What Are Credit Card Assessment Fees — And Why You Cannot Negotiate Them

Most merchants reviewing a processing statement for the first time can identify the interchange line. They can identify the processor’s discount rate. The line that almost nobody can identify — and the one your processor will not explain unless you ask — is the credit card assessment fees line. And it appears every single month.

Credit card assessment fees are charges paid directly to Visa, Mastercard, Discover, and American Express for the use of their networks. They are pass-through fees, set by the card brands, collected by your processor, and paid to the networks. They are not interchange. They are not your processor’s markup. And they cannot be negotiated.

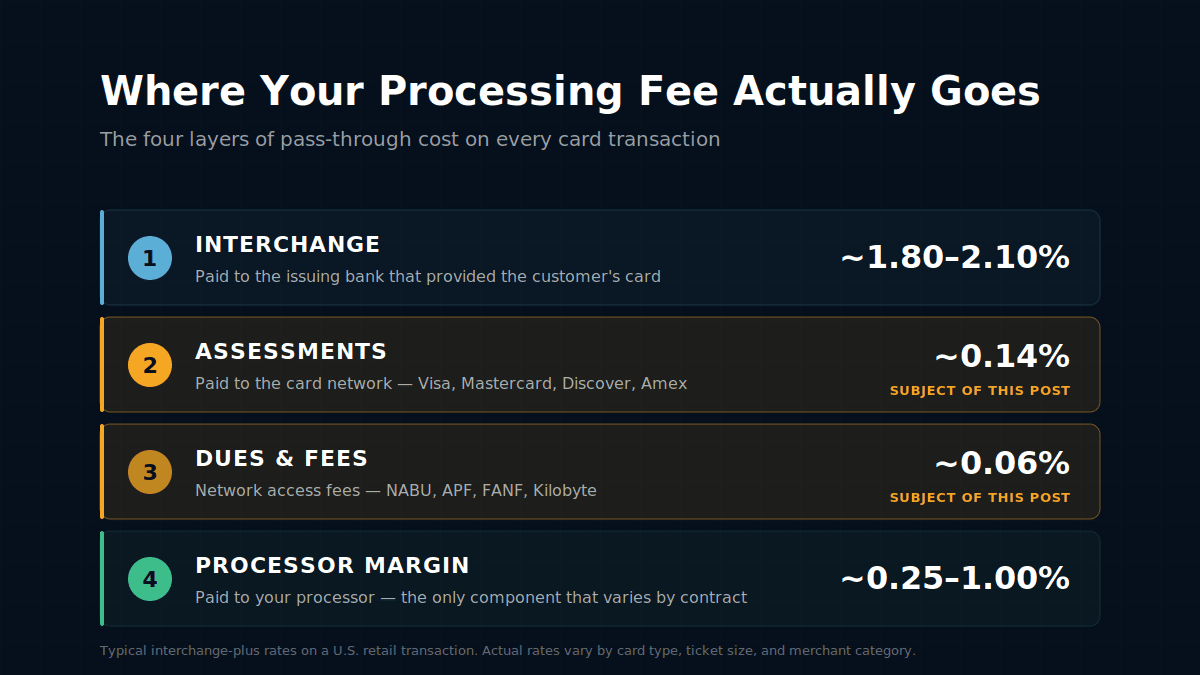

The image above shows where every layer of your processing fee actually goes. Interchange — paid to the issuing bank — is the largest portion. Assessments and dues & fees together are smaller in raw percentage but together account for roughly 8% of your total processing cost on a typical retail transaction. The only layer your processor controls is the margin in the fourth row.

What Credit Card Assessment Fees Actually Are

An assessment fee is a percentage of card transaction volume that the card network charges for using its rails. The fee gets calculated on every dollar processed and added to your monthly bill as a separate line item — assuming your processor is on interchange-plus pricing. On flat-rate or tiered pricing, the assessment is bundled into the larger rate and never broken out.

The “assessment” by itself is a percentage of volume. But the industry term often gets used loosely to cover a broader category — what statements label “Dues & Assessments” or “Card Brand Fees” — that also includes per-transaction network fees. These charges, sometimes called card brand fees on processing statements, all go to the card networks. All are non-negotiable. All are separate from the interchange your issuing bank receives.

