Funeral Home Payment Processing: The Pre-Need Cost Nobody Prices

Funeral Home Payment Processing Isn’t About the Swipe Rate

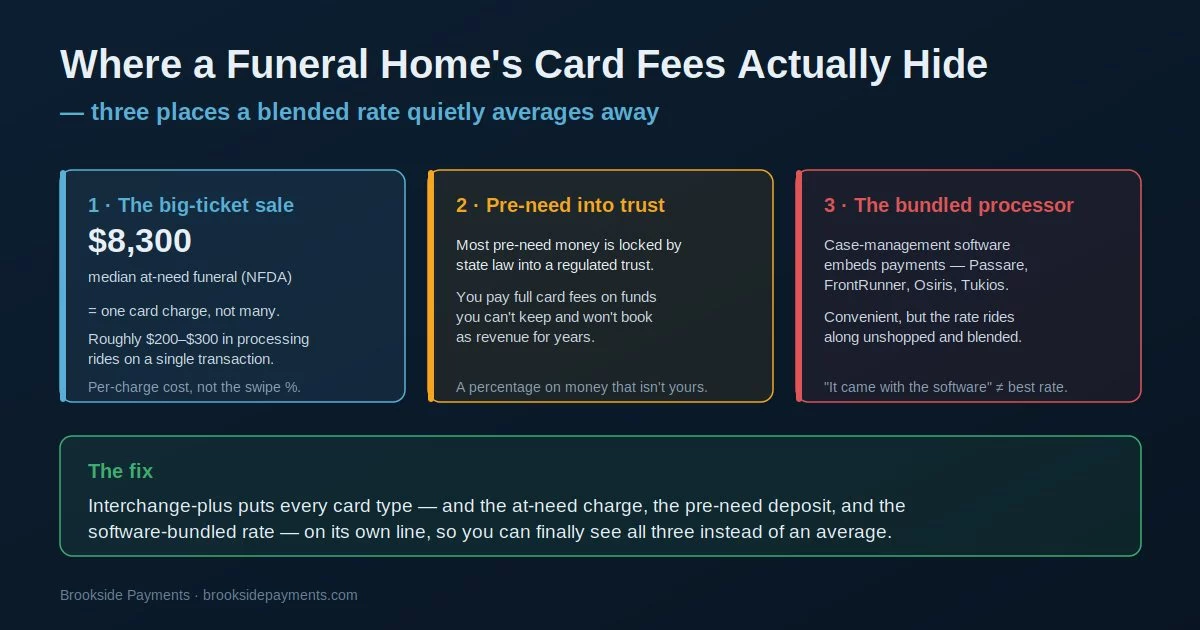

Funeral home payment processing looks like a rate problem and is really a structure problem. A funeral home doesn’t charge cards the way a restaurant or a retail shop does — it collects a single large at-need payment at the worst moment in a family’s life, it takes pre-need money years in advance that the law often won’t let it keep, and it usually runs all of it through whatever processor came bundled with its case-management software. The cost lives in those three places — the big-ticket charge, the trust-bound pre-need dollars, and the embedded rate — not in a tenth of a percent on the swipe.

That matters because the part of funeral home payment processing you can see on a rate sheet is already close to competitive. The part you can’t see — what a $9,000 charge actually costs you to run, or what you’re paying in card fees on money that has to sit in a state-regulated trust — is where a firm quietly overpays for years.

Your Case-Management Software Usually Picks Your Processor

Most funeral homes run case-management software — Passare, FrontRunner, Osiris, SRS — and most of those platforms now bundle a payment processor directly into the product. Passare added integrated card processing inside its case management; FrontRunner sells FuneralPay for taking payments on the firm’s website; Osiris offers optional integrated processing; Tukios builds online payments into the funeral home website. The pitch is real convenience: a balance gets paid, the case file updates, and the books reconcile without anyone re-keying a number — and the platform quietly decides the firm’s funeral home payment processing along the way.

The cost shows up in two places. First, the embedded rate is usually blended — one flat percentage across every card type — which means the expensive cards hide inside an average you never get to inspect. Second, low transaction count works against you here in a way it doesn’t for a busy retailer: a funeral home might handle a few hundred cases a year, so a monthly account fee, a per-item fee, and a statement fee spread across far fewer, far larger sales — and each one takes a bigger bite per transaction than it would at a shop ringing up hundreds of cards a day. “It came with the software” is not the same as “it’s the best rate I can get,” and the only way to tell the difference is to compare the embedded number against an interchange-plus quote on your real mix of sales.

A blended rate charges the same percentage on a debit card, a rewards card, and a commercial card, even though those cost the processor very different amounts. You never see the spread, so you can’t tell whether the markup is fair. Interchange-plus shows the network cost and the processor’s margin as separate lines — the only way to audit what a large funeral charge is really costing you.

An At-Need Funeral Is One Large Charge, Not Many Small Ones

The economics of funeral home payment processing are unusual because the average sale is so large and so infrequent. The national median cost of a funeral with viewing and burial is about $8,300, and a funeral with cremation about $6,280, according to the National Funeral Directors Association — and a firm that adds a vault, cemetery items, or merchandise can clear $10,000 on a single arrangement. When a family pays that on a card, the percentage you pay runs against the whole amount, so one transaction can carry $200 to $300 in processing cost by itself.

