Auto Body Payment Processing: The Deductible Is the Whole Story

In a Body Shop, the Only Thing You Card Is the Deductible

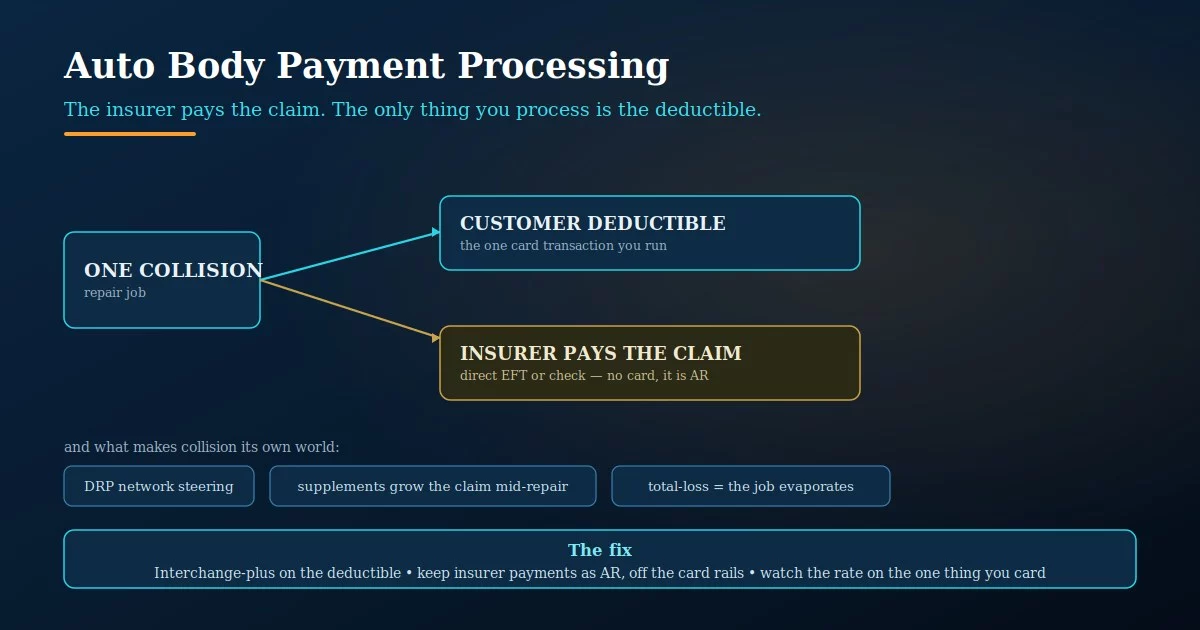

A collision repair is a big-dollar job, but almost none of it runs through your card terminal. The insurer pays the claim — the bulk of the money — directly to the shop. The customer pays one thing: the deductible. That single fact reshapes auto body payment processing completely, because your entire card-processing footprint is essentially one transaction per job, and everything about how you should be priced follows from that.

It also means the usual advice aimed at retail or restaurants is close to useless here. You’re not running hundreds of varied tickets a day; you’re running a handful of deductibles, each potentially several hundred to a couple thousand dollars, while the real revenue arrives as an insurance payment on terms. Get the card side right and there’s a second, sharper problem hiding in how the insurer chooses to pay you.

Price the Deductible Like It’s Your Whole Card Volume — Because It Is

The deductible is the customer’s responsibility and, in most jobs, the only thing they hand you a card for. It’s also not small — commonly $500 to $1,500 — which means each one is a meaningful transaction, and you run them often enough that the pricing on them is the pricing of your entire card business. On a shop floor where the deductible is close to 100% of your card volume, a flat, bundled rate overcharges every dollar you process, because there’s no low-cost transaction mix to dilute it.

This is the part of collision repair payment processing that’s easy to ignore precisely because the card volume looks small next to the claims. But “small volume” and “overpriced” aren’t the same thing — if every card transaction you run is a sizable deductible on a flat rate, you’re overpaying on all of it. A body shop merchant account should price that deductible on transparent terms, because it’s not a side channel; it’s the whole channel.

Because the deductible is nearly all of what you process, there’s nothing to average a hidden markup against — every card transaction is a large, similar deductible, so a flat rate’s cushion lands on all of it. Low volume doesn’t protect you from a bad rate; it concentrates the damage.

