Clio Payments Fees: What the August 31 LawPay Sunset Means for Your Firm

Clio Payments Fees After the August 31 LawPay Sunset

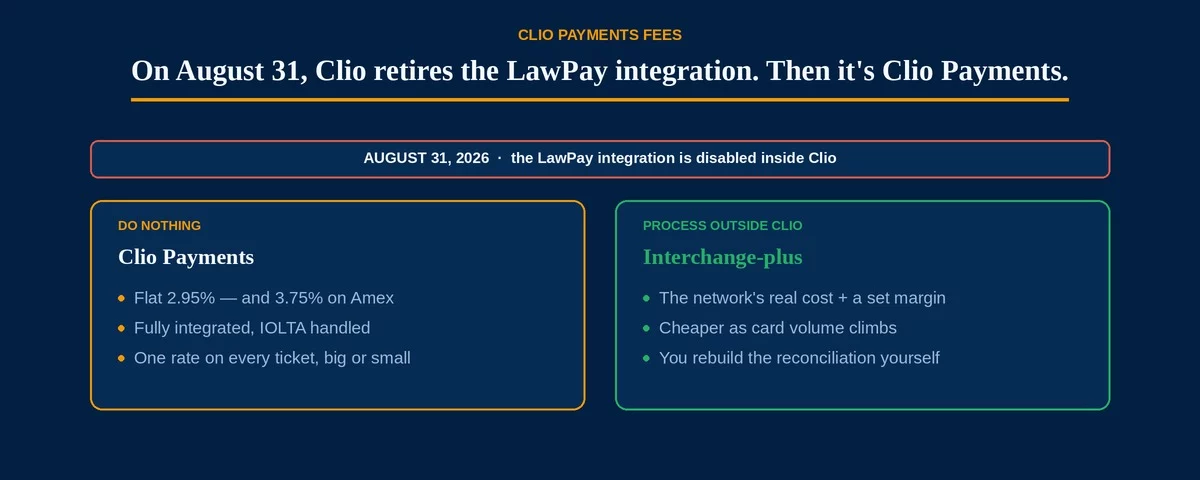

On August 31, 2026, Clio disables the LawPay integration inside its practice-management platform. Firms that have run card payments through LawPay for years will find that path closed, and the built-in alternative is Clio’s own processor, Clio Payments. For most firms this will happen quietly — a setting flips, invoices still get paid — and the rate simply becomes whatever Clio Payments charges. That is exactly why it is worth looking at Clio Payments fees now, before the change makes the decision for you.

This is not a reason to panic, and for many firms Clio Payments is a perfectly reasonable landing spot. But a flat rate applied to legal payments — which are often large and lumpy — behaves very differently than it does for a coffee shop, and the firms that pay the most are usually the ones that never stopped to check their Clio Payments fees against how the firm actually gets paid.

The LawPay API integration within the platform stops working. Your matters, billing, and trust accounting stay exactly where they are; only the payment rail underneath them changes. If you run attorney payment plans, that rail is where each installment routes to trust or operating, so it has to be set up correctly on whatever you move to. The default replacement is Clio Payments, so the practical question is no longer “which integration” but “is this rate right for how my firm gets paid.”

What Clio Payments Fees Actually Are

Clio Payments uses a flat model: one standard rate for card payments and a higher one for American Express, with no per-transaction fee and no separately itemized card-network fees. A flat rate is easy to forecast, and that predictability is a real feature — you always know what a payment will cost. The catch is what a flat percentage does to a large payment. A $10,000 estate-planning retainer or a personal-injury settlement disbursement carries the same percentage as a $200 consultation, so the dollar cost climbs in lockstep with your biggest, most important payments.

That is the difference between a headline rate and an effective rate — the total you actually pay after every payment type is blended together. For a firm whose card volume is mostly small consult fees, Clio Payments fees may land close to the sticker. For a firm collecting large retainers by card, the effective cost of that flat percentage is where the money quietly goes.

At a flat 2.95%, a $10,000 retainer paid by card costs $295 — every time. The same firm on a transparent model, or moving that retainer to a bank rail, keeps most of it. The larger and lumpier your card payments, the more a flat percentage costs you relative to the alternatives.

Route the Big Payments to ACH — Inside or Outside Clio

Before you rethink your whole processor, there is a lever that works even if you stay on Clio Payments: the bank rail. Clio Payments supports eCheck and direct ACH, and a flat-fee bank transfer beats a percentage on any large payment. A client wiring a $10,000 retainer by card costs you hundreds; the same retainer by ACH costs a flat fee measured in cents. Simply steering your largest retainers and settlements to ACH — and reserving cards for the smaller, pay-now moments — cuts your real Clio Payments fees without changing platforms at all.

- Paid by card at a flat 2.95%: $295 in fees

- Paid by ACH / eCheck: a flat fee, often under a dollar

- Do this across a year of retainers and it is the easiest saving on the board

For firms handling trust funds, this also keeps things clean: earned and unearned money stays separate, and the fee side never touches the IOLTA account. Moving large payments to ACH is the rare change that is both cheaper and simpler.

When It’s Worth Processing Outside Clio

If your firm runs meaningful card volume, the deeper question is whether the flat Clio Payments fees fit your firm at all. The alternative is to process on interchange-plus outside the platform — paying the network’s real cost plus a set, visible margin instead of a blended flat percentage. On volume, and especially on large card payments, that gap is real money over a year.

Be honest about the trade, though, because it is a real one. Processing outside Clio Payments means giving up the native integration — payments no longer post themselves against matters and bills automatically, so you rebuild that reconciliation step, and you take on trust-accounting discipline yourself rather than letting the platform handle it. For a solo firm with modest card volume, that trade usually is not worth it, and Clio Payments plus ACH is the right answer. For a firm with high card volume or frequent large tickets, the savings can more than cover the added workflow — the math is worth running before August 31, not after.

Any processor you use for a law firm has to keep earned and unearned funds separate and must never debit fees or chargebacks from an IOLTA trust account. Clio Payments handles this natively; an outside interchange-plus setup can do it too, but it has to be configured for trust compliance from day one. This is a related but different question from LawPay’s own recent rate changes — see what happened to LawPay’s rate for that story.

Frequently Asked Questions

No — but it becomes the default. After August 31, 2026 the LawPay integration inside the platform stops working, so Clio Payments is the built-in way to take payments without leaving the platform. You can still process on another provider outside the platform; you just give up the native, automatic reconciliation.

Clio Payments uses a flat rate — one percentage for standard cards and a higher one for American Express — with no per-transaction fee and no separately passed network fees. It is simple to predict, but because it is flat, the cost on a large retainer or settlement scales straight up with the payment size.

Two ways. First, route large retainers and settlements to ACH or eCheck, where a flat bank-rail fee beats a percentage — this works even if you stay on Clio Payments. Second, if your card volume is high, weigh interchange-plus outside the platform, where a transparent rate can beat a flat percentage by enough to justify rebuilding the reconciliation step.

The law-firm picture, the pricing models, and the rail that does the work

Send Us One Statement. We’ll Show You the Markup.

If your firm takes card payments and the LawPay sunset is about to set your Clio Payments fees by default, this is the moment to know your real number. Send Brookside one recent processing statement and a rough sense of how your largest retainers and settlements get paid, and we’ll calculate your true effective rate, show which payments belong on ACH, and tell you honestly whether interchange-plus outside Clio would save enough to be worth the workflow — or whether Clio Payments plus an ACH habit is the right call for your firm. The math takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day