That changes which lever matters. At a high-volume retailer the swipe percentage is everything; at a funeral home, the cost is concentrated in a handful of big charges, which is exactly where a few tenths of a percent — or a single mis-priced card type — turns into real money per sale. It’s also why dual pricing or a compliant surcharge and ACH are common levers in funeral home credit card processing: passing the card cost on a five-figure charge, or steering it to a bank transfer, saves more than any rate negotiation. The catch is that those tools have to be handled with unusual care, because the customer is a grieving family — many firms quietly default to ACH or check on the large balance rather than present a surcharge line at the arrangement table.

One $9,000 card sale is not the same risk or cost as ninety $100 sales. Large-ticket transactions can draw extra scrutiny from a processor, can bump into card limits, and concentrate your processing cost into a few payments a month. A processor and a pricing model built for a low-volume, high-value business behave very differently from a flat rate designed for a coffee shop — and the blended quote rarely tells you which you have.

You Pay Card Fees on Pre-Need Money You Don’t Get to Keep

This is the part of funeral home payment processing almost no one prices correctly. When a family pre-pays for a funeral, that money usually can’t stay with the firm. A pre-need contract is funded one of two ways — through a state-regulated trust or through an assigned life insurance policy — and most states require that some or all of the trust-funded payment be deposited into a restricted, regulated account. Some states require 100% into trust; others require 70% or 80%, with the remainder kept as an upfront fee. Money sitting in a properly funded trust does not belong to the funeral home, and the firm won’t recognize it as revenue until the service is actually delivered, which can be years away.

Now put a card on top of that. If a family pays pre-need by credit card, the firm pays full interchange — roughly two to three percent — on the entire amount, and then has to turn around and deposit most of that money into a trust it can’t touch. You’ve paid a percentage on dollars that aren’t yours, to hold money for a service you’ll provide later. Pre-need installment plans make it worse in a quiet way: a family paying a contract off over months or years is a recurring card arrangement against a future obligation, and every installment carries its own card fee. The firms that handle this well route pre-need toward ACH, check, or insurance assignment specifically to keep card fees off trust-bound money — the most mispriced decision in funeral home payment processing, and one a blended rate makes invisible.

Collecting pre-need by card feels like service, but you’re paying interchange on money the law won’t let you keep, recognized as revenue years from now. On a $10,000 pre-need contract that can be $200–$300 in fees on funds headed straight into trust. Steering pre-need to ACH or insurance assignment — and pricing the card path on interchange-plus when a card is unavoidable — keeps that cost from compounding contract after contract.

What Actually Lowers a Funeral Home’s Payment Cost

The levers that move the number in funeral home payment processing are structural, not a single renegotiated percentage. They come down to seeing the cost, keeping the leverage to shop it, and routing each kind of payment to the cheapest path it can take.

- Move to interchange-plus so the big at-need charge, the pre-need deposit, and each card type are priced on true cost — the averaging in a blended rate is where overpayment hides on large, infrequent sales.

- Keep the processor unbundled from the software — a funeral home merchant account you own rather than rent — or choose a platform that lets you connect an outside gateway, so the rate stays shoppable instead of locked to whatever the case-management system bundles.

- Route by payment type — steer large at-need balances and trust-bound pre-need toward ACH, check, dual pricing, or insurance assignment, and reserve card acceptance for where it genuinely adds convenience.

Funeral home payment processing is a structure, not a single percentage. The firm that audits the whole structure — the embedded rate, the cost of its big-ticket charges, and the card fees riding on trust-bound pre-need — almost always finds more savings in the parts that never appear on the quote than in the one number that does. Comparing your blended quote against a true effective rate by payment type is where that audit starts.

Frequently Asked Questions

Not necessarily. Software-bundled processing is built for convenience and is usually priced on a blended rate that averages your card types together. Because a funeral home makes few, large sales, fixed fees and a blended markup hit harder per transaction than they would at a high-volume shop. The only way to know is to weigh your funeral home payment processing against an interchange-plus quote on your actual mix of at-need and pre-need payments.

Because you pay full interchange on the entire amount, then most states require that money to be deposited into a regulated trust you can’t keep or recognize as revenue until the service is delivered. You’ve paid a percentage on dollars that aren’t yet yours. Routing pre-need funeral payments to ACH, check, or insurance assignment keeps card fees off trust-bound funds.

It’s the concentration of cost in a few large charges plus the card fees on pre-need money headed into trust. A single at-need sale can carry $200–$300 in processing, and a blended rate hides which payment types and which channels are driving it. Interchange-plus and routing by payment type are what surface it.

Keep reading on rates, big tickets, and pre-need

Send Your Statement. We’ll Show You What the Big Tickets and Pre-Need Are Costing.

If your processor came bundled with your case-management software, or your pre-need and at-need charges run on a blended rate, send Brookside one recent statement. We’ll break it into an interchange-plus view by payment type, show you what your large at-need charges and pre-need card fees are actually costing, and where to route them instead. The math takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day