Pre-Need Funeral Payment Processing: Fees You Can’t Recoup

Pre-Need Funeral Payment Processing: You’re Paying Card Fees on Money You Can’t Keep

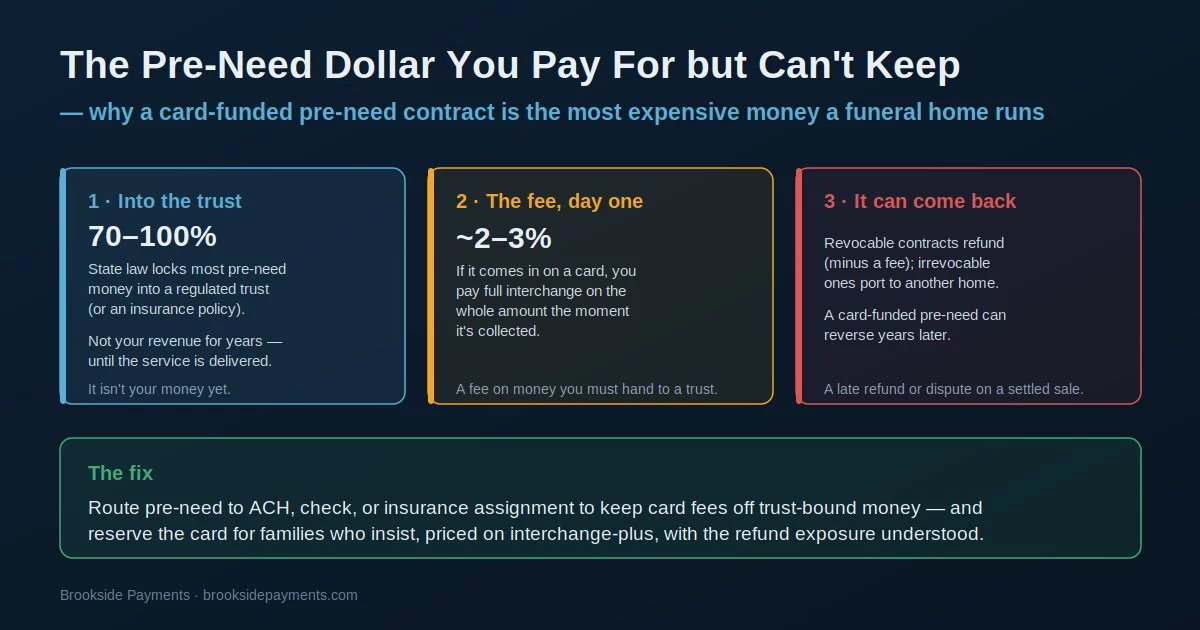

Pre-need funeral payment processing is the one place in the business where the money you collect today isn’t really yours. When a family pre-pays for a funeral, state law usually requires most of that money to be deposited into a regulated trust or used to fund an insurance policy — and you won’t recognize it as revenue until you actually deliver the service, which can be years or decades away. Yet if that payment comes in on a credit card, you pay full interchange on the entire amount the moment it’s collected. You’ve paid a percentage on dollars you have to hand to a trust and can’t touch.

That alone makes pre-need funeral payment processing more expensive than the at-need charge most funeral homes worry about. But the deeper problem is what happens later: pre-need contracts can be cancelled, refunded, or transferred to another funeral home under the law, which means a card-funded pre-need sale isn’t really final the way a retail swipe is. Understanding where the money goes — and how it can come back — is the whole game.

Where Pre-Need Money Actually Goes

In pre-need funeral payment processing, a contract is funded one of two ways, and both put the money out of your reach. The first is a trust: most states require that 70% to 100% of a trust-funded pre-need payment be deposited into a regulated, restricted account, with only a small retainage (where state law allows) kept by the firm up front. The second is insurance: the family buys a policy with the funeral home named as beneficiary, overseen by the state insurance commissioner. Either way, the bulk of the money sits in a protected vehicle, earns its own return, and is released only when the service is provided.

This is what makes pre-need funeral payment processing structurally different from any other sale you run. In retail, you swipe a card and the money is yours minus the fee. In pre-need, you swipe a card, pay the full ~2-3% interchange on the whole amount, and then deposit most of that money into a trust you can’t draw on for years. The fee is real and immediate; the revenue is deferred and restricted. A blended processing rate makes this invisible — it treats a trust-bound pre-need deposit exactly like an at-need charge you get to keep, when economically they are nothing alike.

If your state requires 100% of a pre-need payment into trust and a family pays $10,000 by card, you pay roughly $200-300 in interchange and deposit the full $10,000 into the trust. You’re out the fee on money that won’t be yours for years. Routing that payment to ACH, check, or insurance assignment instead keeps the card cost off funds you legally can’t keep — the single highest-leverage decision in pre-need funeral payment processing.

