HVAC Runs a Membership Business and a Replacement Business on One Account

HVAC Runs a Membership Business and a Replacement Business on One Account

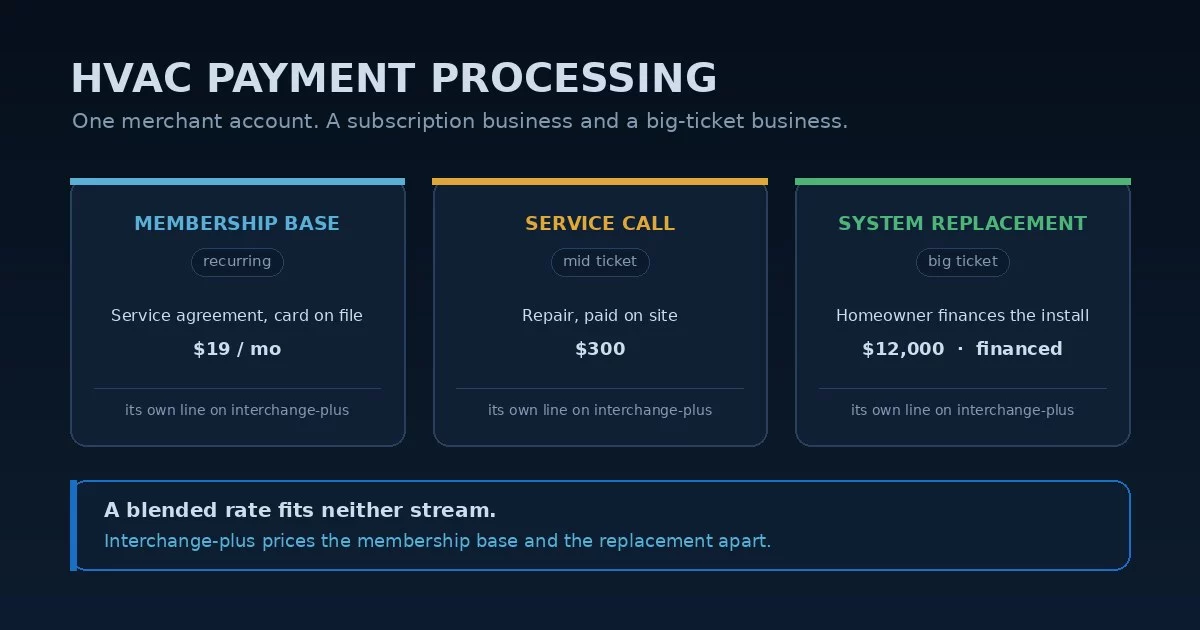

HVAC payment processing looks like a rate problem and is really a two-business problem. A heating and cooling company runs two very different operations through the same account: a maintenance-membership base, where hundreds of small charges hit cards on file every month on a recurring service agreement, and a replacement-and-install shop, where a single system swap can land an eight-to-fifteen-thousand-dollar ticket that the homeowner finances. Those two streams cost a processor very different amounts to run, and a blended rate can only ever be tuned for one of them. The headline percentage your software quotes is built around one of those streams — and quietly overcharges the other — the half of HVAC payment processing nobody quotes.

That single fact reshapes how an owner should think about the whole setup. Get HVAC payment processing wrong and a rate that looks fine on a $19 monthly membership charge is silently expensive on a $12,000 financed replacement. Get it right and both streams are priced on what they actually cost, instead of an average that fits neither.

Your HVAC Software Usually Picks Your Processor

Most HVAC payment processing decisions get made by accident. Almost every operator runs a field-service platform — ServiceTitan, Housecall Pro, FieldEdge, Jobber — and most ship with an integrated payments product that bundles card processing, consumer financing, and membership billing right into the app. ServiceTitan runs recurring membership billing and third-party financing inside the job; Housecall Pro bundles payments, service-plan auto-billing, and financing similarly. The convenience is real: the membership charge, the service call, the financed install, and the renewal all reconcile inside one system.

The cost of that convenience is leverage. When the processor comes attached to the software, the rate is usually a single blended number, and you rarely get to shop it without the vendor’s blessing. It means your HVAC payment processing rate was set by whoever your software vendor partnered with, not by you — and that same vendor now decides your financing offer and your surcharge tool too. As with any home services payment processing setup, the bundled processor is rarely the one you’d have chosen, and the only way to know whether the rate is fair is to put it next to an interchange-plus quote on your real volume. We walk through one platform’s economics in detail in our ServiceTitan fee breakdown.

A blended rate charges the same percentage on a $19 recurring membership charge and a $12,000 financed install, even though those cost the processor very different amounts. Interchange-plus breaks out the network cost and the processor’s markup as separate lines — the only view that shows what each of your two streams actually costs.

The Membership Base and the Replacement Are Priced as One

Here is the structural problem at the center of HVAC payment processing. The maintenance-membership base is high-frequency and low-value — many small recurring charges, billed to a card on file, where the per-transaction fixed fee matters more than the percentage. The replacement and install work is the opposite: rare, but large, where the percentage is everything and the fixed fee rounds to nothing. A blended rate is a single compromise stretched across both, so it is never actually right for either — it is set for one stream and merely tolerated on the other.

On interchange-plus, those two streams stop fighting each other. The card-on-file rate on the membership base is its own line, and the large-ticket interchange on the financed replacement is its own line, and you can read and shop each instead of trusting one number to cover both. For an HVAC contractor running real membership volume alongside install work, separating the two is where HVAC payment processing stops leaking. An HVAC merchant account priced this way shows the two streams apart instead of burying them in a blend.

