Therapy Practice Payment Processing: The No-Show Fee You Can’t Collect

In a Therapy Practice, One Session Gets Paid Three Different Ways

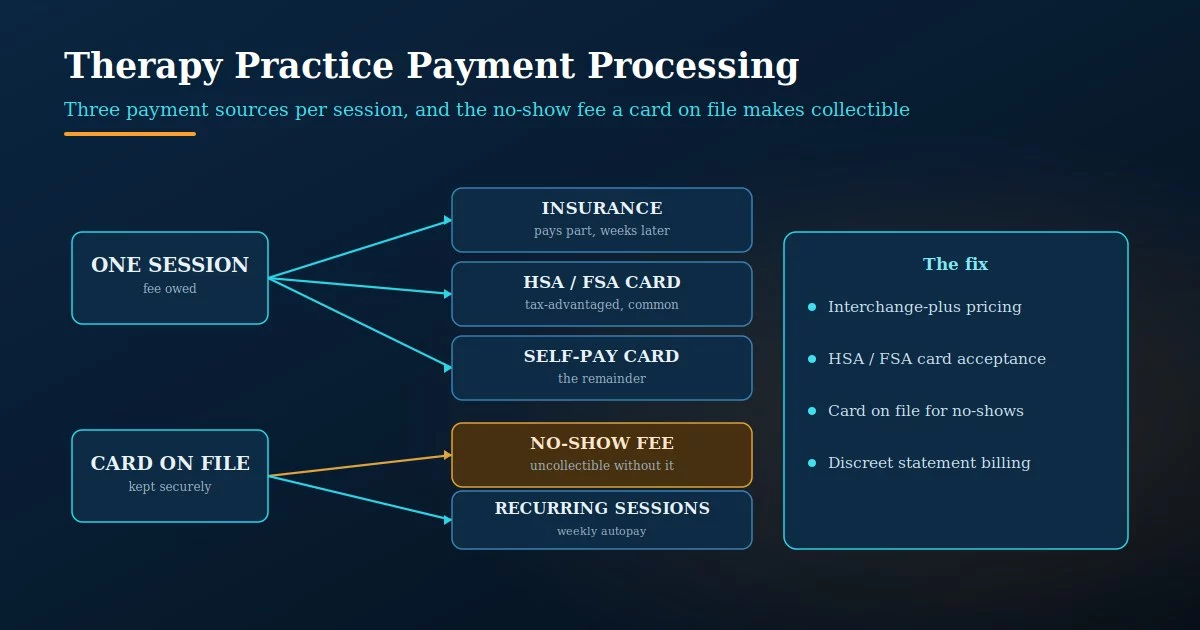

A single therapy session looks like one fee, but it almost never arrives as one payment. A slice comes from the insurer weeks later, a slice comes off an HSA or FSA card, and the remainder is self-pay on a personal card. That fragmentation is the defining feature of therapy practice payment processing, and it is why a setup built for a normal retail business quietly costs a private practice money it never sees leaving.

There is a second feature unique to this work: the appointment that doesn’t happen. A no-show or a late cancellation is lost clinical time the practice can’t resell, and it’s the single most recoverable piece of revenue most practices leave on the table — but only if the payment setup was built to collect it. Both of these come down to the same few decisions about how you take payment.

Three Payment Sources, One Session Fee

Start with where the money actually comes from. The insurer pays its contracted portion, often weeks after the session and after its own adjudication. The patient’s responsibility — the copay, the coinsurance, or the full fee for an out-of-network or private-pay client — gets paid at the time of service. And a large share of that patient portion now comes off a health spending card, because mental health therapy is generally an HSA- and FSA-eligible expense.

Here’s the part practices miss: those HSA and FSA cards run on the exact same Visa and Mastercard rails as any other card, which means they carry the same interchange and, if you’re on the wrong pricing, the same hidden markup. A practice that takes most of its patient payments on health spending cards and personal cards is running real card volume every day — and if that volume sits on a flat, bundled rate, the markup is buried in every copay. Good mental health payment processing treats that patient-pay volume as what it is: the core of the business, not an afterthought.

An HSA or FSA card isn’t a special payment type with special pricing — it’s a branded Visa or Mastercard tied to a tax-advantaged account, and it processes at standard interchange. The eligibility is the patient’s concern; the processing cost is yours. So the same question applies to it as to any card: is the markup on top of interchange visible, or buried in a flat rate?

