Bookkeeping Payment Processing: The Recurring-Rate Markup

Bookkeeping Payment Processing: The Recurring-Rate Markup

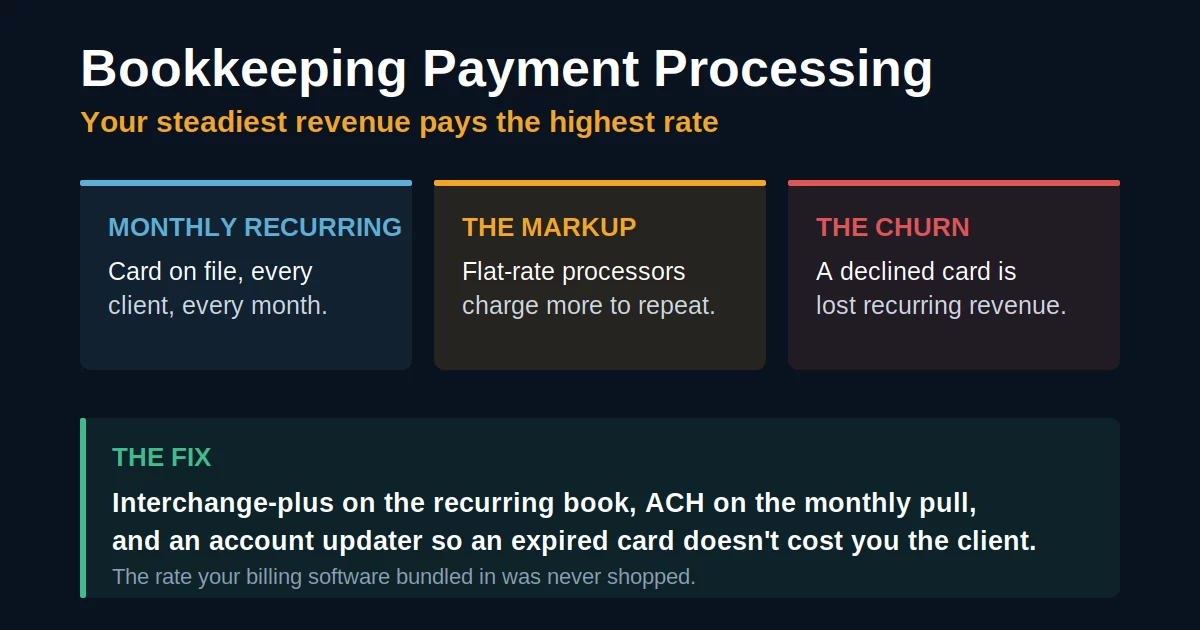

Bookkeeping payment processing has a quiet trap built into it: your steadiest, most valuable revenue stream — the monthly recurring retainer — is often the one your processor charges the most to collect. A bookkeeping practice runs almost entirely on card-on-file and scheduled charges, and flat-rate processors tend to price recurring, card-not-present payments higher than a card someone taps in person. Your best clients, billed the most predictable way, sit in the most expensive bucket — which is the central irony of bookkeeping payment processing.

This is your practice accepting payment from its own clients. If you’re instead reviewing a client’s statement for fees they’re overpaying, that’s the auditor’s job, covered in statement line-items bookkeepers flag.

A Book of Monthly-Close Clients Is a Subscription Business

Client advisory and monthly-close work moved the profession off the hourly invoice and onto fixed recurring fees — a shift the AICPA’s own practice-management data ties to faster revenue growth per client. That’s good for the firm. It also means your payments look nothing like a retail shop’s: instead of many small one-off sales, you have a stable list of clients each paying a set amount on the same date every month, on a card or bank account you keep on file.

This is the clean line between bookkeeping payment processing and a tax-and-accounting firm’s setup. A CPA practice spikes in the first quarter and goes quiet; a bookkeeping practice bills a flat, predictable amount every month, all year. The seasonal problem is theirs. The recurring problem is yours — and the seasonal-versus-recurring split is exactly why the two need different accounts. The tax-firm version lives in accounting firm payment processing.

Card-on-File Is Usually the Priciest Way to Get Paid

A flat-rate processor typically quotes one headline number for a card tapped in person and a higher one for a card stored and charged on a schedule — the card-not-present, recurring rate. Because a bookkeeping practice runs the overwhelming majority of its revenue through exactly that channel, the higher rate isn’t an edge case you hit occasionally. It’s the rate on almost everything — the reason bookkeeping payment processing rewards a shopped account more than most businesses.

If seventy or eighty percent of your revenue is recurring and the recurring rate is the highest one on your agreement, then a fraction of a percent isn’t cosmetic — it’s a fraction of a percent applied to nearly your whole book, every month, forever. That’s the same math that makes recurring-revenue businesses like gyms overpay; see gym payment processing.

A Declined Card Is Lost Monthly Revenue

The second cost is quieter than the rate and often larger. Cards expire, get reissued after fraud, or hit a limit. When a stored card fails on the monthly run, that client’s payment doesn’t just slip — if nothing catches it, the charge silently stops. This is involuntary churn: revenue you already earned and expected, gone not because the client left but because a sixteen-digit number changed.

An account updater refreshes a stored card automatically when the issuer reissues it, so the monthly charge keeps working without a client ever knowing. A proper dunning sequence retries a failed payment on a schedule and nudges the client before the balance ages. Most bundled billing tools do one, both, or neither — and knowing which is a real question to ask, not a footnote.

What Bookkeeping Payment Processing Should Look Like

The account should be built around a recurring book, not a checkout counter. Three moves carry most of the value:

Replace the flat recurring rate with interchange-plus pricing, which passes the network’s real cost through and adds a transparent margin — instead of a blended flat rate quietly padded for card-on-file. On a book that’s mostly recurring, this is where the money is.

A recurring bank draft costs a small flat fee — often capped — no matter the amount, and doesn’t expire the way a card does. Defaulting your monthly retainers to ACH cuts both the rate and the churn in one move, and leaves the card for clients who insist on it.

You don’t have to leave Ignition, Anchor, Financial Cents, or QuickBooks to fix this. The processor behind the payments button can be re-priced and configured for account-updater and dunning while your billing workflow stays exactly the same. Benchmark what you pay today against your true effective rate first.

The recurring nature of bookkeeping payment processing is the whole reason the wrong account is so expensive — and the same reason the right one compounds in your favor. The ACH rail that carries the cheaper monthly pull is governed by Nacha.

Frequently Asked Questions

For a fixed monthly retainer, almost always. A card charges a percentage every month; an ACH draft charges a small flat fee, often capped, and doesn’t expire. Across a full book of monthly-close clients, the difference is substantial — and it removes most involuntary churn at the same time.

It automatically refreshes a stored card when the issuer reissues or renumbers it, so your monthly charge keeps running when a card expires or is replaced after fraud. Without it, a reissued card silently stops paying you — lost revenue from a client who never actually left.

No. In bookkeeping payment processing the rate is set by the processor behind your billing tool, not the tool itself. In most cases that processor can be re-priced onto interchange-plus and configured for account-updater while your Ignition, Anchor, or QuickBooks workflow stays unchanged.

More on Firm Payment Processing

Send One Statement. We’ll Show You the Recurring Markup.

Send Brookside one recent processing statement and we’ll calculate your true effective rate on recurring charges, show you whether an ACH pull would cost less, and flag how much involuntary churn an account updater is leaving on the table. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for Free ReviewNo obligation • No pressure • Response within one business day