Why Your SaaS Vendor Will Push Harder on Payments as AI Eats Their Subscription Revenue

The Embedded Payments SaaS Narrative Is Half Right and Half Wrong

The current story about embedded payments SaaS and the broader software industry goes like this. AI is eating seat-based pricing. Agents replace seat-licensed users. Consumption pricing replaces flat subscriptions. The traditional SaaS revenue model — pay per user per month, expand seats as the company grows — is in structural retreat.

The first half of that story is correct. Gartner, BetterCloud, and a dozen industry analysts have documented the trend through 2025 and into 2026. AI-driven productivity tools genuinely compress seat counts. Outcome-based and consumption-based pricing genuinely cannibalize the predictable subscription line item. CFOs at software vendors are openly discussing how to defend revenue as agentic AI displaces the human workflow their software was designed to support.

The second half of the story — the implication merchants are quietly being asked to accept — is wrong. The prevailing narrative says that as subscription compresses, vertical software vendors will be forced to compete harder, lower prices, and loosen their grip on the merchants who use them. The opposite is happening. As subscription revenue erodes, platforms are doubling down on captive payments capture, not loosening their grip on it. The captive payments arrangement that gave Toast 6x more revenue from fintech than from subscriptions in 2025 is the lifeline these platforms are now pulling on harder, not the appendage they are dropping.

This post explains why. It also explains what the merchant who runs their dental practice on Eaglesoft, their restaurant on Toast, their salon on Mindbody, their contracting business on ServiceTitan, or their boutique on Shopify needs to understand about where the relationship is going. The short version: the processing rates have not yet drifted to where they will drift. The strategic logic of the vertical SaaS platform now favors capturing more, not less, of the merchant’s payment processing economics.

