Optometry Payment Processing: Retail at a Medical Rate

An Optical Shop Billed at a Medical-Software Rate

Optometry payment processing is unusual because the practice is really two businesses wearing one set of books. There’s the clinical side — the exam, billed to vision and medical plans — and there’s the optical side, a retail store selling frames and lenses at $300, $600, sometimes over $1,000 a pair. Those two halves have completely different payment economics, and most practices run a single bundled rate across both, set by whatever the eyecare software decided to charge.

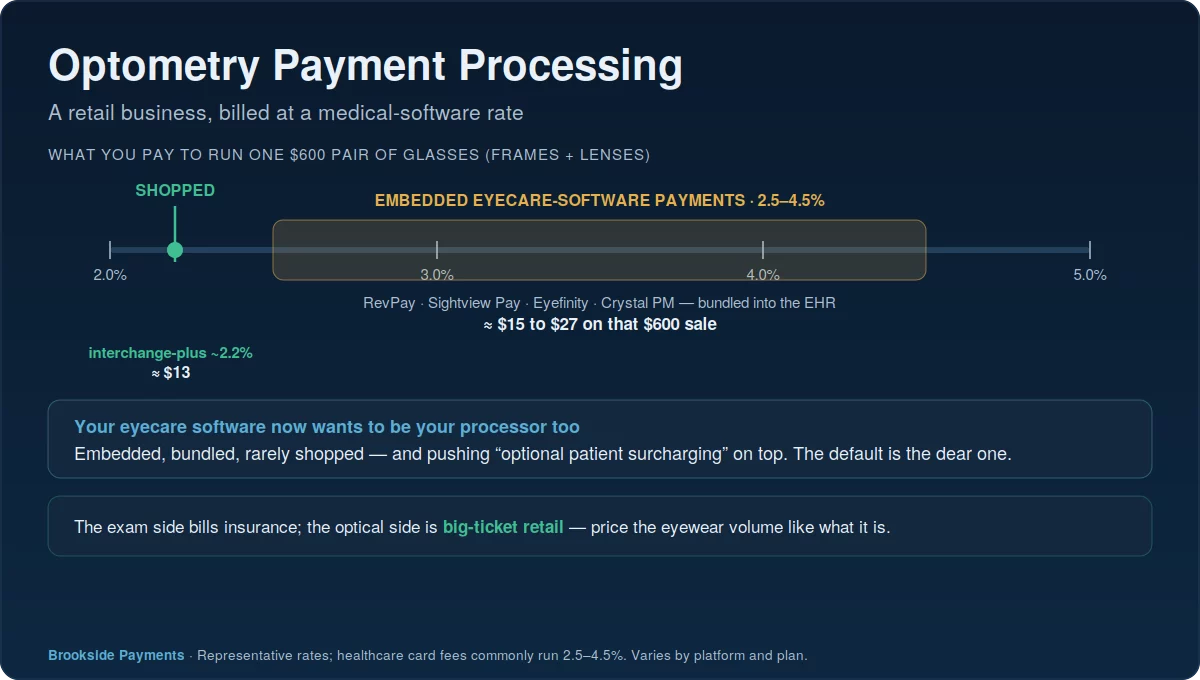

That mismatch is where the money leaks. The optical counter is, for payment purposes, a retail business with big tickets and patient payments — exactly the kind of volume that deserves a sharp, shopped rate. Instead it usually rides the same healthcare-tier processing fee as the rest of the practice, which the industry’s own platforms describe as commonly running 2.5 to 4.5 percent. On a $600 pair of glasses, the gap between that and a shopped rate is real money, repeated at the counter all day. Sorting it out is the heart of optometry payment processing.

The exam is an insurance-billed clinical service; the eyewear is a big-ticket retail sale. Charging both at the same bundled software rate optimizes for neither — and the retail side, where the tickets are largest, usually pays the price.

The Retail Side Is Where the Rate Matters

On the clinical side, a vision plan like VSP or EyeMed pays much of the exam, and the patient’s card only touches a copay or a modest balance. On the optical side, it’s the opposite: insurance covers a limited allowance, and the patient pays the rest — the frame upgrade, the premium lenses, the coatings — often several hundred dollars on a single card. That patient-paid optical balance is the largest card transaction in the practice, and it’s the one most exposed to a bad rate.

Because the optical sale behaves like retail, it belongs on retail pricing. Interchange-plus pricing charges the true cost of each card plus a fixed, visible markup, which on a big-ticket eyewear sale lands well below a bundled 3-to-4-percent embedded rate. Shave a point and a half off every $600 pair, multiply by the eyewear volume a busy practice moves in a year, and the savings reach into the thousands — without touching the clinical billing at all.

