Funeral Home Surcharging: Legal Is the Easy Part

Funeral Home Surcharging: Legal Is the Easy Part

Funeral home surcharging is one of the few payment decisions where the law is the simple half of the problem. In most states a funeral home can legally pass its card-processing cost to the family, within clear rules — but a funeral bill is the single worst place in retail to get the optics wrong. A three percent fee on a $9,000 funeral is roughly $270, itemized as a separate line on the bill of a family that buried someone this week. The compliance is learnable in an afternoon; the harder question is whether, and how, to pass that cost without it reading as predatory.

So funeral home surcharging is really two questions stacked together. First, what do the card networks and your state actually allow? Second — the one most articles skip — which method passes the cost in a way a grieving family can accept, and does that answer change between an at-need arrangement and a pre-need one? It does, sharply, and that’s where the real decision lives.

What the Card Rules and State Law Require

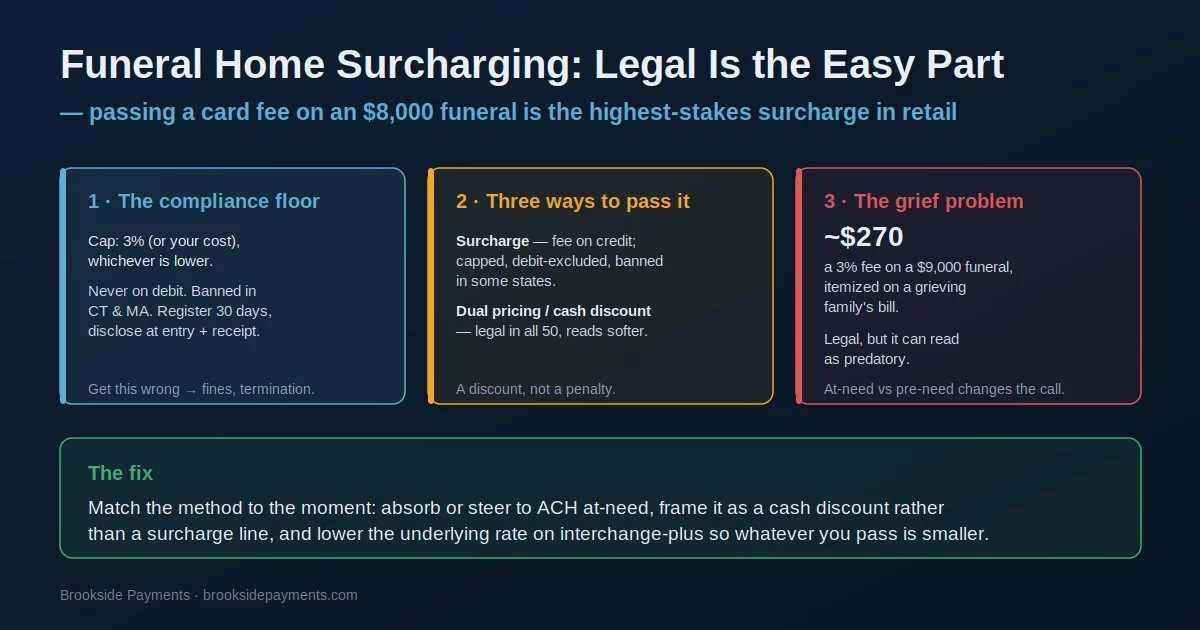

Before any judgment call, funeral home surcharging has a compliance floor you can’t go below. A credit card surcharge is capped at the lower of the card network limit — 3% under Visa, 4% under Mastercard, so effectively 3% if you take both — or your actual cost of acceptance; if your effective rate is 2.4%, your surcharge can’t be 3%. A few states cap lower (Colorado at 2%; several others limit it to your actual processing cost). You can never surcharge a debit card, even when the customer runs it as credit — that’s federal law under the Durbin Amendment, and it applies to prepaid cards too, so your terminal has to identify card type and suppress the fee automatically. And a handful of states prohibit surcharging outright: Connecticut and Massachusetts maintain clear bans as of 2026, with Maine and Puerto Rico also restrictive, while California and Texas bans have been found unconstitutional but remain murky to enforce.

On top of the caps and bans, surcharging has process requirements. You must register your program with Visa and Mastercard at least 30 days before you begin, and you must disclose the surcharge clearly — at the point of entry, again at the point of sale, and as a separate line item on the receipt. For a funeral home this disclosure layer overlaps with the FTC Funeral Rule, which already requires itemized, transparent pricing — so a surcharge line can’t hide, which is precisely what makes the optics question unavoidable. Getting funeral home surcharging wrong on any of these points risks card-brand fines or losing card acceptance entirely.

Credit only, never debit or prepaid (terminal must detect card type). Cap at the lower of 3% or your actual cost. Skip it entirely in Connecticut and Massachusetts (and treat Maine, Puerto Rico, California, and Texas as consult-your-attorney). Register with the card brands 30 days ahead. Disclose at entry, at the register, and on the receipt. Miss one and your funeral home surcharging program is non-compliant.

