State Interchange Fee Laws: Which States Are Following Illinois

Why You’re Suddenly Hearing About State Interchange Fee Laws

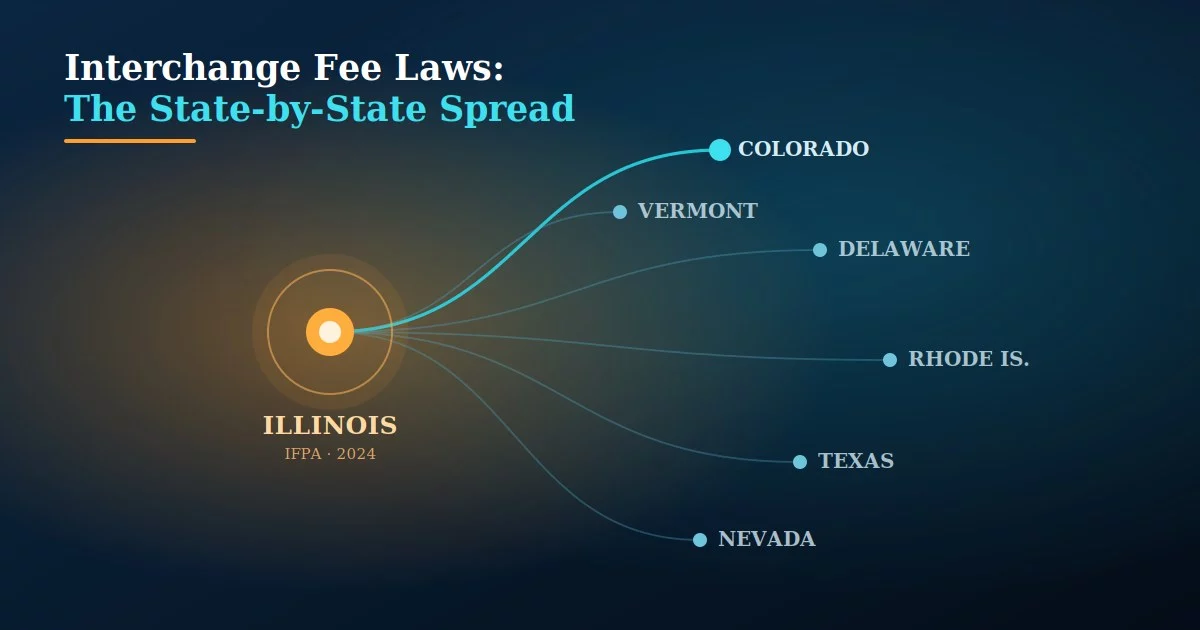

For two decades, the fees you pay to accept a card were set in two places only: by the card networks, and by Congress. That is changing. A wave of state interchange fee laws is now moving through statehouses, each one trying to carve the tax and tip portion of a transaction out of the swipe fee you pay. Illinois passed the first one in 2024. As of mid-2026, roughly a dozen states are weighing their own versions.

If you run a restaurant, a shop, or any business that accepts cards, two questions follow naturally: is one of these laws coming to my state, and if it does, will it actually lower my costs? This is the honest map — which states have acted, where each bill stands, and why the answer to “will it save me money” is more complicated than the headlines suggest.

What a State Interchange Fee Law Actually Bans

These laws do not ban interchange. They ban it on one slice of the transaction. When a customer pays a $40 restaurant check with a $10 tip, plus sales tax, the whole amount runs through the card network, and interchange is normally calculated on the full total. A state interchange fee law says the network and bank may not charge interchange on the tax and gratuity portions — only on the underlying $40 of goods and services.

That is the core of every version of these interchange fee laws by state: the swipe fee should apply to what you actually sold, not to money you are merely collecting on the government’s behalf or passing through to a tipped employee. Supporters argue a business should not pay a processing fee on sales tax it never keeps.

Interchange is the largest part of your processing cost, and it is set by Visa and Mastercard, then collected by the bank that issued your customer’s card. It is charged as a percentage of the entire transaction. On a typical 2% to 2.5% effective rate, the tax-and-tip slice of a check is a small fraction of your total bill — which is why the dollar savings from these laws are modest even where they apply.

Which States Have Interchange Fee Laws in 2026

The list of swipe fee laws by state is short on enacted statutes and long on pending bills. Here is where the serious activity sits as of mid-2026.

Illinois is the flagship. Its Interchange Fee Prohibition Act passed in 2024 and was the first law of its kind. But its start date has now slipped twice — to July 1, 2026, and then, in a June 2026 budget move, to July 1, 2027 — and the courts have carved it up (more on that below). Illinois proved the concept is politically possible; it has not yet proved it works in practice.

