Wedding Venue Payment Processing: You’re Paid Long Before the Big Day

You Take the Money a Year Before You Deliver Anything

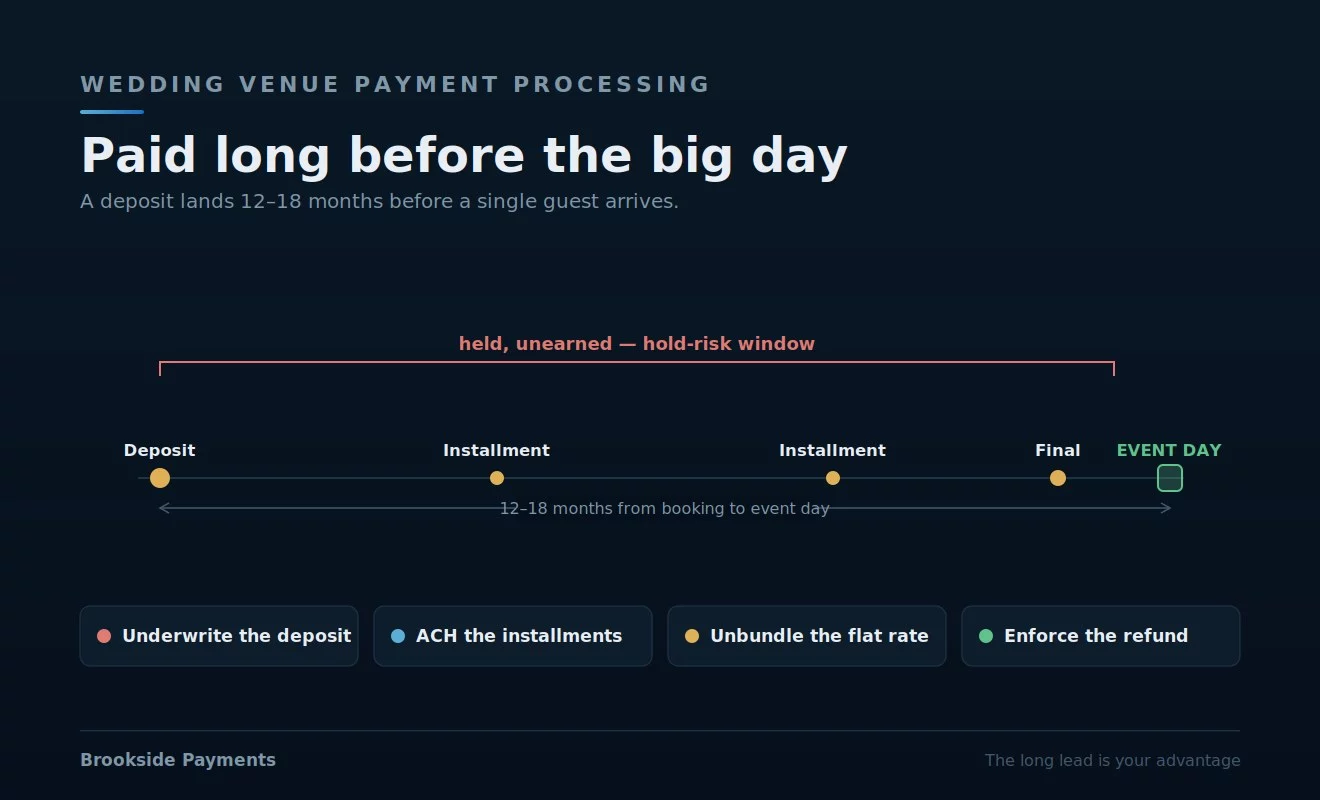

A wedding venue books a date twelve to eighteen months out and collects a deposit the moment the contract is signed — then holds that money, and the installments that follow, for a year or more before a single guest walks in. No other business carries that long a gap between getting paid and delivering. That gap is the whole story of wedding venue payment processing: it shapes your risk, your fees, and whether the deposit you’re counting on is actually safe when the date finally arrives.

