Med Spa Payment Processing: Coded Wrong, Frozen Later

Med Spa Payment Processing Isn’t a Salon Problem or a Doctor’s-Office Problem

Med spa payment processing is hard for one reason: a med spa lives between two worlds the card industry treats very differently. Half of what you do looks like a salon — facials, peels, retail skincare, memberships — and half looks like a medical practice — injectables, lasers, weight-loss protocols delivered by licensed staff. Your processor has to pick a lane for you, and the lane it picks decides your rates, your reserves, and whether your account is still open in six months. The cost in med spa payment processing isn’t a tenth of a percent on the swipe; it’s being boarded wrong and finding out the hard way.

That’s what makes this different from a hair salon down the street. A salon’s payments are small, uniform, and low-risk. A med spa runs $500 to $3,000 charges for Botox, filler, and laser, sells prepaid packages and monthly memberships, and increasingly offers weight-loss injections — and every one of those is a reason a generic, flat-rate processor either overcharges you or freezes you — the two failure modes med spa payment processing has to design around.

The MCC You’re Boarded Under Decides Everything

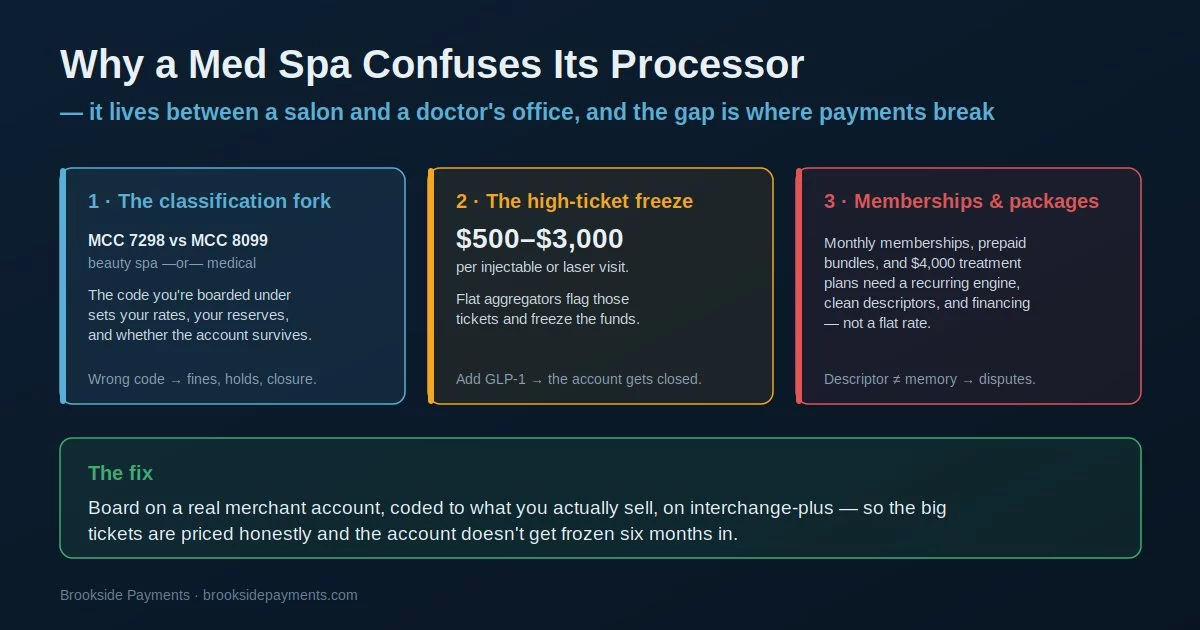

Every merchant account is assigned a four-digit Merchant Category Code, and for a med spa the code is a fork in the road. Boarded as a beauty and health spa, you fall under MCC 7298 — the same family as salons and day spas, treated as ordinary retail-service risk. Boarded as a medical practice, you fall under MCC 8099, “Health Practitioners, Medical Services — Not Elsewhere Classified,” a catch-all that many processors treat as high-risk, with rolling reserves, monthly minimums, and longer-term contracts attached. The acquirer makes the call at boarding, and it drives your interchange, your risk profile, and whether the account is stable — which makes the MCC the most consequential decision in med spa payment processing.

The trap is that the wrong code doesn’t fail loudly on day one. It fails later. A med spa boarded as a plain beauty spa that then starts billing injectables, GLP-1 weight-loss shots, peptides, or hormone protocols is now processing medical services under a retail code — and when that mismatch surfaces, it can mean card-brand fines, fund holds, or termination. The right move in med spa payment processing is to be coded for what you actually sell from the start, which sometimes means a healthcare merchant account rather than a salon one. If licensed medical or nurse practitioners perform procedures and you keep clinical records, parts of your operation may fall under healthcare-processing and HIPAA-aware handling rules; if you’re purely aesthetic and retail, a salon-style account may fit. The service mix and the licensing decide.

Your category code isn’t a label — it sets the interchange your cards run at, the reserve a processor may hold, the underwriting scrutiny you face, and the card-brand rules you’re measured against. A med spa coded as a beauty spa to win a cheaper rate looks fine until medical-service volume shows up and the account is reclassified, frozen, or closed. Coded correctly, the same business is simply priced for what it is.

