Towing Payment Processing: Two Ways to Get Paid

In Towing, You Get Paid Two Completely Different Ways

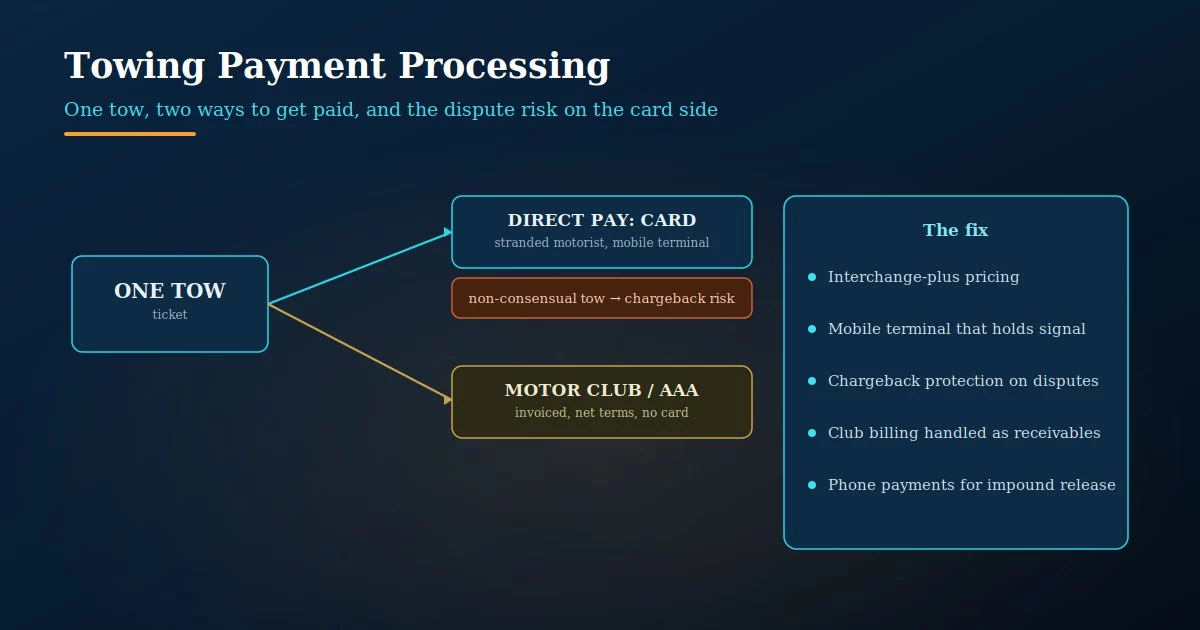

A tow company runs two businesses that happen to share a truck. One is the stranded motorist who pays on the spot — a card swiped on the shoulder of a highway. The other is the motor club, the insurer, or the police rotation that sends the call and pays on an invoice weeks later, never touching a card at all. Towing payment processing goes wrong when a setup built for one of those is asked to handle both, because the two paths have nothing in common except the tow itself.

Then there’s the part no other roadside trade carries quite the same way: the tow the customer didn’t ask for. Non-consensual and impound tows are a real share of the work, and they’re also the ones most likely to be disputed — which means the card side of towing carries a chargeback risk that can quietly reshape your entire processing relationship.

Half Your Revenue Never Touches a Card

Start by separating the money. Direct-pay work — the motorist on the roadside, the customer reclaiming an impounded vehicle — is card volume, paid then and there. Club and contract work — AAA and other motor clubs, insurance dispatch, dealership accounts, municipal police rotations — is accounts receivable. You send an invoice, you wait on net terms, and a card never enters the picture. A lot of tow truck payment processing setups blur these two together, and that blur costs money in both directions.

It costs you when club work gets pushed through a card processor or a “billing platform” that takes a percentage of money that should have cost you nothing to collect — you don’t pay card fees on a check from AAA. And it costs you the other way when the direct-pay card volume, the part that genuinely runs on the card rails, sits on a flat rate that hides what the roadside swipes actually cost. A clean towing company payment processing setup treats these as the separate revenue streams they are.

Money from a motor club, an insurer, or a municipal contract arrives by check or ACH on terms — it is accounts receivable, and it should cost you almost nothing to collect. If a processor or billing service is taking a percentage of your club work, you’re paying card-rail pricing on money that never went near a card.