The optical counter moves big-ticket, patient-paid sales all day. That volume should sit on a shopped interchange-plus rate, not a flat medical-software fee built for copays.

Your Eyecare Platform Now Wants Your Payments Too

Most practices run on an eyecare-specific platform — RevolutionEHR, Eyefinity, Crystal PM, Compulink, Sightview — and those platforms have moved aggressively into payments. RevolutionEHR launched its own embedded payments product, RevPay, in early 2026; Sightview’s payments run on Global Payments; the others bundle eyecare merchant services directly into checkout. The pitch is convenience, and it’s genuine: one screen, one ledger, automatic posting. But the rate baked into that embedded option was set for the platform’s economics, not yours, and it’s rarely the cheapest way to run a $600 sale.

This is the same pattern that quietly raises costs in dental practices and other software-driven offices: the system you chose for clinical reasons ends up choosing your processor for you. The fix isn’t to abandon the platform you like — it’s to recognize that you can usually bring your own processor underneath it, or at minimum negotiate the embedded rate with real numbers in hand, especially on the optical volume that carries the largest tickets. It’s the most fixable line in optometry payment processing.

Patient Surcharging Is Tempting, and Regulated

Some eyecare platforms now offer “optional patient surcharging” — passing the card fee to the patient — as a built-in feature. It’s understandable on a thin clinical margin, but it’s a regulated move, not a free switch. A surcharge applies to credit cards only and never to debit; a handful of states restrict or ban it; it must be disclosed before payment; and in a healthcare setting, adding a fee to a patient’s bill carries goodwill and compliance considerations a retail store doesn’t face.

For most practices, the better lever on the optical side isn’t surcharging the patient at all — it’s pricing the big-ticket eyewear sale correctly in the first place, or using a transparent dual-pricing approach where it’s permitted and clearly posted. If you do pass fees along, confirm what your state allows before you switch it on. This is general information, not legal advice.

Passing card fees to patients is governed by state law and card-network rules, can’t be applied to debit, and must be disclosed. Treat it as something to confirm for your state, not a default to switch on.

How to Audit Your Optometry Payment Processing

Start by splitting your effective rate by side of the house: what you pay on clinical copays versus on patient-paid optical balances, pulled from your processing statement and your platform’s reports. Then ask the questions that move money: is your optical volume on a shopped interchange-plus rate or a flat embedded one; can you bring your own processor into your eyecare software; and if you’re surcharging, is it compliant in your state. The biggest single win is almost always getting the eyewear sales off the bundled default.

The exam side is insurance-billed and largely fixed; the optical side is big-ticket retail you control. Put that eyewear volume on interchange-plus, unbundle the processor from your software, and the practice keeps far more of every premium pair sold.

Frequently Asked Questions

It depends on your mix, but the optical side — big-ticket, patient-paid eyewear — should be on interchange-plus, not a flat embedded healthcare rate that the platforms describe as commonly 2.5 to 4.5 percent. Shop that retail volume hard; the clinical exam side is insurance-billed and a different animal entirely.

No. RevolutionEHR’s RevPay, Sightview Pay, Eyefinity and the others are convenient, but they bundle a rate set for the platform’s margin, not yours. You can usually keep the software your team knows and run your own processor underneath it — compare the all-in cost, especially on optical sales, before defaulting to the embedded option.

Some platforms now offer it, but it’s regulated: surcharges apply to credit cards only, never debit, a few states restrict them, and they must be disclosed before payment — plus there’s the patient-goodwill question. On big-ticket eyewear, pricing the sale correctly or using compliant dual pricing is usually a better lever than charging patients. Confirm your state’s rules first; this isn’t legal advice.

Tools to Price Your Optical Volume Right

Send Us One Statement. We’ll Split Optical From Clinical.

Most optometrists have never seen what they pay to process a $600 eyewear sale versus a clinical copay, side by side. Send Brookside a recent statement and we’ll separate your optical rate from your exam rate, show what shopping the eyewear volume onto interchange-plus would save, and flag whether your eyecare platform’s embedded rate is one you could beat. The read takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Check Our Practice’s Real RateNo obligation • No pressure • Response within one business day

Figures shown are representative; RevolutionEHR, Eyefinity, Crystal PM, Sightview and other platforms set their own rates, which vary by plan. Surcharge and dual-pricing rules vary by state. Confirm current pricing and rules directly before relying on them.