The most useful way to think about them: they are the second of three pass-through layers on every card transaction. Interchange is the first (paid to the issuing bank). Assessments and dues & fees are the second (paid to the card networks). Your processor’s margin is the only layer that is not pass-through.

Current Assessment Rates by Card Network (2026)

Each network publishes its own assessment schedule. The numbers below reflect U.S. domestic rates as of April 2026. International transactions, business cards, and prepaid products carry separate surcharges that are not covered here.

The Visa assessment fee is 0.14% on credit card volume and 0.13% on debit card volume. Applied to every transaction processed on a Visa-branded card issued in the United States.

The Mastercard assessment fee is 0.1275% on transactions under $1,000 and 0.1475% on transactions of $1,000 or more. The break point is per transaction, not per merchant — so a single $1,200 ticket gets the higher rate even if your average ticket is $40.

0.13% on credit card volume. Applied as a single rate without the under/over $1,000 split that Mastercard uses.

0.15% on credit card volume for merchants on the OptBlue program. Direct Amex contracts (negotiated separately with American Express) operate on a different fee schedule.

If you process roughly $50,000 a month with a typical U.S. small business card mix — 70% Visa/Mastercard credit, 20% debit, 10% Amex/Discover — your monthly assessments alone come to roughly $70 to $80. Spread across the year, that is just under $1,000 in pure pass-through cost to the card networks before any other fee or markup is applied.

Dues and Fees — The Layer Most Merchants Miss

Beyond the percentage assessments, each network charges a series of small per-transaction fees for network access and authorization handling. These are commonly grouped under “Dues & Fees” on statements. Four show up on virtually every U.S. merchant statement:

The NABU fee is $0.0195 per authorization. Charged on every Mastercard transaction submitted for authorization, whether it ultimately settles or not. NABU is sometimes labeled simply as “network access fee” on statements.

The APF fee is $0.0195 per credit authorization and $0.0155 per debit authorization. Charged on every Visa transaction submitted for authorization, even if the transaction is later declined or voided.

A monthly fee that varies by merchant tier — typically $55 to $70 per location for small retail, higher for card-not-present and larger volume merchants. Billed quarterly, which is why it sometimes seems to disappear and reappear.

Visa charges $0.0047 per transaction; Mastercard charges $0.0035. The fee covers transmission of authorization and clearing data through the network.

None of these are large in isolation. On a small merchant doing 1,000 transactions a month, NABU and APF together come to roughly $39. FANF adds another $55 to $70. Kilobyte fees add another $4 to $5. The full per-transaction stack lands around $100 to $115 per month for that merchant — money that goes to the networks regardless of who processes their cards.

How Credit Card Assessment Fees Appear on Your Statement

What you see depends entirely on your pricing model.

Assessments and dues & fees appear as separate line items. You will see “Visa Assessment,” “Mastercard Assessment,” “NABU,” “APF,” “FANF,” and “Kilobyte” or “Settlement Network Access” as distinct entries. Each shows the rate or per-transaction amount and the resulting charge for the period. This is the only model where you can verify the network is getting paid what they actually charge.

On Square, Stripe, PayPal, and the bundled-rate side of Clover, assessments do not appear anywhere. They are absorbed into the single advertised rate — the 2.6% + 10¢ or 2.9% + 30¢ that gets charged on every transaction. You are still paying them. You just cannot see them or verify them.

Qualified, mid-qualified, and non-qualified tier rates may show a small assessment line under each tier, may bundle assessments into the tier rates, or may show only an aggregated “Dues & Assessments” number that combines several different fees. The lack of visibility on tiered pricing is the same problem flat-rate has, just dressed in different clothes.

The single most useful diagnostic on any statement: scan for the line items “Visa Assessment,” “Mastercard Assessment,” and “NABU.” If they are missing entirely, your pricing is bundled and your effective rate is being inflated. If they are present but at rates significantly higher than the published numbers above, your processor is padding pass-through fees — a common practice with no recourse other than to reduce processing rate by switching to a transparent processor.