How You Take the Card Matters as Much as the Rate

The direct-pay side runs on a mobile terminal in the cab, and how that terminal works decides part of your cost. A card physically tapped or dipped on a card-present device is the cheapest way to run a transaction. A number read over the phone and keyed in by hand — common when arranging an impound release before the owner arrives — costs more and carries more risk. A tow operator working with a flaky mobile setup or keying transactions that could have been card-present is paying a premium on top of whatever the rate already is.

Connectivity is the unglamorous half of this. A terminal that drops signal on a rural shoulder or a parking garage turns a quick card-present sale into a delayed or keyed one. For roadside towing credit card processing, a mobile terminal that actually holds a connection and accepts a tap is worth more than a slightly lower advertised rate on a device that strands you when the car is already on the hook.

A tapped or dipped card costs less and disputes less than a number keyed in by hand. The fix is a real mobile terminal that holds a signal and takes contactless, so your roadside transactions run card-present instead of getting keyed because the device couldn’t connect.

The Chargebacks That Land Towers on a High-Risk Account

This is the part that separates towing from every other mobile trade. When a customer’s car is towed without their consent — a parking enforcement tow, a police-ordered tow, an impound — the person paying is frequently angry, and angry customers dispute charges. A non-consensual tow has a far higher chance of becoming a chargeback than a service the customer requested, and a run of those chargebacks is exactly what makes a processor reclassify a tow company as high-risk, with rolling reserves and held funds attached.

The defense is documentation and the right processor, not luck. Clear authorization where consent exists, signage and records where it’s a non-consensual tow, and a processor who understands the trade rather than one who panics at the first dispute and freezes your account. Getting blindsided by a chargeback wave and landing on a high-risk merchant account with a reserve is one of the most expensive things that can happen to a tow operator’s cash flow — and it’s largely avoidable with the right towing payment processing setup from the start.

It isn’t the single disputed tow that hurts — it’s what a cluster of them does to your standing. Cross a processor’s chargeback threshold and you can be moved to high-risk pricing with a rolling reserve that holds a slice of every deposit. Documentation on non-consensual tows and a processor who knows the trade are what keep you off that path.

What Towing Payment Processing Should Actually Look Like

Put it together and good towing payment processing follows the work. Price the direct-pay card volume on interchange-plus so the roadside swipes show their true cost instead of hiding in a flat rate. Run that volume through a real mobile terminal that holds a signal and takes contactless, so transactions stay card-present. Keep club and contract billing on the receivables side, collected by check or ACH, not bled through a percentage. Build in chargeback protection and the documentation habits that keep disputed tows from becoming a reserve. And track your blended effective rate on the card side, because that’s the only honest number for what the roadside half of the business pays.

None of this slows down a single tow. It just stops the two halves of the business from being forced through one ill-fitting setup — paying card fees on receivables, keying swipes that should be tapped, and waking up on a high-risk reserve after a bad month of disputes. For a tow operator, that’s real money and real cash-flow stability, recovered from a setup nobody built for the trade.

The worst setup pairs a flat rate on the roadside card volume with no plan for disputes. You overpay on every swipe because the markup is hidden, then a wave of non-consensual-tow chargebacks drops you onto a high-risk account with a reserve. Transparent pricing on the card side and a processor who understands towing chargebacks fix both before they cost you.

Frequently Asked Questions

It can be, mainly because non-consensual and impound tows get disputed more than requested services, and a cluster of chargebacks pushes a processor to reclassify the account. It isn’t automatic — with documentation on non-consensual tows and a processor who knows the trade, many tow companies run on a standard towing merchant account rather than a high-risk reserve.

On a mobile terminal in the cab that connects over cellular and accepts a tapped or dipped card. Card-present transactions cost less and dispute less than numbers keyed in by hand, so the priority is a device that holds a signal — a terminal that drops connection forces you into pricier keyed transactions.

No. AAA, insurer, and municipal contract work is paid by check or ACH on terms — it’s accounts receivable, not card volume, and it should cost you almost nothing to collect. Routing it through a processor or billing service that takes a percentage means paying card-rail pricing on money that never touched a card.

Keep reading on roadside payments and what you pay

See What Your Roadside Card Volume Actually Costs

Send Brookside one recent statement and we’ll calculate your true effective rate on the direct-pay card side, flag whether club work is being charged card fees it shouldn’t be, and check your exposure before a chargeback wave puts you on a reserve. No switch required to find out. Learn more about payment processing consumer protections from the CFPB.

Get Your Towing Rate ReviewedNo obligation • No pressure • Response within one business day