Colorado is the furthest along of the followers. The Colorado interchange fee bill, SB 26-134, passed both chambers of the legislature in May 2026 and was sent to the governor. It bars networks from charging percentage-based interchange that includes sales tax, adds an anti-circumvention clause so networks cannot simply raise the rate on the rest, and exempts smaller issuers with under $60 billion in assets.

Delaware and Rhode Island are moving through committee. Delaware’s HB 315 focuses on tips added to card transactions; Rhode Island’s H 8212 and S 2522 drew supportive testimony from small-business groups earlier in 2026. Beyond those, the Electronic Transactions Association — the industry group fighting these bills — has flagged roughly eleven states as carrying real risk of enactment, including California, Massachusetts, Nevada, New York, Pennsylvania, Tennessee, Texas, and Vermont.

Alabama is the exception that explains the rule. Rather than ban interchange on tax, its SB 221 simply removes card fees from the sales-tax base, effective September 1, 2026 — reaching a similar goal through tax law instead of payments law, and sidestepping the federal fight the interchange bans are about to walk into.

Why These Laws May Not Survive Federal Preemption

Here is the part the headlines skip. Even a state interchange fee law that passes cleanly runs into federal banking law, and so far federal law is winning. National banks operate under the National Bank Act, and federal regulators argue that a state cannot dictate the fees those banks charge.

In 2026 the Office of the Comptroller of the Currency issued a rule and order concluding that federal law preempts the Illinois statute for national banks, and the National Credit Union Administration followed with a parallel rule for federal credit unions, both effective June 30, 2026. On June 1, 2026, a federal judge in Illinois issued a permanent injunction blocking the law as applied to national banks, federal savings associations, out-of-state banks, and the card networks themselves.

What is left after that injunction is narrow: the law would still reach cards issued by Illinois state-chartered banks and credit unions, and only if it survives to its 2027 start date. For most of the cards your customers actually carry — issued by large national banks, run on Visa and Mastercard rails — the federal carve-out keeps the tax-and-tip portion subject to interchange anyway.

A state can pass one of these laws and still deliver almost nothing to merchants, because the institutions that issue most consumer cards are federally preempted out of it. Until the courts settle whether states can regulate network-set fees at all, every one of these laws sits under the same cloud Illinois is under now.

What State Interchange Fee Laws Mean for Your Effective Rate

Strip away the politics and here is the merchant math. Even where one of these laws applies to a given card, the savings are small — the interchange on the tax-and-tip slice of a typical check is on the order of a dollar or so. Meaningful across a year at restaurant volume, but not transformative, and only if the law applies to the card used.

The savings are also not automatic. Your point-of-sale system has to isolate the tax and gratuity amounts and transmit them with the transaction, and the reimbursement typically runs through a submit-and-rebate process rather than a discount at the register. That is real operational work for a small carve-out.

If a sales rep pitches one of these laws as a guaranteed cost reduction or a reason to sign a new processing contract, treat it with heavy skepticism. The savings are modest, conditional on federal preemption fights, and tied to start dates that keep moving. No interchange carve-out should be the reason you sign anything.

What you can control is your effective rate — the true all-in percentage you pay across every transaction — and that has nothing to do with whether state swipe fee legislation passes. If your effective rate is high, that is the real cost worth attacking, today, regardless of what any statehouse does. For the deepest look at how the flagship law is actually playing out, our breakdown of the Illinois interchange-on-tax-and-gratuity law walks through the same carve-out math in detail.

While these laws fight it out in court, the dependable win is making sure you are not overpaying on the 98% of every transaction that no state law touches. A clean interchange-plus structure shows you exactly what the networks charge and what your processor adds on top — and that visibility is available now, not in 2027.

Frequently Asked Questions

Illinois passed the first one in 2024, though its effective date is now delayed to July 1, 2027. Colorado’s bill passed the legislature in May 2026 and went to the governor. Delaware and Rhode Island have bills advancing in committee, and roughly a dozen more states have introduced similar legislation.

Only modestly, and only on the tax and gratuity portion of a transaction — not the whole sale. Because federal preemption carves out cards issued by national banks, the practical savings are small and uncertain. Your effective rate is a far larger and more controllable cost.

In large part, yes. The OCC and NCUA issued rules in 2026 confirming federal preemption for national banks and federal credit unions, and a federal court permanently enjoined the Illinois law as applied to those institutions and the card networks. State-chartered banks and credit unions can still be subject, and the litigation is ongoing.

Keep reading on interchange and what you actually pay

Skip the Statehouse Math. Pull Your Real Effective Rate First.

State interchange fee laws may or may not ever touch your business, and even then only on a sliver of each sale. Send Brookside one recent statement and we’ll calculate your true effective rate, show you where the markup actually sits, and tell you what is worth attacking now — no statehouse required. Learn more about payment processing consumer protections from the CFPB.

Get Your Actual Effective RateNo obligation • No pressure • Response within one business day