The Visa Level 2 Sunset Was April 17. Most B2B Merchants Have Not Been Told.

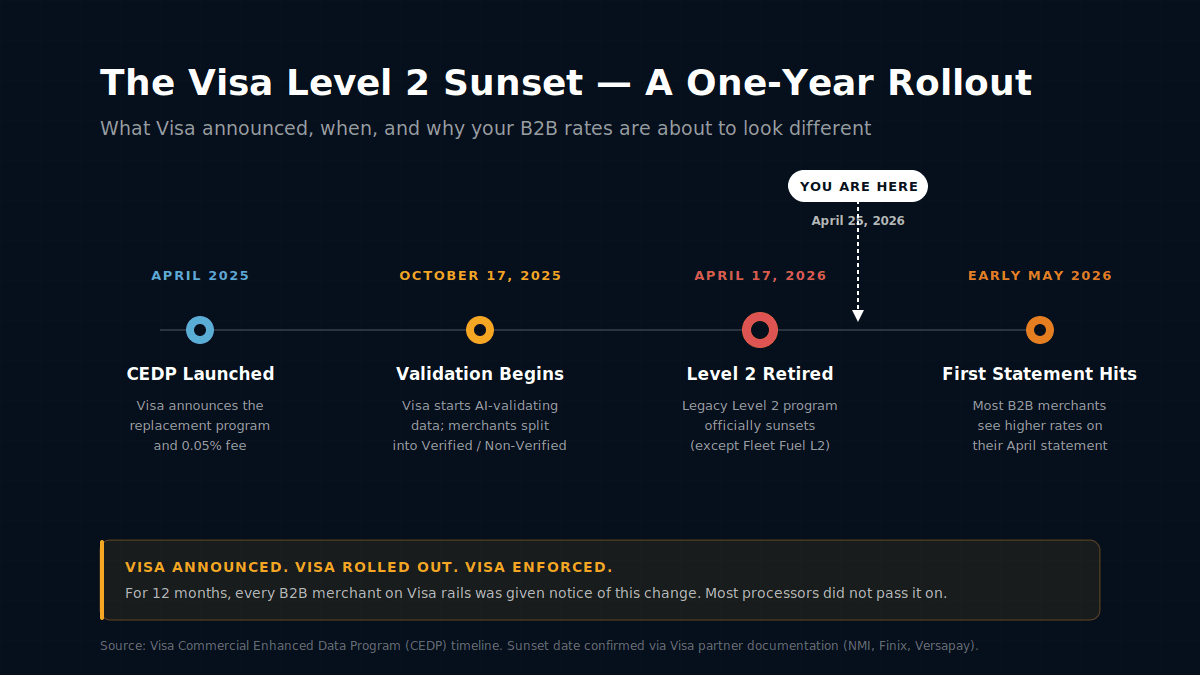

On April 17, 2026, Visa officially retired its Level 2 interchange program. The Visa Level 2 sunset ended a B2B savings tool that thousands of contractors, wholesalers, professional service firms, and government suppliers had relied on for over a decade. It was announced a year in advance. It was rolled out in phases. And most merchants who are about to be affected have not been told it happened.

The first statement reflecting the change will arrive in early May. By then, B2B merchants who were qualifying for Level 2 discounts will see their commercial card transactions priced at higher rates — the difference often running 50 to 100 basis points per transaction. On a contractor processing $80,000 a month in card volume, that is roughly $400 to $800 a month, every month, with no warning.

Here is what changed, why your processor probably did not mention it, and what to do before the next billing cycle.

What the Visa Level 2 Sunset Eliminated — and Why It Mattered

For more than a decade, B2B merchants who processed commercial credit cards (small business cards, corporate cards, government purchasing cards) could qualify for reduced interchange rates by submitting additional transaction data — most commonly a sales tax amount and a customer code. This was Level 2 data. The reduced rates often saved B2B merchants 30 to 75 basis points per transaction on every commercial card swipe.

Level 3 data went further — line-item details including SKUs, quantities, unit costs, and freight charges — and unlocked the lowest available B2B interchange rates. Level 3 was harder to set up but produced bigger savings, especially on large-ticket transactions.