You Can’t Enforce a No-Show Policy You Can’t Charge

Almost every practice has a 24- or 48-hour cancellation policy in its intake paperwork. Far fewer can actually collect on it, because a policy is only as real as your ability to charge it — and you can’t charge a card you don’t have. The practices that recover no-show revenue are the ones that keep a card on file with a signed financial agreement authorizing the charge, so a late cancellation becomes a clean, expected fee rather than an awkward invoice the patient may never pay.

This is where therapist credit card processing stops being a commodity and starts being a clinical-operations decision. A card on file, captured at intake under a clear policy, turns lost clinical hours into recovered revenue and removes the most uncomfortable money conversation in the practice. It also has to be done carefully: no-show charges are more likely than ordinary payments to be disputed, so the signed authorization and clear policy language aren’t paperwork formalities — they’re what protects you if a charge is challenged.

A cancellation policy without a card on file is a suggestion. The practices that actually collect no-show fees capture a card at intake with written authorization to charge it, which turns a lost hour into recovered revenue — and gives you the documentation to stand behind the charge if the patient disputes it later.

Three More Places the Setup Quietly Matters

A large share of sessions are now virtual, which means a large share of payments are card-not-present. Card-not-present transactions can be priced higher if the account isn’t set up to pass the right data, so a practice that went heavily telehealth without revisiting its processing can be paying more per session without realizing the channel changed. Recurring weekly or biweekly clients are the flip side of the same coin: a card on file with autopay means fewer declines, steadier cash flow, and far less time spent chasing balances — the same recurring logic that makes bank-account autopay worth offering to long-term clients who’d rather pay that way.

And then there’s discretion. A line item on a credit card statement is visible to whoever sees that statement, and for mental health care that can matter to a patient. A processor that lets you set a neutral, discreet billing descriptor is a small thing that reflects real care for the people a counseling payment processing setup ultimately serves. These details are part of what separates therapy practice payment processing from a generic terminal.

The same card on file that makes a no-show fee collectible also powers autopay for recurring clients — fewer declined sessions, steadier cash flow, and less front-desk time spent on balances. For a practice with a stable weekly caseload, it’s the single highest-leverage piece of the setup.

What Therapy Practice Payment Processing Should Look Like

The target setup follows directly from the work. Price the card volume on interchange-plus so the markup on every copay and HSA/FSA charge is visible instead of buried. Capture a card on file at intake under a signed policy so no-show fees are collectible and recurring clients are on autopay. Make sure the account is configured for card-not-present so telehealth sessions aren’t quietly downgraded to a higher rate. Set a discreet billing descriptor. And know your blended effective rate across all of it, because in a practice this payment-fragmented, that one number is the only honest measure of what you’re paying.

None of this is exotic, and none of it changes how you practice. It’s the difference between generic card acceptance and therapy practice payment processing built for a practice that gets paid three ways per session and lives or dies on collecting for the time it reserves. For a clinician, that difference is hours of recovered revenue and a markup that finally shows itself.

The worst position is a flat rate with no card on file: you overpay on every copay and HSA/FSA charge because the markup is hidden, and you under-collect because you can’t enforce the no-show policy. It’s the most common private practice payment processing setup and the most expensive — paying more to keep less. Fix both at once: transparent pricing and a card on file.

Frequently Asked Questions

Yes, when you keep a card on file with a signed financial agreement that authorizes the charge under a clear cancellation policy. The authorization and policy language matter, because no-show charges are disputed more often than ordinary payments, and the documentation is what lets the charge stand.

No — they run on the same card networks at standard interchange. Eligibility (whether the expense qualifies) is the patient’s responsibility; your cost is the same as any card. What determines your cost is your pricing structure, which is why interchange-plus matters on a practice with heavy HSA/FSA volume.

Interchange-plus pricing so the markup is visible, a card on file under a signed policy so no-shows are collectible and recurring clients are on autopay, card-not-present configured for telehealth, and a discreet billing descriptor. That combination handles the patient-pay volume, the no-show revenue, and the privacy this work calls for.

Keep reading on practice payments and what you pay

Stop Overpaying on Copays and Under-Collecting on No-Shows

Send Brookside one recent statement and we’ll calculate your true effective rate across your copays, HSA/FSA, and self-pay volume, and flag whether your setup can actually collect a no-show fee. No switch required to find out. Learn more about payment processing consumer protections from the CFPB.

Get Your Practice Rate ReviewedNo obligation • No pressure • Response within one business day