A blended rate optimized for the $19 monthly membership is quietly expensive on the $12,000 replacement; one tuned for the replacement overpays on every recurring charge. There is no single percentage that is fair to both, which is exactly what a bundled blended price hides.

Where the Percentage Actually Bites

On the replacement side, a fraction of a percent stops being rounding. A few points on a $12,000 system swap is real money, every time, which is why the big ticket is where HVAC payment processing deserves the most attention. Two levers live here, and a bundled setup usually makes both decisions for you. The first — and for HVAC the dominant one — is consumer financing: letting a homeowner spread a replacement over monthly payments while you get paid upfront. It turns an emergency a customer might patch instead of replace into an approved install, and platforms wire a financing offer (Wisetack, GreenSky, Synchrony) straight into the in-home proposal.

The second lever is surcharging — passing the card cost to the customer on a large credit-card job, which an HVAC software’s built-in tool will happily switch on at its own default. Surcharging can offset the fee, but it is state-regulated, capped, disclosure-bound, and never allowed on debit, so the rules matter; we keep those in the surcharge legality and dual-pricing guides rather than re-explaining them here. The point isn’t that financing or surcharging is always right; it’s that on the replacement side these are real decisions worth making deliberately, not defaults your software flips for you. On the big ticket, HVAC payment processing rewards a deliberate hand.

When the financing offer and the surcharge button both live inside your HVAC software, they apply the vendor’s partner, rate, and rules — not necessarily the ones that fit your margin or your state. Both are legitimate big-ticket levers; the decision should be yours, not a default toggle.

The Recurring Stream That Funds the Off-Season

The maintenance-membership base is the steady floor of an HVAC business, and the basics there are worth getting right: a card-on-file rate you can actually see, clean recurring billing on whatever cycle you sell — monthly, quarterly, or annual — and failed-payment handling so an expired card doesn’t quietly drop a membership and the renewal revenue with it. It’s the unglamorous half of HVAC payment processing, and it’s the half that keeps cash moving through the slow shoulder seasons. None of that requires a special account; it requires a rate structure that prices the recurring stream honestly instead of burying it in a blend.

One classification detail is worth a look. An HVAC contractor codes under MCC 1711, Heating, Plumbing and Air-Conditioning Contractors — a standard special-trade code, not a high-risk one. Confirming you’re coded as the contractor you are is a free check, since a miscode can carry the wrong interchange profile. But it’s standard-risk either way; nothing about HVAC payment processing freezes accounts the way a true high-risk vertical can. The money is in the rate structure on top of the code, not the code itself — heating and cooling payment processing priced on the real mix beats any code tweak, and clean HVAC credit card processing on the membership base protects the recurring revenue.

What Actually Lowers an HVAC Company’s Card Cost

The levers that move HVAC payment processing are structural, not a tenth of a percent on the swipe. Done right, HVAC payment processing prices the membership base and the replacement on separate terms instead of one blended average.

- Move to interchange-plus so the recurring membership and the financed replacement are each priced on their true cost — the only model where a small card-on-file charge and a large-ticket install aren’t forced under one number.

- Price the big ticket deliberately — decide financing and surcharging (where compliant) on the replacement side yourself, instead of letting your software’s defaults decide for you.

- Keep the processor shoppable — an HVAC merchant account you control rather than one rented from your software — so the rate, the financing offer, and the surcharge tool all stay your call.

- Protect the membership base — a visible card-on-file rate, clean recurring billing, and failed-payment handling so an expired card doesn’t silently drop a renewal.

HVAC payment processing is a two-business problem before it’s a rate problem. The owner who audits the whole account — the embedded rate, the recurring membership base, the financed-replacement pricing, and the code underneath — almost always finds more in the parts that never appear on the quote than in the one number that does.

Frequently Asked Questions

Not necessarily. A bundled processor like ServiceTitan’s or Housecall Pro’s built-in payments is built for convenience and usually priced on a blended rate that averages your card types together. It may be competitive on small recurring membership charges, but the only way to know — especially on financed replacements, where HVAC payment processing actually bites — is to compare it against an interchange-plus quote run on your real volume.

Financing is the core big-ticket tool for HVAC: the homeowner spreads a replacement over monthly payments while you get paid upfront, which closes installs a buyer might otherwise patch and defer. Surcharging can offset the card cost on a large credit-card job, but it’s state-regulated, capped, disclosure-bound, and never allowed on debit, so the rules matter (see our surcharge-legality and dual-pricing guides). The point is to choose deliberately rather than let your software’s default decide.

No. HVAC codes under MCC 1711 (Heating, Plumbing and Air-Conditioning Contractors), a standard special-trade code, not a high-risk one — worth confirming you’re coded as the contractor you are. It’s standard-risk, so there’s no high-risk fork that freezes accounts. The savings come from pricing the membership base and the replacement separately — the way HVAC contractor payment processing should be run — not from a special account.

Keep reading on rates, big-ticket pricing, and the field-service verticals

Send Your Statement. We’ll Price the Membership Base and the Replacement Apart.

If your processor came bundled with ServiceTitan, Housecall Pro, or another HVAC platform, send Brookside one recent statement. We’ll break it into an interchange-plus view by card type, show you what the financed replacements are really costing against the small recurring membership charges, and lay out whether financing or surcharging fits the install side. The review takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day