The system worked like this: the more structured data you sent with each commercial card transaction, the lower your interchange. Level 1 was basic transaction data (no discount). Level 2 added tax and customer code (modest discount). Level 3 added line-item invoice detail (largest discount). Most B2B merchants ended up at Level 2 — because Level 3 required tighter integration with their accounting or ERP system, and most processors made Level 2 the default path.

What Replaces Level 2 — CEDP and Product 3

Visa is replacing the Level 2 / Level 3 system with a single program called the Commercial Enhanced Data Program (CEDP). Under CEDP, the only path to discounted B2B interchange rates is a new category called Visa Product 3 interchange — and Product 3 has substantially stricter requirements than the Level 2 program it is replacing.

Three things changed:

Under the old Level 2, processors only checked whether required fields were present. Under CEDP, Visa runs every transaction through an AI validation algorithm that checks whether the data is actually accurate and complete. Placeholder values like “9999” for tax (a known industry workaround) no longer qualify. The data has to be real.

Visa now grades every B2B merchant on the quality of the data they submit. A Visa Verified Merchant — one who consistently submits accurate, complete, validated data — qualifies for the lowest Product 3 interchange rates. A Non-Verified merchant pays standard commercial card rates, which can be 50 to 100 basis points higher. Most merchants started in Non-Verified status by default on April 17.

Acquirers participating in CEDP are charged a 0.05% fee on each qualifying transaction. This fee is typically passed through to the merchant. Even merchants who qualify for Product 3 rates pay this 5-basis-point participation fee on top of the discounted interchange — though the savings still net out positive for fully Verified merchants.

The structural change is not subtle. The bar for B2B interchange savings just got significantly higher — and most merchants have not adjusted their data flow to clear it.

What the Visa Level 2 Sunset Means for Your B2B Rates

The financial impact splits cleanly along the Verified / Non-Verified line. There is no middle ground.

B2B merchants who were already submitting Level 3 data and pass Visa’s accuracy validation may actually save money. Product 3 rates are slightly lower than the old Level 3 rates for some categories, and Business Credit cards (small business cards) are now eligible for Product 3 — a category they could not access under the old system. Net effect for fully Verified merchants is typically a small improvement, partially offset by the 0.05% participation fee.

B2B merchants who relied on Level 2 — the simpler tier requiring only tax and customer code — and have not upgraded to full Product 3 data submission now pay standard commercial card interchange. The difference is typically 50 to 100 basis points per transaction. On a contractor processing $80,000 monthly in B2B volume, the rate increase translates to roughly $400 to $800 per month — $4,800 to $9,600 per year — every year going forward.

Under CEDP, transactions that initially qualify for Product 3 can be downgraded retroactively if Visa’s validation later flags the data as inaccurate. These adjustments typically appear 10 to 15 days after the original transaction. Merchants may see surprise debits on statements weeks after the fact, with no clear explanation unless they know to look for it.

How to Tell if You Are Affected by the Visa Level 2 Sunset

Three quick checks will tell you whether your business is going to feel the change. If your business does not accept commercial cards from other businesses (B2B), you are not affected. If you do, run through these:

If any of these checks turn up red, the May statement will show the impact. The cleanest way to see the actual dollar difference is to calculate your effective rate from your March statement (pre-sunset) and your May statement (post-sunset) — the gap is the cost of the change.

The Three Actions That Restore B2B Interchange Rates

The fix for B2B interchange changes 2026 is not complicated, but it does require coordination between your processor, your gateway, and your accounting system. Three steps cover most merchants.

Identify what data your current setup actually sends to the network on each B2B transaction. If your gateway or ERP integration uses placeholder values to “qualify” for Level 2 — a common practice for years — those workarounds will not pass CEDP validation. The data has to be accurate or it does not count.

Major gateways have rolled out CEDP-compliant features — tax field validation, line-item template support, AI pre-validation that flags data errors before they hit Visa’s network. If your gateway has not been updated for CEDP, no amount of merchant-side data quality will help. Your processor should know whether your gateway is current.

Verified status is earned over time — Visa reviews data quality monthly. Even with all systems in place, it can take 30 days of clean transactions to get verified. Start sending accurate data now and the May statement may not be perfect, but the June statement will reflect the improved status.