The One Thing About These Fees That Actually Helps You

The card networks set assessment rates. Visa publishes its rates and updates them in October each year. Mastercard publishes its rates and updates them in April and October. Discover and Amex publish on their own schedules — and for AmEx specifically, the dynamics around OptBlue versus direct AmEx further complicate where the line between assessment and processor markup falls. Acquirers (the entities that contract with merchants) collect the fees on behalf of the networks and remit them. There is no negotiation step in this chain. Your processor cannot waive a Visa assessment fee any more than your bank can waive a Federal Reserve fee.

This is structurally the same situation as interchange — the issuing bank fee that gets the most attention. Both interchange and assessments are network-set, non-negotiable, and identical across processors. Statements just make them look different because some processors bundle them and some pass them through. According to the Federal Reserve’s interchange fee revenue data, this pass-through structure is a permanent feature of the U.S. payment system, not a negotiation lever.

Because assessment fees are identical across every processor, the only variable in your processing cost that anyone can negotiate is the processor’s margin. That single layer — typically 0.25% to 1.00% — is where every cost reduction conversation should start. The assessments are constant. The interchange is constant. The processor margin is the entire game.

What Credit Card Assessment Fees Do to Your Effective Rate

Assessments and dues & fees together typically add 0.18% to 0.22% to your effective rate, plus another $30 to $80 per month in flat per-transaction and monthly fees. On a merchant processing $50,000 a month at a typical retail card mix, that is around $115 to $130 in pure network pass-through cost — money that would be paid regardless of whether the processor is Square, Stripe, Brookside, or anyone else.

Visa + Mastercard + Discover assessments on $50,000 of mixed-network volume: roughly $70. NABU + APF on 1,000 transactions: $39. FANF: $55–$70. Kilobyte: $4–$5. Total network pass-through: roughly $168 to $184 per month, or 0.34%–0.37% of volume. That is the floor every processor charges before any margin is added.

The reason this number matters: when comparing two processor quotes, you cannot meaningfully compare advertised rates without first stripping out the pass-through layer. A processor advertising “2.6% flat” is bundling around 0.20% of pass-through cost into that number. A processor advertising “interchange + 0.30%” is showing you the assessment line separately. Same total cost, completely different visibility.

To calculate your own effective rate, divide total monthly fees by total card volume, then multiply by 100. Anything above 2.50% on standard retail mix means there is room. The effective rate guide walks through the calculation step by step.

Frequently Asked Questions

No. Interchange fees are paid to the issuing bank — the bank that gave the customer their credit card. Assessment fees are paid to the card network — Visa, Mastercard, Discover, or American Express. Both are pass-through costs, but they go to different parties and serve different purposes.

No. Assessment fees are set by the card networks and are identical across every processor. Any processor that claims they can lower your assessment fee is either confused about terminology or being misleading — what they can lower is their own margin, not the network’s pass-through cost.

Flat-rate processors bundle assessments, dues & fees, and interchange into a single advertised rate (such as 2.6% + 10¢). You are still paying the assessments — they are simply absorbed into the larger number rather than displayed as a separate line item. The only way to see assessments broken out is on interchange-plus pricing.

Yes, and it happens regularly. Because the published rates are the wholesale cost from the network, a processor on interchange-plus can charge a higher rate on the assessment line and pocket the difference. The fix is to compare the assessment lines on your statement against the published rates — 0.14% for Visa credit and 0.1275% to 0.1475% for Mastercard. Anything materially above those is padding.

Yes, at slightly different rates. Visa charges 0.13% on debit volume versus 0.14% on credit. Mastercard charges the same percentage on debit and credit at the same volume tier. Per-transaction fees like NABU and APF apply to both credit and debit transactions.

More on Processing Fees and Statement Analysis

If you can identify your assessment fees, you can spot the padding

Send us your most recent processing statement and we will tell you exactly what your processor is charging at the network pass-through line — and what is being added to it.

Get Your Free Statement ReviewNo obligation • No pressure • Response within one business day