When the Insurer Pays by Virtual Card, You Eat the Fee

Here’s the one that quietly costs body shops real money. Insurers increasingly pay claims not by check or EFT but by virtual credit card — a one-time card number emailed to the shop to “run” like any other card. It sounds convenient. It isn’t. When you process that virtual card, you pay interchange on the entire claim amount — 2 to 3% of a $6,000 repair is well over a hundred dollars in fees on money the insurer owed you anyway, money that would have cost nothing as an electronic transfer.

This is the insurer pushing its payment onto the card rails at your expense, and most shops don’t realize they can decline it. You can almost always request EFT or ACH instead of accepting a virtual card, and on claim-sized amounts that single change saves more than any rate negotiation on your deductibles ever will. Good auto body payment processing means keeping the claim payment off the card rails entirely — the deductible belongs on a card, the claim does not.

Processing a claim paid by virtual credit card means paying 2–3% to receive money that an EFT would have delivered for free. On a single large repair that’s over a hundred dollars handed to your processor for nothing. Ask every insurer that sends a virtual card whether they’ll pay by EFT instead — most will, and it’s the highest-value call you can make.

The Claim Is a Moving, Slow Number — the Deductible Isn’t

Three things make collision unlike any other repair trade. Insurers run direct repair programs (DRP) that steer volume to in-network shops, so a chunk of your work arrives with the payment relationship already defined. Supplements are routine: once teardown reveals hidden damage, the claim grows mid-repair — but the customer’s deductible doesn’t change, so your card exposure stays fixed while the insurance side moves. And total-loss decisions can evaporate a job entirely; the insurer totals the car and the repair revenue you’d counted on disappears, sometimes leaving only a teardown fee.

Underneath all of it is time. A car sits in your shop for weeks, and the claim pays on completion, often 30 to 45 days out. That’s the cash-flow shape of auto body shop credit card processing: the small, fast deductible up front, then a long wait for the large, slow insurance payment. It’s the opposite of a business that gets paid at the counter, and your payment setup should reflect that reality rather than fight it.

The deductible funds quickly; the claim is slow AR. That gap is normal in collision — the mistake is paying to close it, like running an insurer’s virtual card to “get paid now” and surrendering 2–3% to front your own receivable. The claim is coming. Don’t buy it back from yourself at card rates.

What Auto Body Payment Processing Should Actually Look Like

Auto body payment processing comes down to a short list, because the surface is small. Price the deductible — your real card volume — on interchange-plus, so the one transaction you run on every job isn’t sitting on a padded flat rate. Refuse virtual-card claim payments and request EFT or ACH instead, keeping the claim off the card rails where it belongs. Track your effective rate on the deductible volume specifically, because that number is your whole card cost in this business. And build your expectations around the cycle — fast deductible, slow claim — rather than paying anyone to compress it.

Do that and there’s very little left to leak. Collision shop payment processing is simple precisely because so little of the money touches a card — but the two places it does touch (the deductible you price, the virtual card you decline) are exactly where shops give money away without noticing. Close those two and you’re done.

Two mistakes, both quiet: a flat rate on the deductible means overpaying on essentially 100% of your card volume, and accepting insurer virtual cards means paying 2–3% to receive your own claim money. Neither shows up as a line you’d notice. Price the deductible transparently and insist on EFT for claims, and the leaks close.

Frequently Asked Questions

Interchange-plus pricing on the deductible — which is nearly all of your card volume — and a firm policy of requesting EFT or ACH instead of accepting insurer virtual cards on claims. The deductible belongs on a card; the claim doesn’t. Get those two right and there’s little else to optimize.

No. When an insurer sends a virtual credit card, processing it means paying 2–3% interchange on the full claim — over a hundred dollars on a large repair — to receive money an EFT would deliver for free. You can almost always request EFT or ACH instead, and you should.

Usually, yes — the deductible is typically the one card transaction per job, often $500 to $1,500. Because it’s nearly all of your card volume and each one is sizable, it’s worth pricing carefully; a flat rate there overcharges essentially every card dollar you take.

Keep reading on automotive payments and what you pay

See What You’re Paying on Deductibles — and on Virtual Cards

Send Brookside one recent statement and we’ll calculate your true effective rate on your deductible volume and flag every insurer virtual-card payment you’ve been eating fees on that could have been a free EFT. No switch required to find out. Learn more about payment processing consumer protections from the CFPB.

Get Your Body Shop Rate ReviewedNo obligation • No pressure • Response within one business day