For B2B merchants in contracting and trade industries — the heaviest commercial card users — the work pays back fast. A typical commercial HVAC, electrical, or plumbing contractor running $50,000 to $150,000 per month in B2B volume saves $3,000 to $18,000 per year by maintaining Verified status under Product 3 versus paying Non-Verified rates.

The Question Worth Asking Your Processor

Visa announced CEDP in October 2024. The replacement program launched in April 2025. Validation began October 17, 2025. The Visa Level 2 retirement was scheduled and confirmed publicly at every step. None of this was a surprise to anyone in the payments industry. According to the Federal Reserve’s interchange fee revenue data, B2B card volume is one of the largest segments of commercial card processing — meaning every processor with B2B merchants on their book had clear advance notice of who would be affected.

The processors knew. Their compliance teams knew. Their pricing analysts knew. The question worth asking is why most of them did not write to their B2B merchants saying “this is happening, here is what to do, here is whether your account is ready.”

The answer is consistent across the industry: a non-trivial number of processors quietly benefit from rate increases. When network costs go up, the increase passes through to the merchant. When the merchant does not know why, there is no negotiation. When the merchant does not know it happened, there is no churn. The Visa Level 2 sunsetting was a textbook case of this dynamic — a major change that disadvantages merchants by default, with a path to remediation that requires the merchant to push for it.

If you have noticed your processing rates rising recently without any explanation from your processor, the May statement will probably make it explicit. The line items on a CEDP-impacted statement are different from the ones that came before. If that conversation does not happen, then it is worth asking why — and what else is going unsaid.

There is a structural option the Level 2 sunset does not touch: moving B2B payments off cards entirely. ACH bank transfers carry no interchange at all — no Level 2, no Level 3, no CEDP qualification to chase. For B2B merchants whose customers are other businesses paying invoices, collecting by ACH sidesteps the entire interchange-tier problem. ACH B2B volume grew 11.6% in 2024 as more firms made exactly this shift. It will not fit every transaction, but for recurring or invoiced B2B revenue it is worth evaluating alongside interchange optimization. The other temptation — passing the higher cost on as a surcharge — backfires with B2B buyers more often than retail; here is why a B2B surcharge can cost you the account. Why your B2B clients shouldn’t pay by credit card walks through the full cost-gap math.

Frequently Asked Questions

Yes. Effective April 17, 2026, the Visa Level 2 interchange program is officially sunset for all categories except Fleet Fuel. Visa announced the change in October 2024, launched the replacement (CEDP) in April 2025, and began full validation in October 2025. The sunset is documented in Visa’s published partner guidance and confirmed by all major processors.

The Commercial Enhanced Data Program (CEDP) and a new interchange category called Product 3. Product 3 offers similar or slightly lower rates than the old Level 3 program, but requires AI-validated invoice-quality data on every transaction. Merchants are classified as Verified or Non-Verified, and only Verified merchants qualify for the discounted Product 3 rates.

For B2B merchants who were qualifying under Level 2 and are not yet submitting full Product 3 data, the typical rate increase is 50 to 100 basis points per commercial card transaction. On $80,000 of monthly B2B card volume, that is roughly $400 to $800 per month going forward. The first statement reflecting the change arrives in early May 2026.

Only if your data is accurate and complete on every transaction. Verified status is earned, not assigned — Visa reviews each merchant’s data quality monthly. Most merchants need a CEDP-ready gateway, an updated point-of-sale or virtual terminal, and disciplined data entry to stay verified. The classification can take 30 days of clean transactions to achieve.

Fleet Fuel transactions retain a legacy Level 2 fee category and are not affected by the April 17 sunset. All other commercial card transactions — small business, corporate, purchasing, government — fall under the new CEDP / Product 3 framework.

More on B2B Interchange and Statement Review

If your B2B rates went up last week, your May statement will show it

Send us your March statement and your May statement when it arrives. We will identify the exact rate categories that changed, calculate what the Visa Level 2 sunset cost you, and show you what it would take to get classified as a Verified Merchant under Product 3.

Get Your Free Statement ReviewNo obligation • No pressure • Response within one business day