In Solar, the Lender Funds the Job — Your Merchant Account Only Sees the Cash Deal

In Solar, the Lender Funds the Job — Your Merchant Account Only Sees the Cash Deal

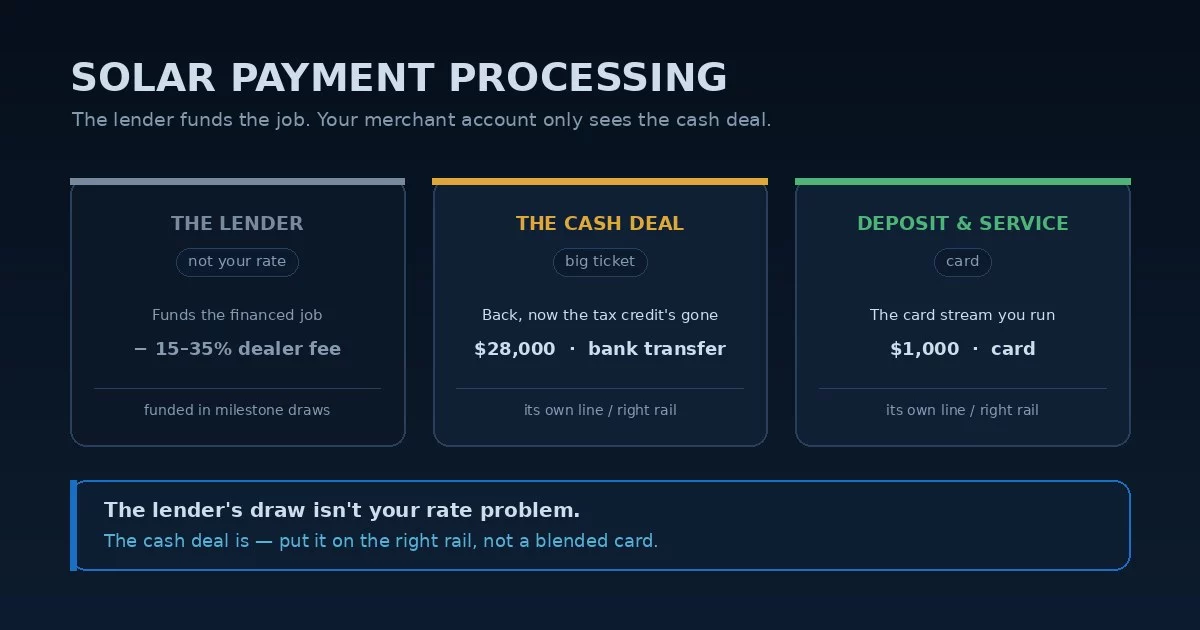

Solar payment processing is unusual because the biggest payer is a lender, not a card. On a financed system — still most of the market — a solar loan company funds the installer in milestone draws and takes a dealer fee of fifteen to thirty-five percent off the top, baked into the homeowner’s loan. What actually runs through the merchant terminal is everything around that: the cash deal, the deposit, the change order, the service and monitoring call. That card stream looks small next to a $30,000 financed install, which is exactly why it gets ignored, and exactly why solar payment processing tends to run on whatever blended rate came bundled with the proposal software.

That has quietly changed in 2026. With the federal residential solar tax credit expired at the end of 2025, the old loan trick — re-amortizing the balance once the homeowner claimed their thirty percent — is gone, and the cash price has become a far stronger close. More homeowners are paying cash or with a home-equity line to dodge the dealer fee entirely, which means the card-and-bank stream a solar company used to wave off is suddenly where real money moves. That makes solar installer payment processing a live cost center for the first time in years. Get solar payment processing wrong now and a rate nobody questioned is expensive on every cash deal you close.

The Financing Dominates, So Nobody Prices the Card

Most solar payment processing decisions get made by accident, for a specific reason: all the attention goes to the loan. The proposal runs through design software, the close depends on which lender approves the homeowner, and the big money arrives from GoodLeap, Sunlight, Dividend, or whoever the installer is signed with — so the deposit and the cash deal feel like an afterthought, collected on whatever processor came attached to the CRM. The card volume looks small against the financed pipeline, so shopping the rate never reaches the top of the list.

The cost of that inattention is leverage. When the processor is whatever was bundled and the card stream is treated as rounding, the rate is a single blended number nobody ever questioned. It means your solar payment processing rate was set by default, not by you — and across a year of cash deals, deposits, and service calls, that default adds up. As with any home services payment processing setup, the bundled processor is rarely the one you’d have chosen, and the only way to know whether the rate is fair is to put it next to an interchange-plus quote on your real card-and-bank volume — small as it feels against the financed jobs.

A blended rate charges the same padded percentage on a $1,000 deposit and a $28,000 cash system, even though those cost a processor very different amounts and a five-figure cash deal almost never belongs on a card at full rate. Interchange-plus — and bank-transfer options — break the cost apart so the part of solar the lender doesn’t fund is priced on what it actually is.

What the Lender Takes Off the Top

To understand solar payment processing you have to understand the dealer fee, because it shapes everything around the card. When a homeowner finances, the lender charges the installer a fee — commonly fifteen to thirty-five percent of the system price — and rolls it into the loan principal. A $25,000 system financed at a twenty-five percent dealer fee means the homeowner actually finances closer to $31,000, even though the contract says $25,000. The gap between the cash price and the financed price is that fee, and it is large enough that the Minnesota Attorney General has sued several major solar lenders over how it was disclosed.

This is not a card-processing cost — no merchant account changes a lender’s dealer fee — but it is why the cash deal matters so much now. With the tax credit gone, the honest cash price undercuts the financed price by thousands, and a solar company that can take a large cash or bank payment cleanly keeps margin the lender would otherwise have eaten. The financed draw is an accounts-receivable and lending question; the cash deal is the one that lands in your merchant account, and solar payment processing is really about pricing that side well rather than the part the lender controls.

