Hotel Payment Processing: The Costs the Rate Sheet Hides

Hotel Payment Processing Isn’t About the Swipe Rate

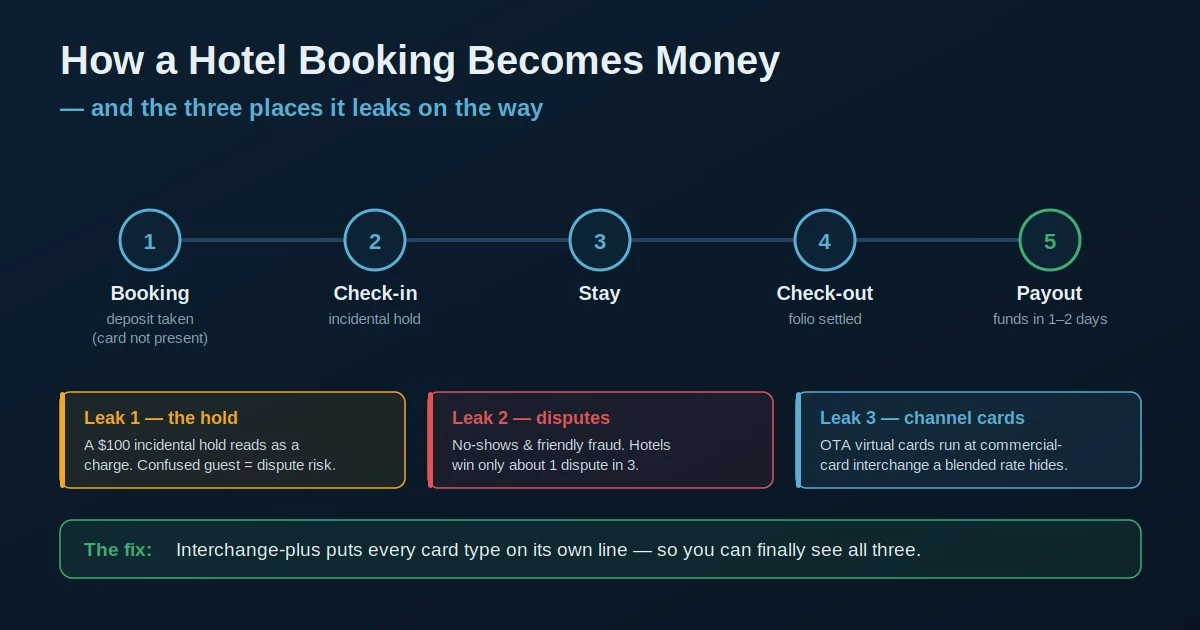

Hotel payment processing looks like a rate problem and is really a workflow problem. Most lodging owners shop the headline percentage their software quotes them and stop there, but a hotel charges cards in ways a restaurant or retail shop never does: a deposit taken weeks before arrival, an incidental hold placed at check-in, a folio settled at check-out, a no-show billed to a card the guest never handed over, and a third party’s single-use card arriving in lieu of a real guest. The money in lodging payment processing leaks through that layer — the deposits, holds, disputes, and channel cards — not through a tenth of a percent on the swipe.

That matters because the part of hotel payment processing you can see on a rate sheet is the part that’s already close to competitive. The part you can’t see — how your system handles a $400 authorization that the guest’s bank reads as a charge, or what a Booking.com card actually costs you to run — is where a property quietly overpays for years.

Your Property Management System Usually Picks Your Processor

Most independent hotels, inns, and B&Bs run a property management system — Cloudbeds, Mews, Little Hotelier, RoomRaccoon — and most of those platforms bundle a payment processor right into the software. Cloudbeds offers Cloudbeds Payments, built on Stripe. Mews offers Mews Payments, also built on Stripe. The pitch is real convenience: the card data flows straight into the reservation, deposits and folios reconcile themselves, and there’s nothing extra to set up.

The cost shows up in two places. First, the pricing model is often blended — one flat percentage across every card type — which is the opposite of what a hotel wants, for reasons the channel-card section below makes plain. Some platforms quote interchange-plus-plus for Visa and Mastercard but switch to a blended rate for Amex and other cards, so the most expensive transactions hide inside an averaged number. Second, some systems either restrict which outside processor you’re allowed to connect or add a fee for using one, which quietly removes the leverage you’d normally have to shop the rate.

None of that makes the bundled option wrong — for a very small property the simplicity can be worth it. But “it came with the software” is not the same as “it’s the best rate I can get,” and the only way to know the difference is to compare the embedded rate against an interchange-plus quote on your actual card mix.

A blended rate charges you the same percentage on a rewards card, a debit card, and a commercial card — even though those cost the processor very different amounts. You never see the spread, so you can’t tell whether the markup is fair. Interchange-plus shows the network cost and the processor’s margin as separate lines, which is the only way to audit what you’re paying.

Deposits and Holds Are a Payment Workflow, Not a Footnote

A hotel rarely charges a card once at the point of sale. It takes a deposit when the reservation is made — frequently weeks out, with no card physically present — then places an authorization hold at check-in to cover incidentals, then settles the real amount at check-out. Each of those is a separate decision your hotel credit card processing setup has to handle correctly.

