Accounting Firm Payment Processing: The Seasonal Trap

Accounting Firm Payment Processing: The Seasonal Trap

Accounting firm payment processing has a shape most processors ignore: a firm runs the bulk of its card volume in a ten-week window around tax season, then goes quiet for the rest of the year — yet the fixed monthly fees keep billing all twelve months. A generic flat-rate account treats a CPA practice like a coffee shop with steady daily sales. It isn’t one. The result is a firm that pays a premium on its busiest months and a fee floor on its slowest ones.

This is the firm-as-merchant view — your practice accepting card and ACH payments from your own clients. If instead you’re the one reviewing a client’s merchant statement, that’s a different job, and we cover it separately in the line-items a CPA should flag.

Four Months of Volume, Twelve Months of Fees

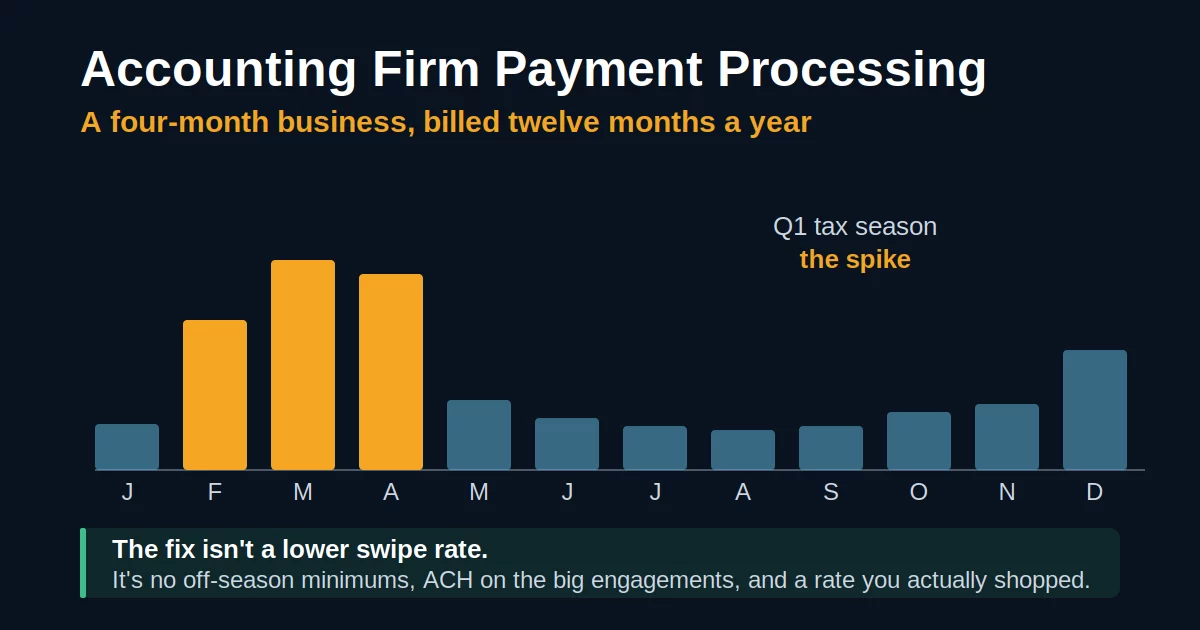

Look at a tax-and-accounting practice’s monthly card volume and you see a curve, not a line. February through April carries the returns, the balance-due payments, and the last-minute engagements. Then May arrives and the graph falls off a cliff until extension season nudges it in September. For many small firms, sixty to seventy percent of the year’s card volume lands in a single quarter.

That concentration is the whole problem. Every processor cost that is fixed — the monthly account fee, the PCI fee, the gateway fee, the statement fee, and especially the monthly minimum — is charged in July and December just as surely as it is in March, when there’s almost nothing running through the account to absorb it.

A monthly minimum works like this: if your processing fees don’t reach the floor, you pay the difference anyway. In your busy quarter you clear it easily. In August, when you might run a few hundred dollars in card payments, that minimum plus the fixed monthly fees can cost more than the fees on the transactions themselves. You’re paying for capacity you only use one season a year.