When financing carried the day, the card stream was an afterthought and a blended rate didn’t seem to matter. Now that more homeowners pay cash to skip the dealer fee, a five-figure cash deal run on a card at a full blended rate can hand a processor seven or eight hundred dollars on a single sale — on exactly the deals where your margin is best.

Where the Percentage Actually Bites Now

On the cash side, a fraction of a percent stops being rounding. A few points on a $28,000 system is real money, every time, which is why the cash deal is where solar payment processing deserves the most attention in 2026. The first lever is the payment rail itself: a large cash purchase paid by ACH bank transfer turns a percentage into a flat fee, and on a five-figure ticket that difference is the cost of a panel or two. Card has its place for deposits and smaller balances, but the full cash system is usually a bank-transfer job.

The second lever is surcharging or a cash-discount program — passing the card cost to the customer on a large credit-card payment — which can offset the fee but is state-regulated, capped, disclosure-bound, and never allowed on debit; we keep the rules in the surcharge legality and dual-pricing guides rather than re-explaining them here. The point is that on a cash solar deal these are real, deliberate decisions — which rail, whether to surcharge — not defaults your CRM’s bundled processor makes for you. On the big cash ticket, solar payment processing rewards a deliberate hand.

When the card processor comes attached to your proposal or CRM software, it applies the vendor’s rate and rules to every deposit and cash deal — rarely the bank-transfer-first setup a five-figure cash system actually wants. The rail and the pricing on a cash deal should be your call, not a default toggle.

Solar Is the One Trade Where the Account Itself Needs Care

Every other field-service trade can treat the merchant account as a commodity — standard-risk, no special handling. Solar is the exception, and solar payment processing has to account for it. A solar company often takes a large deposit on a system that won’t be energized for weeks or months, after permitting, install, and the utility’s permission to operate — and that pattern, a big charge long before delivery, with real cancellation and chargeback exposure, is exactly what makes a processor nervous. Many will classify solar as elevated-risk, hold a rolling reserve, or cap volume until history is established. A processor that understands the deposit-then-deliver timeline is worth more here than a tenth of a percent on the rate.

The coding underneath matters too. A solar installer usually codes under MCC 1731, Electrical Contractors, since the work is electrical at its core, though some sit under 1799, Special Trade Contractors. Neither is inherently a doomed classification, but solar draws more underwriting scrutiny than the code alone implies, because of the ticket size and the fulfillment gap rather than the trade. Clean solar contractor payment processing on the deposit side and disciplined solar credit card processing across the cash deals — paired with an account built for the fulfillment timeline — beat any code tweak. This is the one vertical where a solar merchant account is a decision, not a default — the place solar payment processing stops being a commodity.

What Actually Lowers a Solar Company’s Card Cost

The levers that move solar payment processing are structural, not a tenth of a percent on the swipe. Done right, solar payment processing prices the cash deal on the right rail and keeps the deposit on an account built for a long fulfillment cycle.

- Put the cash deal on the right rail — bank transfer for a five-figure cash system, card for deposits and smaller balances, so you stop paying a card percentage on the deals where your margin is best.

- Move the card stream to interchange-plus so the deposit, the change order, and the service call are each priced on true cost instead of one blended number nobody questioned.

- Get an account built for the fulfillment gap — a processor that understands deposits taken months before energization, so you’re not hit with a surprise reserve or a hold mid-season.

- Make the cash price a real option — now that the tax credit is gone, presenting an honest cash price next to the financed one wins margin the dealer fee would otherwise take, and the merchant setup is what lets you collect it cleanly.

Solar payment processing is a cash-deal-and-deposit problem hiding behind a financed pipeline. The owner who audits the part the lender doesn’t fund — the rail on the cash deals, the rate on the deposits, and the account’s comfort with a long fulfillment cycle — almost always finds more in the part nobody priced than in the financing they don’t control.

Frequently Asked Questions

More than it used to. The financed draw arrives from the lender and never touches your rate, but the cash deals, deposits, change orders, and service calls run through your account all year — and with the federal residential tax credit gone since the end of 2025, more homeowners are paying cash to avoid the dealer fee, so that stream is growing. Pricing it well, and putting large cash systems on a bank transfer rather than a card, is what solar payment processing is actually about.

Because of the gap between payment and delivery. A solar company often takes a large deposit on a system that won’t be energized for weeks or months, with real cancellation and chargeback exposure in between — the pattern underwriters watch most closely. Many processors respond with an elevated-risk classification, a rolling reserve, or a volume cap until history is built. It’s worth seeking a processor that understands the deposit-then-deliver timeline rather than taking whatever’s bundled — the one place solar payment processing genuinely needs a deliberate account.

More care than the other trades, yes. Solar usually codes under MCC 1731 (Electrical Contractors), sometimes 1799 (Special Trade Contractors) — but the classification matters less than finding a processor comfortable with large deposits on long-fulfillment jobs. Unlike standard-risk trades where any account will do, solar contractor payment processing benefits from an account chosen deliberately for the deposit-and-delivery profile, not a bundled default.

Keep reading on rails, big-ticket pricing, and the field-service verticals

Send Your Statement. We’ll Price the Cash Deal and the Deposit Right.

The lender’s dealer fee isn’t your rate’s problem — but the cash deals and deposits you run all year are, and they’re growing. Send Brookside one recent statement and we’ll break the card-and-bank stream into an interchange-plus view, show you which deals belong on a bank transfer instead of a card, and flag whether your processor is set up for the deposit-and-delivery timeline before a reserve surprises you. The review takes about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day