Surcharge, Dual Pricing, or Cash Discount

“Surcharging” is shorthand for three different mechanisms that pass card cost, and the one you choose matters more for a funeral home than for almost any other business. A true surcharge adds a fee on top of the price for credit transactions — it’s the most regulated path, debit-excluded, capped, and banned in some states. Dual pricing displays two prices on everything: a lower cash price and a standard card price. A cash discount posts the card price and takes a stated amount off for customers who pay cash or check. Dual pricing and cash discounts are legal in all 50 states, including the states that ban surcharging, because the law treats a discount for cash as a protected right rather than a penalty on credit.

For funeral home surcharging, that distinction does real work. Dual pricing and cash discounts sidestep the debit-detection burden, they work in banned states, and — most important here — they frame the gap as a discount for paying another way rather than a penalty added to a grieving family’s bill. The same dollars change hands; the words on the page read very differently. Most funeral homes that pass card cost successfully do it through dual pricing or a cash discount, not a literal surcharge line, and they confirm the legal details against the surcharge rules before they start.

It’s legal in every state, it doesn’t require your terminal to police debit cards, and it presents the cash price as the deal rather than the card price as a punishment. For a business where the customer is grieving and the bill is already large, “save $270 by paying with a check” lands far better than “$270 credit card surcharge” — even though the math is identical — the usual answer to funeral home surcharging.

Why a Funeral Surcharge Is the Highest-Stakes One in Retail

This is the part of funeral home surcharging that no compliance guide covers, because it isn’t a compliance question. A funeral home runs on reputation and referral — families choose you because someone they trust did, and a single bill that felt exploitative can end that chain. A clearly disclosed surcharge line is perfectly legal, but on the bill of a family in acute grief it can read as charging extra to mourn, and that perception is its own cost, separate from any fine. The FTC Funeral Rule guarantees the family sees every line, so there’s no soft place to put it.

That’s why need-type should drive the decision. At-need — when a family is arranging a funeral in the days after a death — is the worst moment to present a card fee; many funeral homes simply absorb the processing cost on at-need card payments, or steer the large balance to ACH or check where no fee is passed, or use dual-pricing language that reads as a courtesy. Pre-need is different: a family planning ahead, calmly, months or years before a death, is in a normal purchasing posture, and funeral home surcharging or dual pricing is far more defensible there. Splitting the policy by need-type — gentle and often absorbed at-need, more straightforward on pre-need — is how thoughtful firms handle funeral home surcharging.

Legal does not mean advisable in the moment. A surcharge line on an at-need funeral bill can cost you a referral network worth far more than the fee you recovered. Treat at-need and pre-need as different decisions: lead with absorbing or ACH-steering at-need, reserve any explicit pass-through for pre-need and for the gentler cash-discount framing, and never let the recovered fee cost you the family’s trust.

How to Pass the Cost Without It Reading as Predatory

The goal of funeral home surcharging isn’t to recover every dollar of processing cost on every transaction — it’s to pass what you reasonably can in a way that protects both your margin and your reputation. Three moves get you there.

- Lower the underlying rate first — move to interchange-plus so the cost you’re deciding whether to pass is as small as possible; a smaller fee is a smaller optics problem and sometimes one you can simply absorb.

- Choose dual pricing over a surcharge line — it’s legal in all 50 states, skips the debit-detection trap, and frames the gap as a discount for cash rather than a penalty on a grieving family’s bill.

- Split the policy by need-type — absorb or steer to ACH at-need where grief makes any fee read badly; apply the pass-through more straightforwardly on pre-need, where the family is planning calmly.

Done this way, funeral home surcharging stops being a yes-or-no question and becomes a routing-and-framing one. The firm that gets the underlying rate down, passes cost as a discount rather than a penalty, and reads the moment correctly recovers real money without the bill ever feeling predatory. It fits inside the bigger picture of funeral home payment processing, where the at-need charge, pre-need, and the bundled processor are the other costs worth auditing.

Frequently Asked Questions

In most states, yes, with rules: the surcharge is capped at the lower of 3% or your actual cost, it can’t be applied to debit or prepaid cards, you must register with the card brands 30 days ahead, and you must disclose it at entry, at the register, and on the receipt. Connecticut and Massachusetts ban it (Maine and Puerto Rico are restrictive; California and Texas are unsettled). Confirm your state with counsel before you start.

It’s legal, but it’s a reputation decision as much as a compliance one. A clearly disclosed fee on an at-need funeral bill can read as charging extra to grieve, and a funeral home lives on referral. Many firms absorb the cost at-need or steer the balance to ACH, and reserve any explicit pass-through for pre-need, where the family is planning calmly. The economics of recovering the fee rarely justify the risk to the trust that brings families to you.

Dual pricing is usually the better fit. It’s legal in all 50 states, including the ones that ban surcharging, it avoids the debit-card detection trap, and it frames the difference as a discount for paying by cash or check rather than a penalty added to a grieving family’s bill. The dollars are the same; the language reads far better in a funeral home. A true surcharge line is the harder path to justify in funeral home surcharging.

Keep reading on passing card costs, compliantly

Send Your Statement. We’ll Show You the Compliant, Gentle Way to Pass Card Cost.

If you’re weighing whether to surcharge, or you want to pass card cost without it landing badly with families, send Brookside one recent statement. We’ll show you your true rate, what a compliant dual-pricing or cash-discount setup looks like for a funeral home, and where steering to ACH makes more sense than passing a fee. The review takes about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day