A Card-Funded Pre-Need Can Come Back Years Later

Here is the part of pre-need funeral payment processing that almost no one prices in. A pre-need contract is not a final sale — the law builds in several ways for the money to come back, and each one is a problem if the contract was funded by card. Every pre-need contract can be cancelled within a short window (commonly seven days) for a full refund. After that, a revocable contract can still be cancelled and refunded, though the firm may keep a cancellation fee (often 10-20%) where state law permits. An irrevocable contract — the kind used for Medicaid spend-down — generally can’t be cancelled for a refund, but it remains portable: if the family moves or changes their mind, you must transfer the trust funds to the new funeral home, often within about ten business days.

Now layer the card on top. If a pre-need was paid by credit card and the family later cancels or transfers, you have to refund or release the principal — but the interchange you paid at the time of sale is gone and isn’t coming back. Worse, if the family disputes the charge instead of requesting a refund, you can face a chargeback on a transaction that settled years ago, long past the point where you have easy records to defend it. A card-funded pre-need carries a delayed-reversal exposure that an ACH or insurance-funded one largely doesn’t — another reason pre-need funeral payment processing rewards routing the money to the right rail from the start.

A retail card sale is final in days. A pre-need card sale can be unwound months or years later through a cancellation, a refund, or a portability transfer — and you keep none of the interchange you paid up front. If it returns as a dispute rather than a refund request, you’re defending an ancient transaction. ACH, check, and insurance assignment don’t carry this long tail; that’s a real reason to steer the big pre-need balance away from cards.

Pre-Need Paid Over Time Is Recurring Card Billing

Many families don’t fund a pre-need contract in a single payment — they pay it off over months or years. That turns pre-need funeral payment processing into a recurring-billing operation, with all the plumbing that implies. Every installment carries its own card fee, so the cumulative interchange on a multi-year payment plan is larger than a one-time charge would have been. Cards on file expire and get reissued, so without an account-updater service you get failed payments that interrupt the schedule. And a missed installment on a future-delivery obligation is a dunning problem, not just a bookkeeping one.

None of this is a reason to avoid installment pre-need — payment plans are how many families can afford to plan ahead at all. It’s a reason to treat installment pre-need funeral payment processing as recurring billing and run those plans on tooling built for it: a real recurring engine, an account updater to catch reissued cards, and clean billing descriptors so a family recognizes the charge and doesn’t dispute it. Steering the recurring portion to ACH, where the per-payment cost is far lower and cards-expiring isn’t an issue, is often the cleanest answer.

A $9,000 pre-need paid in 36 monthly card installments pays interchange 36 times, not once — and each reissued or expired card is a failed payment to chase. Recurring pre-need belongs on an account-updater-equipped recurring engine or, better for the per-payment math, on ACH. A flat aggregator gives you neither the updater nor the descriptor control to keep disputes down.

Route Pre-Need by How the Law Treats the Money

The lever in pre-need funeral payment processing isn’t a renegotiated swipe rate — it’s matching each payment to the rail that fits how the money is treated. Three moves do most of the work.

- Steer the trust-bound balance off cards — route the large pre-need payment to ACH, check, or insurance assignment so you’re not paying interchange on money headed straight into a regulated trust you can’t keep.

- Run installment plans on recurring tooling — an account updater for reissued cards, clean descriptors to prevent disputes, and ACH where the per-payment cost and reliability beat a card.

- Separate pre-need from at-need in your processing — so you can see the cost of each, and price the card path on interchange-plus for the families who genuinely want to use a card, with the refund and portability exposure understood up front.

Pre-need funeral payment processing rewards a firm that treats the payment method as a legal-and-financial decision, not a convenience default. The money is going into a trust, it may come back, and the card fee is real today — so route it like it matters, because it does. This sits underneath the broader picture in funeral home payment processing, where the at-need charge and the software-bundled processor are the other two costs a blended rate hides.

Frequently Asked Questions

With an at-need charge you keep the money now. With pre-need you pay full interchange on the whole amount, then most states require most of it to be deposited into a regulated trust you can’t keep or recognize as revenue until the service is delivered — often years later. You’ve paid a percentage on dollars that aren’t yet yours. Routing pre-need funeral payment processing to ACH or insurance assignment keeps that card cost off trust-bound funds.

Often, yes — which is the risk. Any pre-need contract can usually be cancelled within a short window (commonly seven days). A revocable contract can be cancelled and refunded after that, though a cancellation fee may apply where state law permits; an irrevocable one generally can’t be refunded but stays portable to another funeral home. In every case you keep none of the interchange you paid up front, and a dispute on an old card sale is far harder to defend than a current one.

You can, but route the large trust-bound balance to ACH, check, or insurance assignment wherever you can, and reserve the card for families who genuinely want the convenience. If a family does pay by card, price that path on interchange-plus rather than a blended rate, run any installments on recurring tooling with an account updater, and understand the refund and portability exposure before you treat the sale as final — the habits that make pre-need funeral payment processing pay off.

Keep reading on funeral payments, funding timing, and routing

Send Your Statement. We’ll Show You What Pre-Need Cards Are Really Costing.

If you collect pre-need on a card, or run installment plans on a blended rate, send Brookside one recent statement. We’ll separate your pre-need and at-need processing, show you what you’re paying in card fees on trust-bound money, and lay out where to route it instead. The review takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day