Why Square and Stripe Freeze Med Spa Money

Flat-rate aggregators are built for a world of small, uniform transactions — a coffee, a haircut, a $40 retail sale. A med spa breaks that model the moment it runs a $2,000 laser package or a $3,000 filler appointment. Large, irregular tickets are exactly what an aggregator’s automated risk engine is trained to flag, and the response is often a hold on the funds while it investigates — your money, parked, at the worst possible time for cash flow. This is the single most common complaint in med spa payment processing: not the rate, but the held deposit.

It gets sharper with medical-aesthetic services. When weight-loss injections, peptides, or hormone protocols start showing up in a flat aggregator’s transaction history, many of them don’t just hold funds — they offboard the account entirely, because those services sit outside what the aggregator agreed to support. A salon can live on a flat aggregator forever; a med spa that grows into injectables and GLP-1 is on borrowed time there. The fix isn’t a better aggregator — it’s a real merchant account with an underwriter who expects high tickets and medical-aesthetic services and prices the account for them up front — the foundation of stable med spa payment processing.

On a flat aggregator, a $3,000 charge isn’t just expensive — it’s a flag. Aggregators approve businesses in bulk with little underwriting, so they manage risk after the fact by freezing or dropping accounts that don’t fit the average. A med spa’s whole economics — big tickets, medical services, packages — is the profile that triggers that reaction. A properly underwritten merchant account absorbs it because it was approved knowing exactly what you sell.

Recurring Billing and Five-Figure Tickets Need Their Own Plumbing

The revenue model of a modern med spa puts a second strain on med spa payment processing: it is built on things a flat rate handles badly. Monthly memberships, prepaid treatment packages, and auto-renewing bundles are recurring billing, and recurring billing lives or dies on two unglamorous details: a recurring engine that actually rebills on schedule, and a billing descriptor that matches what the patient remembers buying. When a member sees a charge on their statement they don’t recognize — because the descriptor reads as a holding-company name instead of your med spa — they dispute it on reflex, and a chargeback is far more expensive than the membership was worth. Clean descriptors and clear cancellation terms are dispute prevention, not paperwork.

The other half is the five-figure treatment plan. A $4,000 course of treatments is more than many patients will put on a card at once, which is why patient financing — Cherry, CareCredit, and Allē’s plans among them — has become standard in med spa payment processing. These services approve the patient, pay your practice upfront, and carry the repayment relationship themselves, which does two useful things: it moves the large charge off your own processing and risk, and it lifts conversion because the patient pays monthly instead of all at once. Used well, financing is both a sales tool and a way to keep your biggest tickets — and their recurring obligations — from concentrating on your merchant account.

Prepaid packages and memberships generate disputes in two ways: a descriptor the customer doesn’t recognize, and a renewal they forgot they authorized. Both are preventable with a recognizable billing descriptor, written terms at sign-up, and a processor whose recurring tooling lets you document the authorization. The recoverable money here usually dwarfs any rate concession — and a flat aggregator gives you almost nothing to fight a dispute with.

What Actually Makes Med Spa Payments Work

The levers that matter in med spa payment processing aren’t a renegotiated swipe rate. They’re structural: get coded right, get underwritten by someone who expects your business, and route each kind of payment to the path built for it.

- Board on a real med spa merchant account coded to what you sell — not a flat aggregator that approves you in bulk and freezes you later. An underwriter who expects high tickets, injectables, and GLP-1 prices the account for them and doesn’t panic when they appear.

- Price on interchange-plus so your big-ticket charges and your card mix are itemized honestly instead of averaged into a flat number — and so you can read your true effective rate per service type.

- Match the payment to the plumbing — a recurring engine with clean descriptors for memberships and packages, patient financing for five-figure treatment plans, and the right account type (salon vs healthcare) for your services and licensing.

Med spa payment processing is a structure, not a single percentage. The practice that gets the classification right, gets underwritten by a processor that understands aesthetics, and routes memberships and big tickets through the tools built for them almost never has the freeze-and-scramble story — and quietly pays less than the flat aggregator that looked cheaper on day one.

Frequently Asked Questions

It depends on what you actually sell. A purely aesthetic, retail-style spa often fits MCC 7298 (health and beauty spas); once licensed practitioners deliver injectables, lasers, GLP-1, or other medical services, MCC 8099 (medical, not elsewhere classified) is frequently the right home. The acquirer assigns the code, but boarding under the wrong one to win a cheaper rate risks fines, holds, or termination when the mismatch surfaces.

Flat aggregators approve businesses in bulk and manage risk afterward by holding or dropping accounts that don’t fit the average. Large injectable and laser tickets trip their fraud models, and weight-loss or hormone services often fall outside what they support, so the account gets frozen or offboarded. A real merchant account built for med spa payment processing, with med-spa-aware underwriting, is approved knowing those things up front, so it absorbs them instead.

It comes down to your services and licensing. If licensed medical or nurse practitioners perform procedures and you maintain clinical records, parts of your operation may fall under healthcare-processing and HIPAA-aware handling, pointing toward a healthcare merchant account. If you’re aesthetic and retail without those, a salon-style account may be appropriate. Many med spas sit on the line, which is exactly why the account type should be chosen deliberately, not by default.

Keep reading on classification, high tickets, and recurring billing

Send Your Statement. We’ll Tell You How You’re Coded and Where the Risk Is.

If your processor froze a deposit, or you’re not sure whether you’re boarded as a beauty spa or a medical practice, send Brookside one recent statement. We’ll show you your MCC and effective rate, flag where high-ticket and medical-service volume puts your account at risk, and lay out the right structure for your services. The review takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day