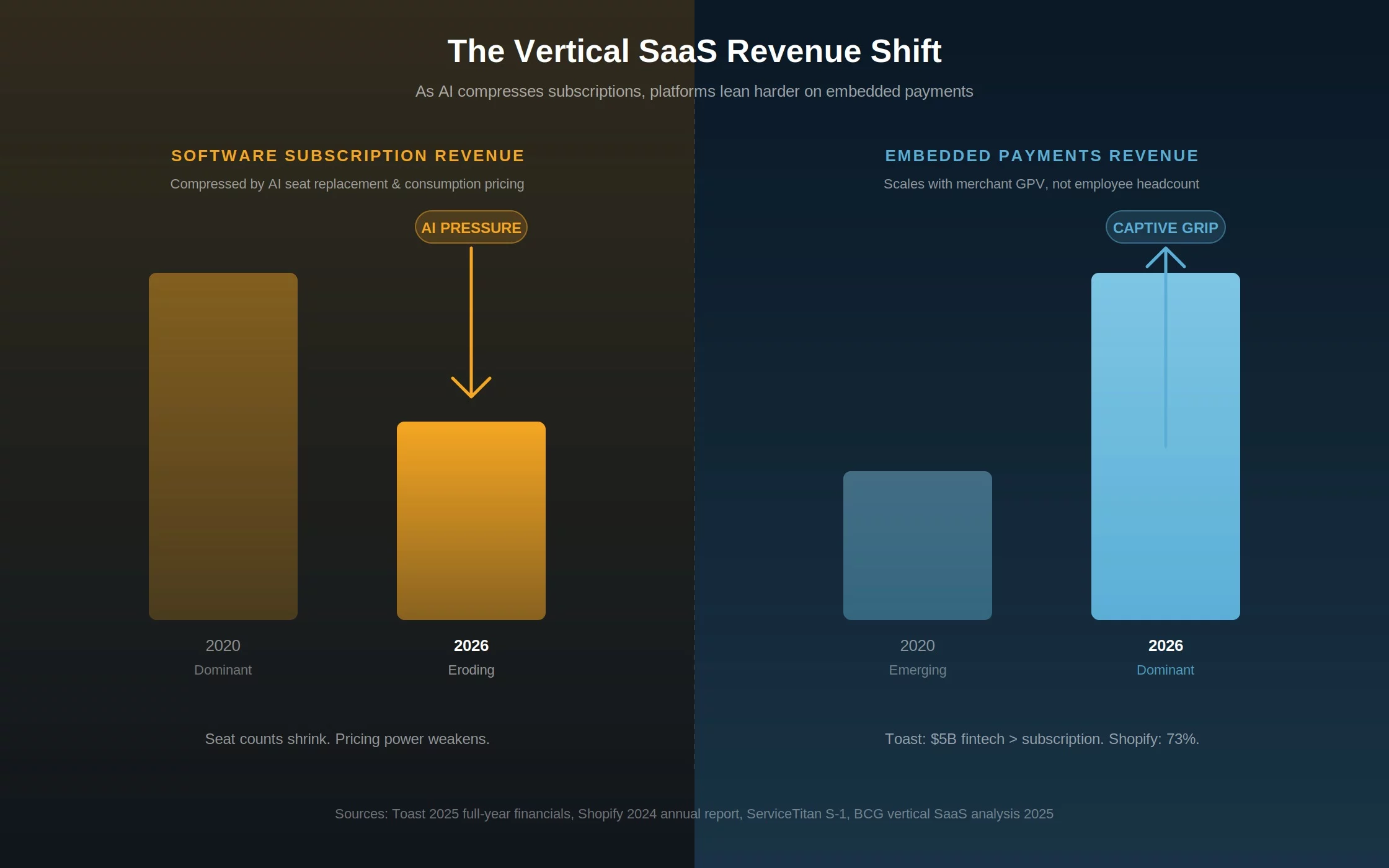

Embedded Payments SaaS Is Already the Bigger Half of the Business

The shift from subscription-dominant to payments-dominant revenue at these platforms is not a forecast — it has already happened at the largest operators. The 2025 full-year financials make the structure visible.

Toast, the restaurant operating system serving 164,000 locations, reported approximately $5 billion in 2025 financial services revenue against substantially smaller subscription revenue. Payments revenue is roughly six times the size of the subscription line. Annual processing volume through Toast’s payment rails hit $195 billion in 2025.

ServiceTitan, the home services platform whose customers are contractors, plumbers, and HVAC operators, reported a revenue split at its 2024 IPO of 71% subscription, 25% fintech, and 4% services. The fintech line — usage-based payment processing revenue — was growing materially faster than the subscription core. Industry analysts project the fintech share will continue expanding through 2026 and 2027.

Shopify, the e-commerce platform, reported that 73% of total company revenue in 2024 came from merchant solutions — payments, capital, shipping — versus only 27% from the subscription product itself. The platform that began as “rent the software” has become “use the software, pay us the payments fees.”

The broader market structure follows the pattern. The Boston Consulting Group’s 2025 software industry analysis documented that software platforms now manage 60% to 70% of their merchants’ payment processing contracts. Andreessen Horowitz separately reported that adding fintech capabilities increases a software platform’s revenue per customer by two to five times. The US embedded finance market grew to approximately $24.7 billion in 2024 and is projected to grow at 30% annually through 2034.

Vertical SaaS platforms are not lightly attached to payments. Payments revenue is now structurally larger than subscription revenue at the largest operators, growing faster than subscription revenue, and growing at consumption rates rather than seat rates — which means payments revenue scales with the merchant’s business size rather than their employee count. This is the revenue line AI cannot easily disrupt. It is also the revenue line that depends entirely on the merchant continuing to process payments through the platform’s preferred rails at the platform’s preferred margins.

Why AI Pressure on Subscriptions Makes Captive Payments More Important

The mistake the prevailing narrative makes is assuming that pressure on one revenue line forces a vendor to relax pressure on the other. The opposite holds. When subscription revenue is threatened, the rational response of a vertical SaaS platform is to lean harder on the revenue line that is not threatened. Captive payments is that line.

Three strategic dynamics make this true at every platform of meaningful scale.