The venue-management software almost everyone runs — HoneyBook, Tripleseat, Perfect Venue, Planning Pod, Releventful, Momentus — is built around exactly this rhythm: deposit, installment schedule, final balance before the date, day-of add-ons. What it doesn’t always make visible is who’s actually processing those payments, at what rate, and what happens to a large deposit that sits “unearned” on a processor’s books for eighteen months. Get wedding venue payment processing right and the long lead funds your calendar; get it wrong and it invites a held deposit or a disputed payment at the worst possible moment.

Money Held 18 Months Before the Event Is What Triggers Holds

Here’s the risk that defines wedding venue payment processing. When you collect a large deposit for an event eighteen months away, a processor sees money taken for a service that hasn’t been delivered and won’t be for a very long time — the textbook profile for a reserve, a hold, or a frozen payout. It’s worse when your processing runs through a payment facilitator (the bundled aggregator model many venue platforms use, where you’re a sub-account rather than a true merchant), because a PayFac can freeze far faster and with less warning than a dedicated account. The longer the lead, the bigger the exposure — and weddings carry the longest lead there is.

It compounds with disputes: a client can file a chargeback on a deposit months before the event, and if anyone cancels, the refund and dispute exposure on a large sum is real. The defense is structural — a real, underwritten wedding venue merchant account whose risk profile expects long-lead deposits rather than an aggregator that flags them as anomalous, plus clean records tying every payment to a future-dated, signed contract. The deposit pile is your working capital for that date; the one thing you cannot afford is to have it frozen.

In wedding venue payment processing, a large deposit for an event 12–18 months out is exactly the profile that triggers reserves and frozen payouts — and a bundled PayFac (where you’re a sub-account, not a true merchant) can freeze faster and with less warning. Get a real merchant account whose underwriting expects long-lead deposits, and tie every payment to a future-dated, signed contract so the money reads as documented, not anomalous.

Big Installments Belong on ACH, Not Cards

Venues bill in stages — booking deposit, scheduled installments, final balance before the date — and those tickets are large. On a $15,000 event paid by card, interchange runs roughly four hundred and fifty dollars; the same payment by ACH is a few dollars. Across a calendar of events, the method you collect on becomes the single biggest number in wedding venue payment processing, dwarfing whatever headline rate you negotiated. Cards are an expensive way to move large, scheduled payments, and a venue’s installments are exactly that.

The better setup leans on the bank rail: put the deposit and installments on ACH or e-check with a card on file as backup, and reserve cards for the small, convenience-driven pieces — a day-of bar tab, a last-minute add-on — where the fee is worth it. Venue software can automate the installment schedule either way; the real question is which rail each charge rides. Sound venue deposit payment processing routes the big money over ACH and saves cards for where speed actually matters.

A $15,000 event on card costs ~$450; by ACH it’s a few dollars — and a venue runs that across a full calendar. Put the deposit and scheduled installments on the bank rail with a card on file as a backup, and reserve cards for small day-of add-ons. The installment schedule automates either way; in wedding venue payment processing, what matters is which rail each charge rides.

Your Booking Software Sets the Rate — Usually a Flat One

Most venue platforms either integrate a gateway like Stripe or Square or bundle their own “native” processing, and in both cases the rate is typically a flat aggregator number — often around three percent — folded into the software experience. Flat-rate processing is simple, but on a venue’s large tickets it’s expensive: a flat percentage charges a $20,000 wedding the same way it charges a $200 deposit, with no benefit from the lower interchange that big, well-qualified transactions should earn. That hidden markup is the most overlooked line in event venue payment processing.

Pulling the rate apart from the software is often the biggest single saving, and it doesn’t always mean leaving the platform you like. Many venue systems let you connect an outside processor; where they do, you keep the booking tools and route the actual processing to an interchange-plus account where large transactions are priced on their real cost. Where a platform locks you to its bundled flat rate, that lock-in is itself a cost worth weighing at renewal. Good wedding venue credit card processing treats the software and the rate as two separate decisions.