The authorization hold is the one that bites. The property sets the hold amount; the guest’s bank decides how long it stays on the account, and a hold can sit there for up to thirty days. To the guest, a $150-a-night room plus a $100 incidental hold can read as money already gone, especially on a debit card where it reduces available funds immediately. When the final folio then posts as a separate line, a confused guest is one tap away from disputing the whole thing. Clear disclosure of the hold amount at booking and at check-in isn’t a courtesy — it’s chargeback prevention.

A pre-arrival deposit, a no-show charge, and a cancellation fee are all card-not-present transactions — the guest isn’t standing at your desk. Those carry higher interchange and more dispute risk than a card dipped at check-in. A processor and a workflow that capture a proper authorization (and keep the record) are what make those charges defensible later.

Chargebacks Are the Real Hotel Payment Cost

Ask a hotelier where payments hurt and the honest answer is usually disputes, not rates. The most expensive part of hotel payment processing for a busy property is the money that walks back out the door after it has already landed. Chargebacks in lodging are driven by card-not-present bookings, unclear cancellation and incidental policies, and gaps in verifying who actually used the card. Most of them are first-party — the “friendly fraud” where a guest who recognizes the charge disputes it anyway — which by common industry estimates is roughly three-quarters of all chargebacks. And the deck is stacked: merchants in travel and hospitality win only about a third of the disputes they fight.

A surprising amount of that loss traces to something mundane: the billing descriptor. If a guest checks their statement a month later and sees “LLC Holding Co. 482” instead of your property’s name, they dispute it on reflex. Your descriptor should carry the recognizable property name and, ideally, the front desk phone number. Past that, the levers are operational — written acknowledgment of incidental holds and cancellation terms, a captured authorization on file, and a processor whose dispute tooling actually lets you submit evidence instead of losing by default.

When the bank pulls funds for a disputed no-show or a “surprise” incidental, it also adds a chargeback fee and forces your staff to assemble paperwork. Properties that shrug and absorb it are leaving real money on the table — the recoverable share of those disputes is larger than almost any rate concession you’d negotiate, and it starts with a recognizable descriptor and a documented authorization, not a lower swipe percentage.

The OTA Virtual Cards You Can’t Price Around

When a guest books through Expedia or Booking.com under the agency’s collect model, you often don’t receive the guest’s card at all. Expedia issues an Expedia Virtual Card; Booking.com issues a virtual card through its payments program; Agoda does the same. You charge that single-use card after check-out, and the funds land in your account like any other card payment, usually within a day or two.

Here’s the part that the bundled blended rate buries: those channel cards are commercial cards, and commercial cards carry materially higher interchange than a consumer credit or debit card. The more of your business comes through the OTAs, the more of your volume runs at that higher cost — and on a single flat percentage, you’d never see it, because the expensive transactions are averaged in with the cheap ones. Some processors even tack on an extra fee specifically for processing virtual cards. A property doing a third or more of its nights through channels is paying a premium it can’t measure until the pricing is broken into an effective rate per card type.

This is the single strongest argument for interchange-plus in hotel payment processing: it’s the only model that puts the commercial-card cost on its own line, so you can see exactly what the channel mix is doing to your margin instead of trusting an average.

What Actually Lowers a Hotel’s Payment Cost

The levers that move the number are rarely the swipe rate by itself. They’re structural: price transparently, hold the leverage to shop, and stop the leaks.

- Move to interchange-plus so commercial channel cards, Amex, and consumer cards are each priced on their true cost — the averaging is where overpayment hides.

- Keep the processor unbundled from the software — a hotel merchant services account you own rather than rent — or choose a PMS that lets you connect an outside gateway, so the rate stays shoppable instead of locked to whatever the platform bundles.

- Close the dispute leak with a recognizable billing descriptor, documented authorizations on deposits and incidental holds, and clear written cancellation terms — the recoverable money here usually dwarfs any rate cut.

Hotel payment processing is a system, not a single percentage. The property that audits the whole system — the embedded rate, the channel-card mix, and the chargeback loss — almost always finds more savings in the parts that never appear on the quote than in the one number that does.

Frequently Asked Questions

Not necessarily. A bundled processor is built for convenience, and it’s often priced on a blended rate that averages your card types together. It may be competitive, but the only way to know is to compare it against an interchange-plus quote run on your actual mix of consumer, Amex, and OTA channel cards.

Expedia and Booking.com pay you through single-use virtual cards, which are commercial cards. Commercial cards carry higher interchange than consumer cards, so the more of your volume comes through the channels, the more you pay — and a flat blended rate hides it by averaging it in with cheaper transactions.

For most properties it’s chargebacks, not the swipe rate. Card-not-present deposits, no-shows, and incidental holds generate disputes, and hospitality merchants win only about a third of them. A recognizable billing descriptor and documented authorizations recover more than almost any rate negotiation.

Keep reading on rates, holds, and disputes

Send Your Statement. We’ll Show You What the Channel Cards Are Costing.

If your processor came bundled with your property management system, or your OTA bookings run on a blended rate, send Brookside one recent statement. We’ll break it into an interchange-plus view by card type, show you what the commercial channel cards and Amex are actually costing, and tell you where the dispute losses are. The math takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day