Payments revenue scales with the customer, not the customer’s headcount — and how a platform monetizes those payments, from payfac to a referral partner, sets how much of it stays with the software company. A dental practice that grows from $1 million to $2 million in annual revenue does not double its software seats. It might add a hygienist or two — perhaps 10% headcount growth against 100% revenue growth. Subscription revenue at the SaaS vendor barely moves. Payments revenue doubles. As AI compresses seat counts even further, the gap between subscription-revenue growth and payments-revenue growth widens — and payments becomes the only line that captures the merchant’s actual business expansion.

Payments revenue is sticky in ways subscriptions are not. A merchant frustrated with their software subscription cost can negotiate, downgrade, or churn. A merchant locked into the platform’s captive payment processor faces a much higher switching cost — replacing the payment rails typically means re-implementing the integration, retraining staff, and accepting operational disruption during the transition. The platform knows this. Pricing pressure on the subscription side is absorbed by the platform; pricing pressure on the payments side is absorbed by the merchant.

Payments margin is invisible to most merchants in ways subscription cost is not. The merchant sees the monthly software invoice and can calculate it against ROI. The merchant rarely calculates effective payment processing rate — and when they do, they typically discover the rate has crept higher year over year without any contract change. PYMNTS reported in 2026 that embedded payments are now being explicitly framed by industry strategists as the “lifeline” for vertical SaaS in the AI era. The framing is honest. The merchant is the lifeline.

Subscription pricing is constrained by the merchant’s ability to comparison-shop. Payments pricing is constrained by the merchant’s ability to understand the statement. The first constraint is tightening as AI makes software easier to evaluate. The second constraint is not. This asymmetry is why vertical SaaS platforms can be losing subscription leverage and gaining payments leverage simultaneously — and why the strategic response of those platforms is to extract more from the side where the merchant has weaker tools.

The Specific Patterns Merchants Are Already Seeing

The macro shift in platform economics produces specific, predictable patterns at the merchant level. Each of these is documented across Brookside’s reduce-X-payments-fees coverage.

Processing rates that creep up year over year without any contract change. A dental practice on Eaglesoft Payments, a restaurant on Toast, a salon on Vagaro, or a contractor on ServiceTitan typically experiences a 5 to 15 basis point effective rate increase each year on the same card mix and the same transaction volume. The increase comes from a combination of network interchange adjustments retained by the platform, “convenience” surcharges added without notice, and the natural drift of card mix toward premium tiers that carry higher interchange. The platform captures the difference. The merchant absorbs it.

“Required” payment integrations that block alternative processors. Five years ago, most platforms supported third-party payment processor integrations. Today, most have either deprecated those integrations, restricted them to legacy customers, or buried them behind technical and procedural barriers that effectively force new customers onto the platform’s captive payment processor. This is by design. Captive payments economics depend on the captive arrangement being the path of least resistance.

Convenience features that require captive payment routing. A new feature ships — automatic patient billing, online ordering, recurring service charges, capital advances — and the feature only works when payments route through the platform’s captive processor. The merchant who uses an outside processor discovers the feature is unavailable to them. Features are increasingly chosen to reinforce the captive arrangement, not to operate independently of it.

Capital products that require captive payment volume. Toast Capital, Shopify Capital, Square Capital, and similar platform-affiliated lending products underwrite based on the merchant’s payment volume through the platform. Merchants who diversify their processing lose access to these capital products. The capital offering is structured to penalize independence from the captive payment relationship.

None of these patterns are new. What is new is the strategic context. AI pressure on subscription revenue does not just allow these patterns to continue — it accelerates them. The platform’s economic survival now depends on the captive payments relationship in a way it did not five years ago, when subscription revenue was a viable growth lever on its own.

The Merchant Position That Holds Up Under This Pressure

The strategic shift at these platforms does not require the merchant to abandon the platform. It requires the merchant to understand the relationship for what it is and to defend the parts of the cost structure the platform is most aggressively trying to capture.

Three principles hold up under sustained pressure.