Percentage Pricing Punishes a $5,000 Invoice

Accounting work bills in large, discrete chunks: an annual tax engagement, a review, a clean-up project, an advisory retainer. When a client puts a four- or five-figure invoice on a credit card, a percentage-based rate scales right along with it — a $5,000 engagement fee can carry a card cost in the range of a good dinner out, on a single transaction.

The same $5,000 moved by ACH bank transfer typically costs a flat few dollars, often capped, regardless of the amount. On your largest invoices, the method matters far more than the rate — and getting that call right is most of what good accounting firm payment processing does. A firm that quietly routes its big annual engagements to ACH — and reserves the card for the client who insists on points — keeps a meaningful slice of every large fee it earns.

On a $6,000 engagement, a card runs a percentage of the whole thing; an ACH pull runs a small flat fee. Multiply that gap across a season of annual engagements and it stops being a rounding error. The exact card cost depends on volume, card mix, and business type — which is precisely why it should be a negotiated range, not a shelf rate you never questioned.

Your Billing Software Chose Your Processor

Most firms never actually picked their processing rate. It arrived bundled inside the billing tool. Turn on payments in Ignition, CPACharge, QuickBooks Payments, Financial Cents, or a practice-management suite, and a flat card rate comes switched on by default — convenient, integrated, and rarely the cheapest money you can find. The software’s job is to get you paid inside your workflow, not to shop your interchange.

That’s fine for a $200 invoice. It’s the single most expensive habit in accounting firm payment processing on a season of $3,000 ones. The integration is worth keeping; the rate behind it is worth challenging. In accounting firm payment processing, the embedded default is almost always a starting point, not a floor — and the firm that treats it as a floor overpays for years without ever seeing a line item that looks wrong.

What Accounting Firm Payment Processing Should Look Like

The account should match the shape of the year, not fight it. Three moves cover most of the gap:

Interchange-plus pricing passes the network’s true cost through and adds a transparent, negotiated margin on top — and a properly structured account carries no seasonal minimum to punish your quiet months. You pay for what you run, when you run it. See how the model works in interchange-plus pricing.

Default your big annual invoices and advisory retainers to bank transfer. Keep the card as the convenient exception, not the standing rail for five-figure fees.

You don’t have to leave Ignition or QuickBooks to change what you pay inside them. The processor behind the button can often be swapped or re-priced while the workflow stays exactly the same. Start by benchmarking what you pay now against your true effective rate, then move to reduce the processing rate without disrupting a single client’s payment experience.

Bookkeeping firms have a related but different problem — steady monthly recurring billing rather than a seasonal spike — and it’s worth reading alongside this: bookkeeping payment processing. For the durable case that the ACH rail is the cheaper way to move a large invoice, Nacha maintains the rules that govern it.

Frequently Asked Questions

No. In most cases the processor behind Ignition, CPACharge, or QuickBooks Payments can be re-priced or replaced while the billing workflow stays identical. The integration is worth keeping; the embedded rate is what you renegotiate.

You can, within the surcharge rules for your state and card-brand caps — but for a professional firm, ACH-first on the large invoices usually solves more of the cost than surcharging solves, and without the client friction. If you do surcharge, apply it only to credit, never debit, and disclose it clearly.

Fixed fees — the monthly account fee, PCI, gateway, statement fee, and especially the monthly minimum — bill every month regardless of volume, so off-season is where accounting firm payment processing feels most overpriced. In your quiet months there’s little processing to absorb those fees. An account with no monthly minimum and low fixed fees is the direct fix.

More on Firm Payment Processing

Send One Statement. We’ll Show You the Off-Season Bleed.

Send Brookside one recent processing statement and we’ll calculate your true effective rate, flag the fixed fees you’re carrying all year, and tell you whether ACH-first would keep more of your big engagement fees. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for Free ReviewNo obligation • No pressure • Response within one business day