In wedding venue payment processing, venue platforms usually bundle a flat ~3% rate (native or via Stripe/Square) that charges a $20,000 wedding like a $200 deposit, ignoring the lower interchange big transactions earn. Where the platform allows an outside processor, keep the software and route processing to interchange-plus so large tickets are priced on real cost. Where it locks you in, count that lock-in as a renewal cost.

One Cancellation Is a Five-Figure Problem

The flip side of big tickets and long leads is big exposure. When an event cancels — or a client disputes a deposit — you may be returning or fighting over a five-figure sum, sometimes after you’ve already turned away other bookings for that date or spent against the deposit. A vague refund policy, or a processor that doesn’t back you, turns a cancellation into a loss and a dispute into a chargeback. This belongs in any honest look at wedding venue payment processing, not as an afterthought.

The protection is partly paperwork and partly plumbing: a clear, well-disclosed deposit, refund, and cancellation policy written into the signed contract, and a processor and account set up to enforce it — proper documentation, the right deposit handling, and a real merchant relationship that will stand with you in a dispute rather than simply reversing the charge. Pair a tight contract with an account built for large, future-dated transactions — the backbone of safe wedding venue payment processing — and a cancellation becomes a known process instead of a surprise hit.

A cancelled or disputed event can mean returning or fighting a five-figure sum — often after you’ve turned away other bookings. Put a clear deposit/refund/cancellation policy in the signed contract, and pair it with a processor that documents future-dated payments and backs you in a dispute rather than just reversing the charge. In wedding venue payment processing, a tight contract plus the right account turns a cancellation into a process, not a loss.

The Long Lead Is Your Advantage — Protect It

A wedding venue’s long lead time is a gift: you book and bank revenue a year or more before you deliver. Wedding venue payment processing done well keeps that gift from turning on you — a real merchant account that underwrites long-lead deposits instead of an aggregator that freezes them, deposits and installments collected on ACH instead of card rates, the processing unbundled from the booking software so five-figure tickets aren’t priced flat, and a refund policy your processor will actually enforce. Do that, and the money you collect long before the big day is there, and safe, when the day finally arrives.

Frequently Asked Questions

The lead time. A venue books a date twelve to eighteen months out and collects a deposit immediately, holding that money — and the installments after it — for a year or more before delivering anything. That long gap between getting paid and providing the service is the longest of any business, and it drives the category’s defining risks: processor holds on “unearned” deposits, big-ticket installments that belong on ACH, and serious refund exposure if an event cancels.

Yes, and the long lead is exactly why. When a processor sees a large payment for a service that won’t be delivered for many months, it may place a reserve or hold — and that risk is higher if your processing runs through a bundled payment facilitator (where you’re a sub-account) rather than a true merchant account. In wedding venue payment processing, the defense is a real account underwritten for long-lead deposits, with each payment documented against a future-dated, signed contract.

ACH for the big payments, cards for the small ones. On a $15,000 event, card interchange is around four hundred and fifty dollars versus a few dollars by ACH — across a full calendar that’s the largest number in wedding venue payment processing. Put the deposit and installment balances on the bank rail with a card on file as backup, and reserve cards for day-of add-ons like a bar tab where convenience is worth the fee.

Keep reading on deposits, holds, and big-ticket processing

See What Your Venue Is Really Paying — and Risking

Send Brookside one recent statement and we’ll show your true effective rate inside your booking software, what moving deposits and installments to ACH would save across your calendar, and whether your processing runs through a PayFac that could hold a long-lead deposit. It’s wedding venue payment processing built around a real merchant account for big, future-dated tickets. No switch required to find out. You can also review card payment protections from the CFPB.

Get Your Venue ReviewedNo obligation • No pressure • Response within one business day