Keep the platform. Replace the processor when possible. The platform product is usually genuinely valuable — the dental practice does need Eaglesoft, the restaurant does need Toast, the contractor does need ServiceTitan. The captive payments arrangement is a separate question. Wherever the platform still supports third-party processor integration, the merchant who routes payments to an independent processor typically captures 30 to 60 basis points in immediate cost reduction without sacrificing platform functionality. The reduce-X-payments-fees series documents this pattern across Toast, Dentrix, Eaglesoft, CT Payments, Vagaro, and Lightspeed.

Move to interchange-plus pricing. The captive payments arrangement at most these platforms relies on flat-rate or tiered pricing, both of which hide the interchange increases the platform captures over time. Interchange-plus pricing exposes every component on every statement, which is exactly why most platforms do not offer it as the default. Moving to interchange-plus, whether through the platform or through an outside processor, restores the merchant’s ability to see what is actually being charged.

Audit effective rate annually, not transactionally. The merchant who checks individual transaction rates is looking at the wrong number. The number that matters is total processing cost divided by total processed volume across a twelve-month period — the merchant’s true effective rate. This number drifts up under the AI/payments pressure dynamic even when individual transaction rates appear stable. An annual audit catches the drift before it becomes structurally costly. For higher-volume merchants this can mean tens of thousands of dollars in recovered margin per year.

For broader context on how regulatory and network-level changes interact with these vendor dynamics, the recent Visa-Mastercard 2026 settlement and the Capital One/Discover debit routing change both create new merchant-side levers the captive SaaS arrangement is not optimized to capture. Merchants who understand both layers — the macro AI/SaaS shift and the underlying network rule changes — are the merchants who avoid paying for both.

Outside resources worth reading on the same dynamic: the CFPB’s published guidance on small business payment processing covers the merchant-side regulatory protections that apply regardless of the SaaS platform involved.

Frequently Asked Questions

It depends on the platform and the contract. Some vertical platforms — Toast, Square, and Shopify among them — operate as closed-loop captive payment systems where the software and the processing are bundled by design and cannot be separated without leaving the platform entirely. Others — including most dental and medical practice management systems, many home services platforms, and most retail POS systems — technically allow third-party processor integration but make it operationally difficult through technical barriers, feature restrictions, or contract clauses. The first step is reading the merchant agreement and platform documentation to determine which category your specific platform falls into. The second step is calculating what the embedded payments SaaS arrangement actually costs you annually so you know what is at stake.

Some features. Not all features. The pattern across platforms is that core functionality — appointment scheduling, inventory management, customer records, reporting — continues to work regardless of payment processor. The features that typically require captive payment routing are the newer revenue-tied add-ons: automatic recurring billing, capital advance products, certain reporting integrations, and platform-affiliated lending. The merchant’s pre-switch question is whether those specific features are worth the cost differential. For most merchants the answer is no — the cost differential between captive and independent processing typically exceeds the value of the captive-only features by a substantial margin.

Three causes typically combine. First, network interchange schedules adjust periodically — usually twice per year — and the embedded payments SaaS arrangement at most platforms passes those increases through to the merchant while retaining any decreases as platform margin. Second, the customer card mix naturally drifts toward premium and rewards tiers over time as issuing banks aggressively market those products, and premium card interchange runs 15 to 20 basis points above standard consumer interchange. Third, some platforms add small “convenience” or “compliance” surcharges that are technically permitted under merchant agreement terms but never separately announced. The combined drift typically adds 5 to 15 basis points per year on the same volume and the same nominal pricing structure. An annual effective rate audit catches all three drivers in one calculation.

Further reading on vertical SaaS payments capture, processor independence, and the underlying network rule changes

Send Your Last Three Statements. We’ll Show You What the Embedded Payments SaaS Arrangement Is Costing You.

The strategic shift inside vertical SaaS platforms is invisible on a transaction-by-transaction basis. It becomes visible when you calculate effective rate across a twelve-month window. Send Brookside your last three processing statements and we will identify your effective rate, the year-over-year drift, the line items the captive arrangement is using to capture margin, and the specific levers that apply to your platform and your card mix. The analysis takes about twenty minutes. For consumer-side regulatory context, the CFPB’s small business payment guidance covers the protections that apply across platforms.

Get Your Free Statement ReviewNo obligation • No pressure • Response within one business day