Landscaping Payment Processing: Two Seasons, One Rate

One Rate Can’t Fit a $15k January and an $80k June

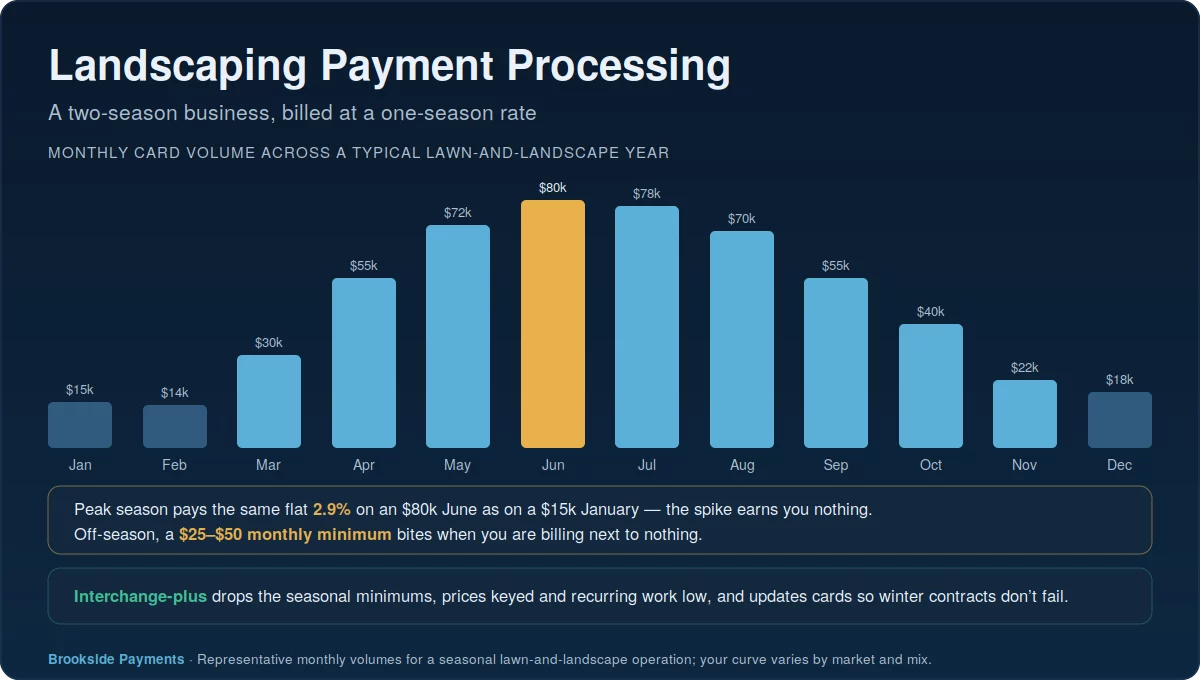

Landscaping payment processing has a problem most processors are built to ignore: the business has two completely different seasons, and a single flat rate optimizes for neither. Card volume that sits at $15,000 in January can climb past $80,000 in June, then fall back to a handful of snow-removal invoices by December. A pricing plan designed for a steady retail shop quietly punishes that swing at both ends — overcharging on the summer peak and billing minimum fees through the dead of winter.

Add in a transaction range that runs from a $40 mowing invoice to a $5,000 tree removal, revenue that’s increasingly locked into recurring maintenance contracts, and field-service software that now picks your processor for you, and the standard flat-rate setup ends up wrong in four different directions at once. The good news is that each of those is fixable — once you stop treating a seasonal, contract-heavy field business like a corner store. That four-way mismatch is the heart of landscaping payment processing, and lawn care payment processing carries every piece of it.

On a flat plan, the $80,000 month earns you no break for the volume, and the near-zero winter month still gets hit with a monthly minimum. The plan is calibrated for a business that looks the same in January and July — which yours never does.

Peak Volume Earns Nothing, Off-Season Minimums Still Bite

The seasonal swing costs you at both ends. At the peak, flat-rate pricing charges the same 2.9% whether you run $15,000 or $80,000 — the volume that would earn a real business a better rate earns a flat-rate landscaper nothing. Then the season turns, and the same plan keeps charging: many processors bill a $25-to-$50 monthly minimum, which lands hardest in the winter months when you might process only a few snow-removal jobs and the minimum is most of what you pay.

This is exactly the profile a seasonal merchant account is meant to handle — no monthly minimums that punish a slow December, and pricing that reflects what you actually process rather than a flat assumption about steady year-round volume. For a business that does most of its revenue in a five-month window, getting off the minimum-fee treadmill alone can save more than any single rate negotiation.

