Attorney Payment Plans: Where the Money Actually Goes

Attorney Payment Plans: Where the Money Actually Goes

Attorney payment plans let a client pay a legal fee in scheduled installments instead of one lump sum — which makes representation reachable and smooths a firm’s cash flow, but quietly hands the firm a trust-accounting problem most payment setups aren’t built to handle. Every installment has to land in the correct account, and the processing fee has to come out of the correct one. Get either wrong and a convenience feature becomes an ethics exposure — which is why attorney payment plans deserve more than a generic merchant account.

This is a payment-plan mechanic, not a primer on legal merchant accounts. For the broader vertical — trust accounts, retainers, and how a firm should accept cards generally — start with law firm payment processing.

A Payment Plan Is Not Fee Financing

These get used interchangeably and they aren’t the same. With a direct payment plan, the firm charges the client’s card or bank account on a set schedule, carries the collection risk itself, and usually charges no interest. With legal-fee financing, a third-party lender pays the firm the full fee upfront, net of a processing cost, and the client repays the lender over time with interest.

Financing suits a flat-fee matter where the firm wants the whole fee now — an uncontested divorce, an estate plan, an immigration filing. A direct payment plan suits a client who simply needs to spread a known cost, and a firm comfortable managing the schedule. Many firms offer both, and both count as attorney payment plans to the client. The trust question below applies to both, but bites hardest on the direct plan.

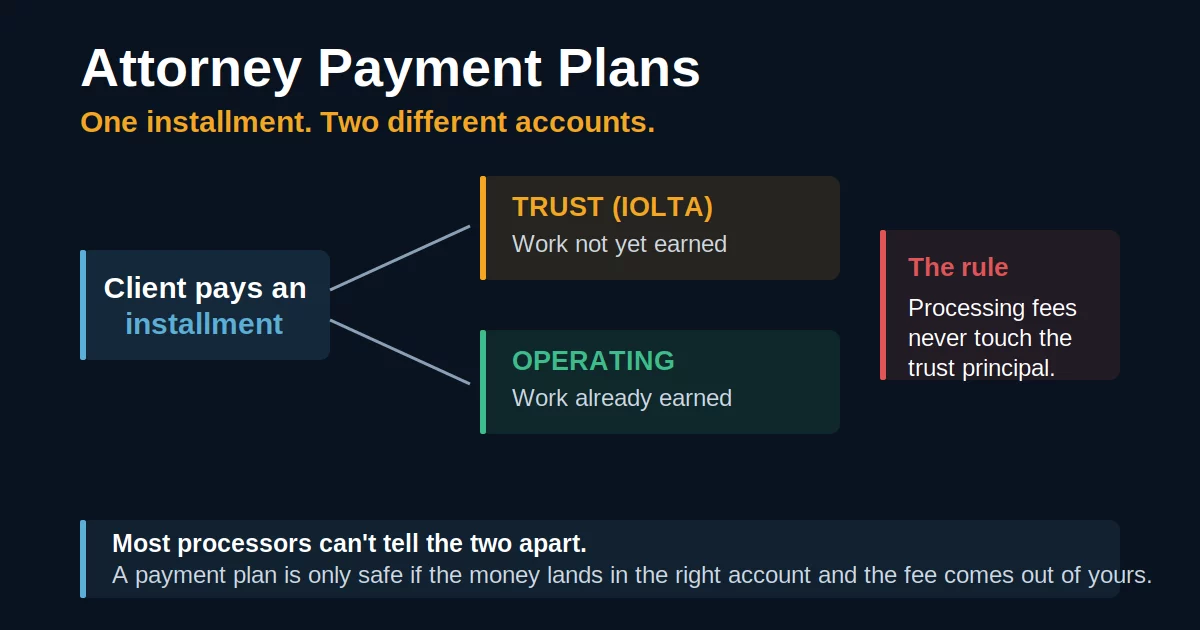

One Installment, Two Possible Accounts

Here is the part generic processing gets wrong. When a client pays toward work you haven’t performed yet, that money isn’t yours — it’s an advance, and in most states it belongs in your client trust account (IOLTA) until it’s earned. When a client pays toward work you’ve already done and billed, that money is earned and belongs in your operating account. A single monthly installment on a long matter can even straddle both.

The American Bar Association’s Formal Opinion 505 made the point sharply: advance fees — including flat fees, however they’re labeled — generally must sit in trust until earned. Some jurisdictions let a flat fee be earned in stages tied to milestones, but the default in most is trust-until-earned.

Depositing unearned installments straight into operating is commingling, and taking unearned fees is the single largest source of client-protection-fund claims. Attorney payment plans that dump every charge into one account — the way an ordinary merchant account does — quietly manufacture that violation month after month.

Processing Fees Can Never Come Out of Trust

Even when an installment correctly lands in trust, the card or ACH processing fee attached to it cannot be paid from the trust principal — that’s the client’s money, and skimming a fee from it is a trust violation on its own. A payment plan running on a generic processor typically nets the fee out of the deposit automatically, which is exactly the wrong behavior for a trust deposit.

Firms often ask whether they can pass the card fee to the client on a payment plan. On the operating side you may be able to, subject to your state’s surcharge rules, the card-brand caps, and clear disclosure — see credit card surcharge legality. On the trust side it’s far murkier, because you can’t move the client’s own money to cover a fee on the client’s own deposit. The clean answer is a processor that debits the fee from operating, never from trust.

What Attorney Payment Plans Should Run On

A payment plan is only as safe as the plumbing under it. Three requirements separate a compliant setup from a disciplinary complaint waiting to happen:

The processor must route each installment to trust or operating based on whether the fee is earned, and it must never draw the processing cost from the trust account. This is the non-negotiable one, and it’s why a legal-specific setup beats a generic merchant account for a firm running plans.

Installments repeat, so the rate compounds. Interchange-plus pricing keeps the recurring card cost honest, and routing a plan through ACH where appropriate lowers it further on the larger schedules.

A stored card that expires mid-plan breaks the schedule and sends a matter to collections that shouldn’t be there. An account updater keeps the installment running when a card is reissued — the same retention tool a recurring business relies on, applied to a fee schedule.

Set up this way, attorney payment plans do what they’re supposed to: widen access for clients, steady the firm’s cash flow, and keep every dollar in the account the rules require — without turning the intake conversation into a compliance risk.

Frequently Asked Questions

It depends on whether the fee is earned. An installment paying for work not yet performed is an advance and generally belongs in the client trust account until earned; an installment paying for work already done and billed belongs in operating. Your state’s rules and your fee agreement govern the details.

You cannot pay a processing fee out of the trust principal — that’s the client’s money. The fee must come from your operating account. A legal-specific processor debits fees from operating and never nets them out of a trust deposit, which is the safe configuration.

No — though people use the terms loosely, and both show up under attorney payment plans. In a direct plan the firm charges the client on a schedule and carries the risk, usually interest-free. In financing, a third-party lender pays the firm upfront and the client repays the lender with interest. Both are useful; they solve different cash-flow problems.

More on Law Firm Payments

Send One Statement. We’ll Check Where Every Installment Lands.

Send Brookside one recent processing statement and we’ll check whether your plan installments and fees are routing to trust and operating correctly, and show you your true rate on the recurring charges. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for Free ReviewNo obligation • No pressure • Response within one business day