If you are a vertical or subscription SaaS earning nothing on payments today, start with a referral partner — you capture revenue immediately with no build and learn what your customers’ processing actually looks like. Graduate to payfac as a service when that volume is large enough to justify the integration and the margin gap matters. Build a true payfac only when you are processing at a scale where owning the whole stack clearly beats sharing it. Most platforms never need to leave the first two.

The mistake is inverting that order — committing to a payfac build on projected volume, then discovering the compliance and risk load outweighs the revenue for years. Starting light keeps SaaS payment monetization a revenue line rather than a second company, and lets the numbers, not the pitch decks, decide when to move up.

The Low-Lift Route, Run for You

Brookside is the referral partner in that first tier of SaaS payment monetization. When your platform sends us a customer, we underwrite and place them on transparent interchange-plus pricing, service the account directly, and share the processing revenue back with you — no payfac to build, no risk to carry, no reserves to fund. For a software company that wants payment revenue without becoming a payments company, it is the fastest honest way to monetize payments, and the one you can turn on this quarter instead of next year.

Frequently Asked Questions

No. Becoming a payment facilitator is the heaviest of three routes and only pays off at large, predictable volume. A referral or ISO partnership earns you a payment revenue share with no build, no compliance burden, and no reserves, and payfac as a service sits in between. Most platforms should start light and only build a payfac if the volume clearly justifies it.

A true payfac owns underwriting, risk, compliance, and network registration — a full payments business inside your company. Payfac as a service, from providers like Stripe Connect, Finix, or Payrix, gives you similar economics while the provider carries the heaviest infrastructure and risk. You launch faster and cheaper, but earn less per transaction and depend on their rails.

You refer your customers to the payments partner, who underwrites and services them and places them on their own merchant accounts. You earn an ongoing share of the processing revenue those customers generate — recurring income tied to volume, with nothing to build or maintain on your side. It is the simplest form of SaaS payment monetization to stand up.

Go deeper on the payments stack

Let’s Talk About a Payments Partnership.

If your platform runs customer payments and you want to earn on them without building a payfac, Brookside will map the revenue-share math against your customers’ actual volume and show you what a referral partnership would return — no build, no obligation. Learn more about payment processing consumer protections from the CFPB.

Start a Partnership ConversationNo obligation • No pressure • Response within one business day