A monthly minimum is designed for a business with steady volume. Drop one on a landscaper and it inverts — the fee bites hardest in the off-season, exactly when there’s almost no revenue to absorb it.

A $40 Mow and a $5,000 Install Don’t Belong on the Same Rate

Landscaping spans an enormous range of transaction sizes, and flat-rate pricing handles the extremes badly. On a $40 mowing invoice, the fixed per-transaction fee — the $0.30 tacked onto every charge — is a real bite out of a small ticket. On a $5,000 install or tree removal, it’s the percentage that hurts, turning a single job into a $145 processing cost. One rate can’t be efficient for both, and most landscapers run both all day.

Most of those payments also arrive as invoices — keyed in or paid online after the work is done — rather than tapped at a counter. Interchange-plus pricing fits this far better: it charges the true network cost plus a small fixed markup, so the big installs aren’t crushed by a blanket percentage and the small mows aren’t dominated by padding. You see exactly what each card type costs, across the whole range of jobs — a core piece of landscaping payment processing that flat rates miss.

Recurring Revenue, and Who’s Really Processing It

More and more landscaping revenue is recurring — weekly and biweekly mowing routes, multi-step fertilization programs, seasonal contracts billed to a card on file. That’s stable, predictable money, but card-on-file recurring billing has a quiet leak: when a customer’s card expires or is reissued, the recurring charge fails. Without a card updater running in the background, a meaningful share of recurring charges decline every month, and your office ends up chasing customers for new card numbers instead of mowing lawns.

And the platform running all of this — Jobber, LMN, Aspire, Service Autopilot, Yardbook — increasingly wants to be your processor too. Jobber’s built-in payments run on Stripe at the standard 2.9% plus $0.30; LMN Pay runs on Stripe as well; the others bundle processing into checkout. It’s convenient, but the rate is set for the platform, not for you. You can usually keep the software your crews already use and run your own processor underneath it — and if you’re on Jobber specifically, it’s worth seeing the exact Jobber fee breakdown before you accept the default.

Bundled platform payments are the easy default, not the cheap one. Keeping the operations software while unbundling the processing is usually the single biggest lever on a contract-heavy landscaping book.

How to Audit Your Landscaping Payment Processing

Start with your real effective rate, pulled from both a peak-season and an off-season statement so the seasonal distortion is visible. Then check the four levers: are you paying a monthly minimum that bites in winter; is your volume on interchange-plus or a flat rate; is a card updater running on your recurring contracts; and is your processor bundled by your software or chosen by you. For residential crews that collect in person, a compliant cash discount program can cut fees to near zero, since many homeowners are glad to pay cash or debit for lawn care. This is the seasonal field-service version of the broader home-services payment picture — built specifically around the swing, the contracts, and the green-industry software.

Kill the off-season minimum, move to interchange-plus, switch on a card updater for contracts, and unbundle the processor from your software. Those four moves fit the seasonal, recurring shape of a landscaping book far better than any flat rate ever will.

Frequently Asked Questions

Not a flat-rate app with seasonal minimums. Interchange-plus pricing fits landscaping best — it handles the swing with no monthly minimum, prices the wide range of ticket sizes fairly, and supports recurring contracts with a card updater. For residential crews collecting in person, a cash discount program can cut card fees to near zero.

No. Jobber, LMN Pay, Aspire and the others bundle payments — Jobber’s run on Stripe at 2.9% + $0.30 — but that rate is set for the platform, not for you. You can usually keep the software your crews use and run your own processor underneath it. Compare the all-in cost before defaulting to the built-in option.

Avoid processors that charge a monthly minimum, because it bills you through the winter when your volume drops to a few snow-removal jobs. Interchange-plus pricing typically has no seasonal minimum — you pay on what you actually process — so the slow months stay cheap instead of carrying a fixed fee you can’t earn back.

Tools for a Seasonal, Contract-Heavy Book

Send Us a Peak and an Off-Season Statement.

Most landscapers have never seen their processing cost laid out across the seasons — what the summer peak really costs, and what those winter minimums add up to. Send Brookside a busy-month and a slow-month statement and we’ll show your true effective rate across both, flag whether a monthly minimum is bleeding you in the off-season, and tell you whether interchange-plus or a cash discount program fits your mix. The read takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Check Our Real RateNo obligation • No pressure • Response within one business day

Figures shown are representative; Jobber, LMN, Aspire, Service Autopilot and other platforms set their own rates, which vary by plan. Monthly volumes and ticket sizes vary widely by market and service mix. Confirm current pricing directly before relying on it.